THE recent surge in interest in building new abattoirs around Australia stands in contrast to the challenges the red meat processing sector has faced in recent decades.

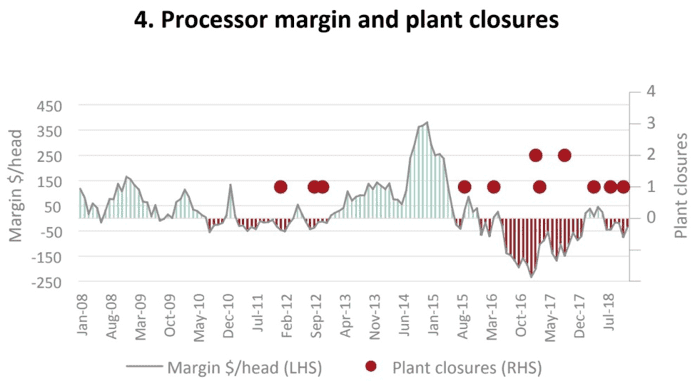

More than 90 abattoirs closed across Australia between the mid 1980s and 2000s, according to statistics reported in the ACCC’s 2017 cattle and beef market study, while a further 16 cattle and sheep plants have closed in the past decade, according to a March 2019 AMPC report.

Gradual declines in sheep and cattle populations over that period and rising labour, energy and regulatory costs have been among the major catalysts for the ongoing rationalisation in the sector.

Source: AMPC

The trend has led to fewer numbers of larger processors operating around the country, as existing operators have sought to drive efficiency through scale.

The ACCC report also noted that despite the  loss of many individual processing facilities, overall processing capacity has increased over that time, as bigger abattoirs have grown larger.

loss of many individual processing facilities, overall processing capacity has increased over that time, as bigger abattoirs have grown larger.

The backdrop of challenging conditions and multiple abattoir closures in recent decades begs the question: why the sudden recent interest in building new ones?

A common message behind new abattoir proposals is that the rationalisation that has occurred in Australia’s meat processing network has left regional gaps that have created opportunities to rebuild, and to take advantage of recent technological advances to drive new efficiencies.

Interviews with proponents of individual projects over recent weeks have identified a range of motivations behind the various proposals including:

– The perception that greater competition is needed in slaughter markets, a common theme of producer input to industry focused-Senate inquiries between 2013-2017 and the 2017 ACCC cattle and beef market study (In its assessment the ACCC found ‘typically close competition’ exists for prime cattle in most regions, with exceptions including NQ and Tasmania – see more from its report in this separate article);

– The view that higher transport efficiencies and animal welfare benefits can be achieved by processing livestock closer to where they are produced, and transporting chilled or frozen meat, instead of cattle or sheep, longer distances by road to consumer markets and export ports;

– The potential to harness new technology including automation and renewable energy in new purpose-designed greenfield plants to achieve greater labour, energy and water-saving efficiencies;

– An opportunity to satisfy growing demand for more service kill capacity from the increasing number of dedicated supply chains and new beef and sheepmeat brands. MLA figures show the number of MSA-licensed brands rose from 131 three years ago to 172 last year. The limited number of plants offering service kill capacity can mean some brand owners currently have to transport livestock significant distances to access required processing space;

– A number of proposals have been driven by local councils seeking to attract overseas investment, with a particular focus on China, to drive economic and employment development projects.

But the question remains: Can new abattoirs succeed in a trading environment that has seen so many recent closures?

The chances of success will clearly vary according to the specific circumstances of each individual proposal, with key factors including the ability of new developments to compete against incumbents or to find underserviced niches capable of paying premiums, and the extent of specialised processing experience and knowledge proponents either have or can access.

Some of the projects on the large list identified yesterday clearly tick more of these boxes than others, while some proposals could perhaps best be described as fishing expeditions for investment, in which relatively limited proposals have been publicly cast out through media in the hope of getting a bite from a big funding fish.

That all of these proposals have been launched leading into what has turned out to be one of the worst droughts in Australia’s recorded history obviously hasn’t helped the cause for attracting investment.

But beyond current seasonal and livestock and water supply challenges, some with significant experience in the processing sector say many of the new proposals are simply not realistic.

In today’s high operating cost, low supply trading environment, they believe a sound argument in fact exists that Australia needs fewer processing plants working more shifts.

Ross Keane has extensive experience in the livestock sector as a fourth generation cattle, sheep and goat producer, a livestock agent and a long-serving general manager livestock for major processor AMH (now JBS Australia). He has also served the industry nationally as the independent chairman of the Red Meat Advisory Council and SAFEMEAT.

Ross Keane has extensive experience in the livestock sector as a fourth generation cattle, sheep and goat producer, a livestock agent and a long-serving general manager livestock for major processor AMH (now JBS Australia). He has also served the industry nationally as the independent chairman of the Red Meat Advisory Council and SAFEMEAT.

In the current environment Mr Keane says a new plant built to suit a boutique market could have a chance of succeeding, providing it is able to capture a premium that is large enough to offset the dearer costs of processing each animal in a smaller plant.

A key challenge in the current environment is available livestock supply.

It is several years since the Australian cattle herd last peaked, and the percentage of females being processed still exceeds 50 percent of total weekly kills.

Mr Keane predicts it will be at least a decade before the herd can return to anywhere near the 30 million mark again.

At the same time, Australia’s sheep numbers have plunged from 180 million in the early 1990s to about 70 million today.

Feedlots have helped to even out seasonality challenges in the cattle industry, but must be located in the grain growing areas to operate efficiently and consistently, he pointed out.

‘For one to succeed, at least one will have to close’

Mr Keane noted that most of the planned new abattoir projects propose to operate at a capacity of 500 to 2000 head per day.

He predicts that if these proposals go ahead, the end result will be either:

- The new plant will be superior in cost to operate than an existing plant in the area, so it will survive, and the old plant will close; or

- The new plant will not be able to compete against the existing plant for a variety of reasons including reputation (solid payment reputation), location (for cattle and labour supply), efficiency (labour saving devices etc), access to port, among others, so the existing plant would stay and the new plant would be mothballed.

“Examples of this would be if a new big plant is built in North Queensland, and it is efficient and reliable, then pick which one of the existing plants must close,” he said.

“Or if a proposed 2000 head per day plant is built on the Darling Downs, and is efficient, then at least two of the current plants will close.

“Really, what do we gain by doing this?”

“Most existing plants today have an upgrading program in place, and only the better located plants are left, so it makes more sense to improve those facilities,” he said.

He believes the focus should be on improving the capacity of existing abattoirs by utilising labour saving technology and installing enough additional chiller and freezer capacity to enable existing plants to work a longer span of hours, and provide flexibility for available livestock supply.

“Currently Kilcoy is the only seven-day a week plant that I am aware of, and it is still upgrading to a double shift seven days a week,” Mr Keane said.

“A smarter move might be the existing operators get together to build a ‘super plant’ that is more internationally competitive, and different operators operate different shifts etc, but that probably won’t happen due to the competitive nature of our industry and ACCC issues.”

Another pre-requisite he believes a new abattoir needs to succeed is sound port access, particularly given that more than 70 percent of Australia’s beef production is exported.

The port of Brisbane

This may come as a surprise but all meat processed for export in Queensland is currently exported for economic reasons through the Port of Brisbane.

This includes meat processed at plants much further north in close proximity to other export ports, including Townsville, Mourilyan (Innisfail), Mackay, Rockhampton and Gladstone.

Freight rates mean it is still more economical to deliver meat from NQ and CQ to the Port of Brisbane to load onto the large container ships for export.

While many of the new projects have received favourable media coverage suggesting each is likely to go ahead, Mr Keane said a large number of the proposals he has seen come forward do not appear to be realistic, particularly in their estimated total costs to build.

“Meeting compliance for noise, odour and environmental regulations is often overlooked I suspect,” he said.

He also added that striking the right balance in scale between size, livestock availability and operating efficiency was a key challenge for new proposals.

“There is always a fine line to tread,” he said.

“Bigger throughput can often lessen your fixed costs, which reduces the per head or per kilogram cost to operate.

“Versus that, the more you kill, the more you need to buy, and often you give up the saving in the cost to operate with the premium to buy the numbers.

“Big throughput plants are good when you have a plentiful supply of cattle, but can be a headache when livestock numbers are short.”

Competition a critical driver of innovation for industry: producer

Competition was an important means of driving innovation throughout the industry, Central Queensland cattle producer and Cattle Council of Australia northern independent director David Hill said.

Any investments that fostered innovation and helped to capture added value and premiums for quality meat should be welcomed, he said.

Mr Hill said the industry has historically tended to focus on a high throughput, minimal-margin approach and economies of scale.

Mr Hill said the industry has historically tended to focus on a high throughput, minimal-margin approach and economies of scale.

But higher costs of production compared to other beef exporting nations meant Australia could not compete in export markets on price, and nor could it compete against cheaper proteins in the domestic market on price.

Examples of innovation to capture value included the ‘boutique-scale’ custom-plant to be built by Blair and Josie Angus near Moranbah, which will feature a cellular design to enable bespoke processing of individual animals to precise specifications, rather than a chain approach.

The larger processing companies were also innovating, he said.

“Look at what Teys are trying to do, for example, and the research they are doing at Lakes Creek.

“They are looking at the potential of automation to improve compliance to customer specifications and have a consumer ready product that is packaged in a way that doesn’t impact on eating quality and can extend shelf life, which is improving efficiency and adding value.”

He said talk of moving away from ‘a commodity approach’ had been around for some time, and there had been examples of this happening, but it now seemed to be gaining momentum as a real focus.

The approach of maximising the potential value of the product, especially for the consumer, was critical, he said.

“Value can be a point of difference as well as price,” he said.

“It would be to the detriment of the future viability of this industry if all value chain participants weren’t prepared to invest in future opportunities because of the belief that they could be unlikely to see a return that would warrant the risk.

“There will always be a level of competition, be it between red meat sectors, or, the big one at the end of the day, filling space on the consumers’ plate.

“A quote about competition I read recently said ‘the best part of competition is that through it we discover what we are capable of-and how much more we can actually do than we even believed possible’.

“Competition will drive innovation.”

In 2018/19, MSA delivered an additional $198m to producers in the form of price differential for MSA v Non-MSA young cattle. This translates to a direct in the pocket benefit of $84/ head for non-feedlot cattle producers. There is ongoing growth of MSA, with 43% of the national adult cattle slaughter MSA graded in 2018/19 with the target of 50% this financial year. The system works!

MSA underpins 195 brands who are licensed to use the MSA trademark and MSA is recognised by the United Nations Economic Commission for Europe as the global standard in eating quality. MSA is one of only two programs outside the US to be certified by the USDA as a Process Verified Program. MSA remains the largest science based consumer eating quality program in the world.

Eating quality remains in the top five priorities for many of our major markets internationally. Achieving a higher price for our red meat will lead to greater returns for producers. It is a focus for our industry – and MLA – to produce and market a product that consumers will be willing to pay more for.

We must continue to highlight and lead globally in our quality, food safety, animal welfare and sustainability attributes – and therefore position ourselves as a global leader in the supply of high quality red meat and the preferred choice for consumers.

Michael Crowley

General Manager Producer Consultation & Adoption

Meat & Livestock Australia

Thanks Michael but why has beef consumption in Australia halved in the 20 years we have had MSA? Millions of levy dollars were spent on its development and operation over the 20 years and it has failed to deliver any increase in consumption. If there are 195 brands where are they on shelf? If these processors have the right to display the MSA logo, why are there none to be seen in our supermarkets? I am sure you have received acknowledgement for the good efforts of your people past and present but this is not why MSA was developed. It must provide at retail a grading system that gives certainty to the customer of its eating quality. In thisd MLA have failed.

Australian Cattle Industry Council

John:

You can’t be serious in trying to align declining beef consumption with MSA’s performance. Worldwide, red meat consumption in developed, affluent countries like the US, the UK and New Zealand has been in decline for decades, as it has in Australia. The reason? People no longer live on a “meat and three veg” diet. They (me included) have discovered other foods – sushi, calamari, etc – that make our diets more diverse, and arguably, more interesting. Any decline in red meat consumption has nothing to do with ‘failure’ of a program like MSA, just a yearning for a more diverse, ethnically-influenced, and arguably somewhat more healthy diet than eating meat twice a day, as most of us once did. Despite recent declines, Australians continue to rank among the world’s heaviest consumers of red meat, when beef and lamb consumption are combined (South Americans eat a lot of beef, but next to no lamb). It can be vigorously argued that that would never have happened, without MSA.

USDA report “Average annual per capita disappearance of beef decreased 0.3 percent annually from 2000 to 2015 but has increased since 2016 and is expected to grow by 3.7 percent in 2018.” In Australia our figure has dropped 40 percent in the same time period. In the Us they eat 40 kgs of beef and we are struggling to eat 20 kegs with MLA supporting even less consumption. Get your facts straight.

John Gunthorpe, you portray a very detailed knowledge of AMH and your involvement in its operation. It would be interesting to know when you worked at AMH, for how long and in what position – as your name doesn’t ring a bell whatsoever.

AMH was a commodity processor, but evolved, particularly after its acquisition by global powerhouse JBS in 2007 into a company that focusses intently on high end branded beef, underpinned by the MSA system. Eating quality is the key criteria for beef produced in Australia (southern Australia in particular) and their brands like Great Southern, Pinnacle, Little Joe, Yardstick, Thousand Guineas and Hereford Boss to name a few all focus on products in top boning groups.

The MSA system is a fantastic one, and Australia is a world leader in quality beef because of it. As a qualified MSA grader, I can not speak highly enough of it. It is underpinned by science, and leaves luck out of the equation.

Thanks for the question Alf. I was a member of the team that negotiated the formation of AMH in 1985 and then its CEO until it was sold to ConAgra. After a few further owners it was purchased by JBS. I am encouraged by your enthusiasm for MSA but why do we not have labels on the meat product to assure consumers of the eating quality. In the USA they can purchase prime beef, choice beef, select beef or beef without a description and termed no roll beef. Where are the brands on shelf and what quality offers do they make?

Australian Cattle Industry Council

John Gunthorpe you have made the statement in your comment that “MSA is failing the domestic customer and our overseas importers”. Can you please provide some clear evidence to underpin your statement, or is this simply your opinion?

My experience as an MSA supplier, and as a contributor to the continued development of MSA for the benefit of the whole supply chain, has been very positive.

Thank you for your question Ian. MSA was introduced following a large amount of taste testing by David Crombie, Jason Strong and their team to identify the meat specifications that led to quality preference in our domestic consumer. It was developed to give some certainty to consumers surrounding quality of beef being consumed. It was anticipated this would lead to an increase in beef consumption in Australia.

Unfortunately as we know this did not eventuate. In the time we have had MSA beef consumption in Australia has fallen from about 40 kgs per person to now about 23 kgs. This is probably the strongest evidence showing that MSA has not worked.

This week MLA supported a proposed beef consumption nationally of 18 kgs per person. Who in MLA would authorize the support for a level of consumption below that currently being consumed is unknown, but we are funding their activity with our levies and this requires explanation. Hopefully I got it wrong.

MSA’s star rating system was abandoned at retail to increase the numbers being presented for grading by getting the support of the two large supermarkets. This decision denied consumers a retail grading system as is available in the USA where USA government graders judge each carcass as prime, choice, select and no roll and these gradings carry through to retail.

Go into your supermarket and buy cuts of beef based on branding with any certainty as to the quality of the beef. Most are packed in supermarket trays all in together. Where is MSA on these display shelves? Frankly, Aldi have captured some certainty of eating quality by selling Bindaree Beef products from northern NSW. Occasionally they special full muscled cuts from Teys and these are also good buying for eating quality.

MSA has a range of grades for cattle but we are only paid the same price premium for our livestock whether they rate few or many stars. Producers are not paid based on performance under MSA only yes or no. And on occasions cattle meet the MSA specifications but are then knocked out by the processors’ specifications.

Regarding overseas sales, company brands were prominent for many years before MSA. Of course the most significant brand is the establishment number of the abattoir from which the product is produced. Reputations go back decades when trading overseas but no matter the owner the establishment number stays the same. In all markets substitution happens of course. Some domestic Holstein fat with Australian grainfed beef and suddenly you can sell it as Japanese domestic Holstein beef at inflated prices.

I am sure you are aware of all this Ian but again thank you for the opportunity to outline our concerns.

Australian Cattle Industry Council

John clearly our views are poles apart. I come from a producer mindset and you come from a commodity processor mindset.

When I benchmark our business I don’t just look at the performance of one paddock, I look at every facet of the whole business to see where I can spend on improvements to get the most gain at the lowest cost. From an overall Australian beef industry perspective why would I want my levy dollars spent trying to increase per capita beef consumption in the minority size Australian market. Competing against increasing multiculturalism and cheap chicken would not be clever at all with so many other markets begging for our beef and willing to pay a much higher price. Clearly most of these global markets have a growing population which are prepared to spend a much greater proportion of their weekly wage on beef, while our good old Aussie friends are munching on their Chicken nuggets and buying flat screen TV’s.

Commodity processors margin model is to buy cheap, process cheap and sell quick for a bit more than costs. The most successful get paid for the product before they pay for the cattle. Cattle producers are completely different. They have huge costs to carry often for years before they ultimately sell for the best price on offer at that time. Clearly cattle producers need to receive the highest price available with such a high risk model. They cant simply reduce their buy price like a processor because they don’t have a buy price they have production costs. Modern producers like to think globally. We are happy to see our beef find a home in China or the USA rather than Australia, if that’s where the best price is. We don’t even mind loading them on a boat if they return more as slaughter cattle in Vietnam. It’s called self preservation. The result is there is less beef available to be sold in Australia. Good old supply and demand.

With regard to MSA cattle being paid as either in or out you really need to have someone explain the non-commodity grids that modern MSA producers are selling on. There is a range of price points depending on the EQ achieved.

Finally you asked where is MSA on the display shelves. MSA is not a brand. It is a science to underpin a brand. Mention of MSA can often be found in the story on the packaging. The MSA mark is a bit like the heart tick. Some choose to use it prominently and some don’t. One thing is for sure the eating quality of Australian beef today is so much better than it was 30 plus years ago. A range of things have changed to make that happen. One of the most significant is MSA grading.

PS

John we are in agreement that MLA supporting (with our levy) 18kg per person is ridiculous.

Attitudes that current practice in any business…….are the best they can be……..paves the way for innovators to disrupt conventional wisdom..

Australian red meat processors supply products into the foot and mouth disease free world markets. Competition comes from the other countries capable of supplying into these markets and these include USA and now some South American processors. For an Australian killing shed to remain competitive it needs to supply product at competitive prices into these markets.

China is taking increasing quantities of beef products but this is because of the severe drought impacting large tracks of some of our better beef producing regions. Breeders are being killed in less than ideal condition and the carcasses are sold to China as frozen quarter beef. China is a price market and will take product from the country offering the lowest cost red meat.

This is the worst time of the cycle to be opening new killing capacity. Today’s processors know they are facing tough times over the next 2 years. When breeders are killed in such numbers it will take years before numbers coming forward reach a level to support today’s installed capacity. Larger processors will rationalize the number of sheds operating hopefully in a controlled and measured manner. We saw this happen in the USA a few years back and today they are enjoying profitable kills as producers there earn lower levels of profitability.

Work completed recently by Dr Selwyn Heilbron for AMPC showed how uncompetitive Australian beef processors were with those countries supplying our worldwide customers. Australia is losing its ability to meet consumer expectations and not only on price. MSA is failing the domestic customer and our overseas importers. MLA’s proposal that it is the system that stands behind our local and overseas brands is a fallacy. Jason Strong was a member of the team that brought us the original MSA system and no doubt this is a challenge he is taking on in his new role.

AMH’s strategy was always to be competitive in the cost of production. This included sourcing livestock and selling into local and distant markets. Grahame Flynn and Peter White shared adjoining offices and used break square models to place the right carcass into the right market. However, some of our greatest success was working with our employees to provide greater flexibility on the kill floor and in the boning room.

Killing cattle is a very sophisticated business and, as AACo found out, it requires large investments with no surety of success. AACo ignored advice, bet the bank and lost. A month after signing the AMH agreement Keating said “banana republic” and its future was secure. Luck was on our side but it was the hard work of a dedicated team of management drawn from companies who were previously fierce competitors that changed the industry forever.

All those considering investment in a new shed I wish you every success but remember more will fail than succeed and there are many factors that will impact your operation over which you will have no control.

John, I struggle to understand why you mention AMH as a reference to todays markets, as AMH has not been in existence since 2007. I am sure all industry participants will agree the fundamentals of our industry at all levels are dramatically different. From quality to marketing and science to name a few.

The advent of point of differentiation branding is the only way our industry can maintain and grow in what is now a world market.

I am a producer that supplies various MSA based branded products and I congratulate the current processors that had the foresight to develop a point of differentiation both domestically and internationally.

I wish all aspiring business’s looking to establish a successful processing model or “shed” as John calls it, all the very best.

Negative comments from individuals living in the past with no skin in the game doesn’t do anyone a service.

How is the season treating you at Lucindale John?

Regards

Marc Greening

Yet again you do not disappoint Marc. Believe it or not marketing beef has always been a “world market”. The more issues change the more they stay the same. I mention AMH because I am proud of the work we did in those formative and challenging times. We made a difference and continue to do so. My friends in Lucindale tell me the season goes well for them. Certainly better than you are facing. I hope you get rain soon.

Australian Cattle Industry Council

Thank you David for you time in promoting and defending our industry. As a beef producer and consumer MSA I believe has helped transform our product from a inconsistent inferior product to a fantastic diverse product we have now. I think we all can remember how the product was produced, slaughtered and cooked in the seventies and eighties it is insulting when a lot of people who degrade our industry publicly have no skin in the game themselves they need to be called out .

Regards Howard Smith.

Thanks for the comment Howard. I think your memory plays tricks. We were serving Australian beef at Wimbledon in the 1980s and Vlado was serving Beef City steaks to his long list of customers at his famous Melbourne restaurant during the same period. Woolworths introduced Tender Valley into their supermarkets and Japanese and Korean customers enjoyed good quality Australian beef both grassfed and grainfed. What happens to the 57% of carcasses that do not grade MSA today? I am sure they are consumed somewhere.