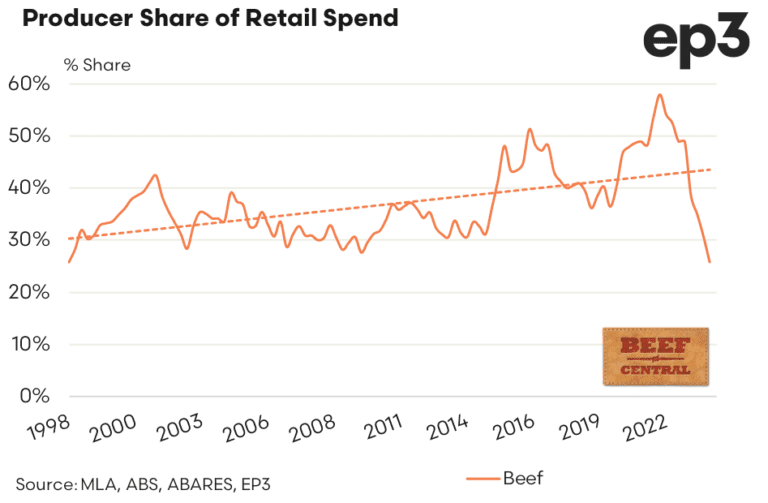

The AUSTRALIAN beef producer’s share of retail dollar spend on beef has continued its rapid descent, hitting all-time historical lows in the December quarter.

The steady decline in saleyard cattle prices during the fourth quarter of 2023, combined with a marginal easing of retail beef prices, saw the beef producer share of retail $ drop to the lowest point since the data-set began back in 1998, at just 25.8 percent.

As can be seen on the graph published above, back in 2022-23 when cattle prices approached record levels, the producer share index soared to almost 60pc.

The release yesterday of quarterly Consumer Price Index data from the Australian Bureau of Statistics provides the opportunity to update the quarterly producer share of retail dollar calculation published jointly by Episode3 and Beef Central.

The scrutiny of producer share of red meat sales $ takes on additional significance this month, as a number of inquiries get underway into supermarket retail pricing (see today’s separate report).

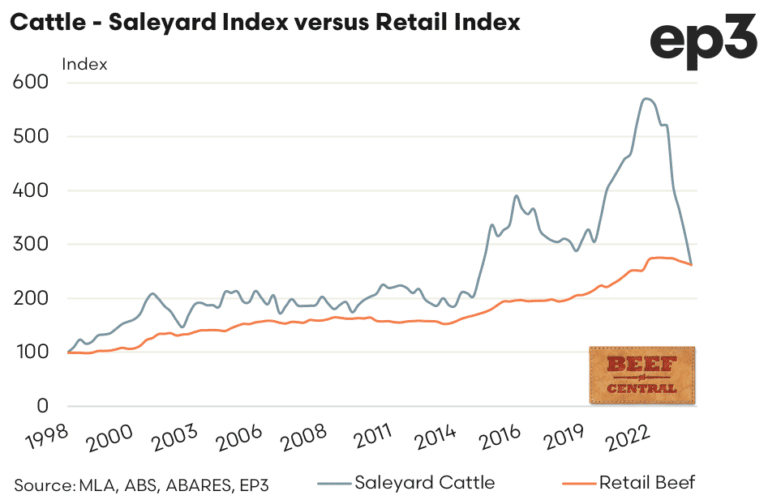

As can be seen in the accompanying graph, cattle prices continued to ease during the final quarter of 2023, with the saleyard cattle index slipping nearly 17pc from 314 in Q3 to 262 by the end of December. Over the same timeframe, the retail beef index eased marginally from 266 to 262, Episode 3 calculated. This slight drop in the retail beef index equates to a decline in average beef prices at the supermarket/butcher from $26.19/kg to $25.80/kg over the December quarter.

Worth noting, the CPI retail price data used to produce the summary carries some lag (December quarter data was released only yesterday). Cattle prices have improved significantly since the start of January, meaning the March quarter producer retail share result, due for release in early May, will capture more recent trends.

Background to the producer share of retail prices calculation

In collaboration with analyst Matt Dalgleish from Episode 3, Beef Central in July last year launched a new quarterly series looking at trends in the beef producer’s typical share of the retail consumer’s spend on beef products.

A similar analysis was compiled by MLA for four years, before being discontinued by the industry service delivery company back in December 2016. The project was originally launched as a result of producer requests during the 2012 MLA annual general meeting.

Beef Central sought, and gained MLA’s approval to resurrect the discontinued series, based on clear reader interest. The same formula is used to compile the new set of results as originally used by MLA (see explanation at base of page).

Episode 3 and Beef Central now jointly publish a quarterly report, soon after ABS quarterly retail beef price data is released. This typically happens in late July, late October, late January (today’s report) and late April.

The exercise sees national saleyard cattle prices in carcase weight terms being converted into an estimated retail weight equivalent and compared to average retail beef prices, as reported by ABS (see summary below).

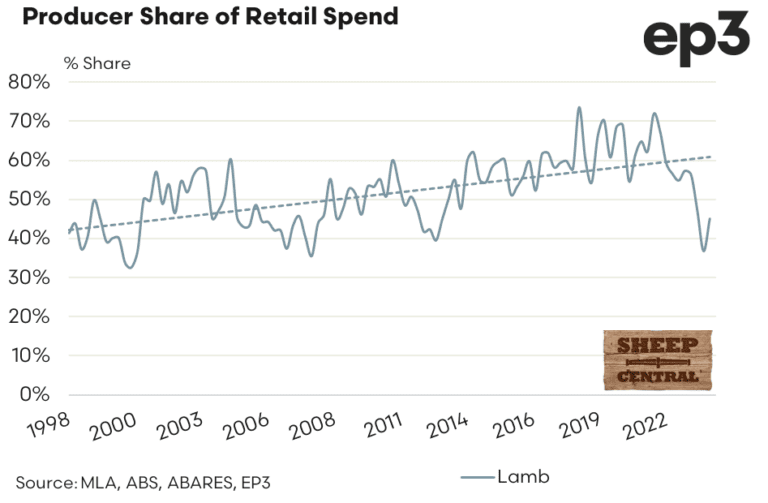

Lamb result shows improvement

A similar quarterly retail share calculation is made for lamb producers.

The latest December quarter result (see graph, or click here to view separate Sheep Central article) shows a more positive outcome than for beef. Lamb producers’ share of retail spend lifted from 36.5pc at the end of September to 45pc for the final quarter of 2023.

As can be seen in the graph, lamb retail prices softened during the final quarter – some would say as a result of pressure on major supermarket retailers over prices seen as being out of alignment with livestock market trends. Coles in November announced significant discounts on some, but certainly not all, lamb lines.

Beef showed only a much more modest decline in average retail price in the December quarter, CPI data showed.

About the producer share of retail spend calculation

The beef producer share of the retail dollar is calculated using a range of assumptions. The national saleyard trade steer indicator is used as the benchmark livestock prices, representing animals suited for the domestic market. Livestock prices are collected by MLA’s NLRS. Converting the carcase weight price to an estimated retail weight equivalent price is achieved using a retail meat yield for beef of 68.7pc.

The indicative retail meat prices are calculated by indexing forward actual average beef prices during each quarter, based on meat sub-group indices of the Consumer Price Index, provided by ABS. These indices are based on average retail prices of selected cuts (weighted by expenditure) in state capitals.

The producer share is calculated by dividing the estimated retail weight equivalent livestock price by the indicative retail price.

Click here to read earlier reports in this series:

Should cattle producers be paying more attention to retail margin share?

Beef Central’s project partner Episode 3 is an independent, data-driven market analysis service providing insights and reports to the agriculture industry, food manufacturing sector and their associated markets. Through robust analytical assessment, EP3 assists agricultural stakeholders to make better, more informed decisions that drive profitability. The company is experienced in producing high-quality reports used by government, RDC’s and corporate entities. In addition, EP3 is available on

a retained basis with clients to provide on-going and bespoke information to assist in their sales or purchasing process. Click here to access the Episode 3 website.