GRAINFED cattle prices have recorded strong growth in 2015 but the latest surge in feeder cattle prices has far outstripped that of finished article.

As of this week, the Queensland over-the-hooks 100-day grainfed steer indicator averaged 559¢/kg, up 136¢/kg year-on-year (+32pc). The MSA equivalent grainfed indicator has recorded an even greater increase, at 564¢/kg this week, up 146¢/kg (+35pc) year-on-year.

In addition, grainfed cattle prices did not bottom-out as much as grassfed cattle did in 2013 and 2014. In mid-2014, when the Queensland over-the-hooks grassfed heavy steer indicator was sitting around 305-315¢/kg, the 100-day grainfed steer indicator was tracking at 385-395¢/kg – an 80¢/kg premium.

As illustrated in Beef Central’s regular 100-day grainfed trading budgets (click here to read most recent report) feeder cattle prices, however, have increased by a greater degree over the past twelve months.

The eastern states export paddock shortfed Angus feeder steer indicator last week averaged 334¢/kg liveweight – with contributors out of Queensland quoting as high as 345¢/kg – up 126¢/kg (+61pc) on this time last year. Saleyard prices recorded similar gains, with the national feeder steer indicator averaging 322¢/kg last week, up 124¢/kg (+62pc) year-on-year.

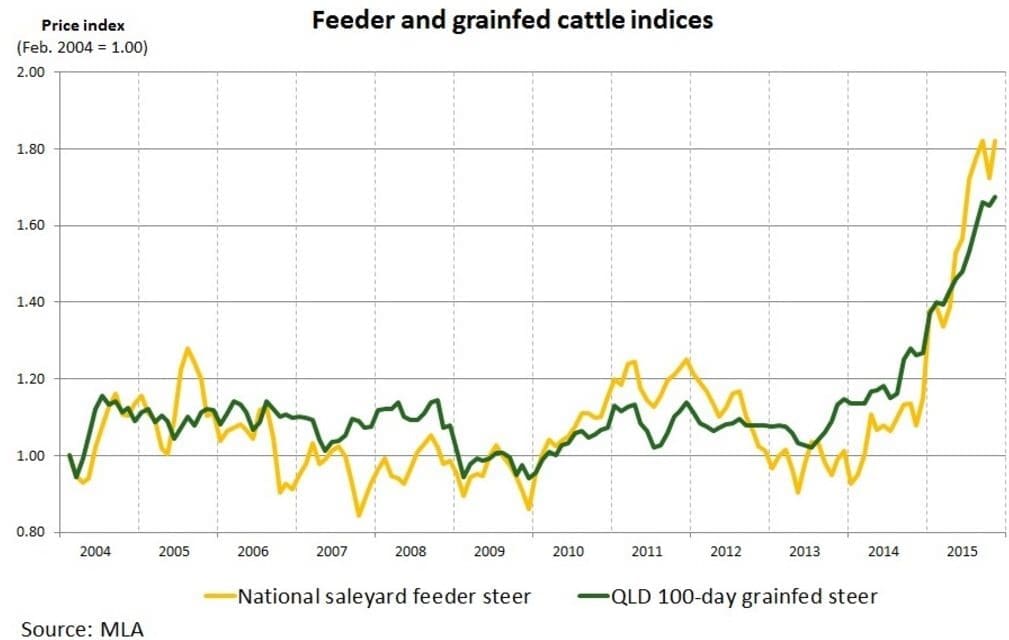

The chart above illustrates the recent rise in feeder and spot grainfed cattle prices.

(Beef Central would suggest, however, that a better comparison may have been between current feeder price and the forward contract 100-day grainfed price for slaughter March next year, as today’s 100-day grainfed finished steer price reflects the feeder market prices of 3-4 months ago. Our most recent breakeven calculation had forward price for grainfed steer SEQ kill at 590c, +30c higher than the 559c/kg spot price mentioned above).

Looking back, the strong rise in grain prices explains the spread between feeder and grainfed prices in 2007 and 2008, while the above average rainfall and additional restocker competition explains the divergence in 2011 and 2012. The onset of drought in 2013 and 2014 saw feeder cattle prices underperform during those years, while tightening supplies and some rain has seen the relationship reverse in 2015.

However, rapidly increasing feeder cattle prices have not deterred lotfeeders in the market and September quarter cattle on feed were estimated to be close to a record high, at just over 961,000 head.

What has given lotfeeders some breathing space has been the easing grain prices. Indicative Darling Downs delivered wheat (SWF1) last week was $273/tonne, back 17pc year-on-year (see yesterday’s regular feedgrain report from Robinson Grains’ Luke Walker). In addition, in their recently published Agricultural commodities: December quarter 2015, ABARES estimated the world wheat indicator price (US no. 2 hard red winter, FOB Gulf) to average US$215/tonne in 2015-16, back 19pc year-on-year.

Looking forward, cattle numbers on feed are expected to decline throughout 2016, as feeder cattle supplies continue to tighten – although, historically, they are likely to remain high.

Source: MLA

HAVE YOUR SAY