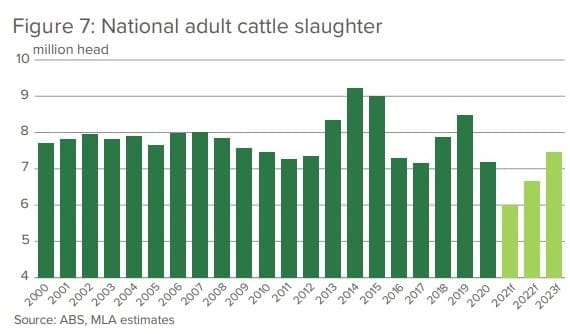

Meat & Livestock Australia has lowered its expectation for cattle slaughter numbers for calendar year 2021, in its latest Industry Projections Update issued earlier today.

The extent of post-drought rain has resulted in slaughter forecasts being revised downward from 6.3 million to 6 million head for 2021 – the lowest figure in 36 years – as producers opt for rebuilding over finished cattle sales.

While carcase weights are still expected to reach record levels, today’s Projections Update has revised weights slightly down to 308kg, bringing overall 2021 production estimates to 1.848 million tonnes carcase weight.

While carcase weights are still expected to reach record levels, today’s Projections Update has revised weights slightly down to 308kg, bringing overall 2021 production estimates to 1.848 million tonnes carcase weight.

“Seasonal conditions started to improve in autumn 2020, and by the end of 2022 calves born since this time are expected to hit the market which will increase the supply of cattle available,” said MLA’s market information manager, Stephen Bignell.

With above average rainfall predicted for all major cattle regions over the next three months and increased rainfall in northern Australia, pasture growth is expected to surge and strengthen the national herd rebuild into 2022.

Mr Bignell said good seasonal conditions across the eastern states and southern Western Australia continued to underpin demand and confidence in the sector.

“The cattle market continues at historic highs, with restocker and feeder demand fuelling record prices at the saleyard, which is flowing along the supply chain,” he said.

“The rebuild is expected to continue into 2022, as the BOM prediction of a La Niña will ensure that ground water supplies are available. The favourable harvest conditions of 2020 and 2021 have also allowed Australia a feed grain buffer should the 2022 season deteriorate.”

Mr Bignell said Australia remained a leading exporter of beef globally, with Korea remaining a strong and reliable market, and Japan continuing to purchase the most Australian beef. Australia has exported 660,568t of beef for the year-to-date, with 17pc lower volumes for the year-to-September.

Mr Bignell said Australia remained a leading exporter of beef globally, with Korea remaining a strong and reliable market, and Japan continuing to purchase the most Australian beef. Australia has exported 660,568t of beef for the year-to-date, with 17pc lower volumes for the year-to-September.

Lower export volumes have been the result of both supply and demand factors, Mr Bignell said.

“Most key export markets have fallen compared to 2020 volumes except for South Korea, which has held steady at a 2pc increase this year,” he said.

“Strong consumer purchasing power and sophisticated retail, foodservice and food manufacturing sectors, combined with a positive image of Australia as a trusted source for tasty and high quality will continue to underpin long-term growth for Australian beef exports to Japan.”

Here are some of the key messages from the latest Industry Projections Update:

Supply

Seasonal conditions started to improve in autumn 2020, and by the end of 2022 calves born since this time are expected to hit the market – increasing the supply of cattle available.

The rebuild is expected to continue into 2022, as the BOM prediction of a La Niña will ensure that ground water supplies are available. The favourable harvest conditions of 2020 and 2021 have also allowed Australia a feed grain buffer should the 2022 season deteriorate.

Herd size

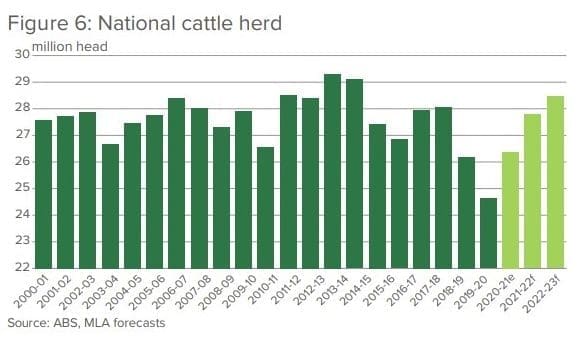

The predicted national herd for 2021 remains unchanged, still estimated to reach just over 26 million head this year, 7pc above the 2020 level. The herd rebuild has continued as positive conditions encourage producers to retain stock for breeding purposes – something that should be sustained with a positive three-month weather outlook across most of the country.

Production

On the back of lower slaughter than predicted and carcase weights dropping slightly, production has been revised to 1.848mt cwt – 12pc below 2020 levels. Similarly, throughout all of 2021, Australia continues to be limited by its current low supply outlook in terms of what can be produced. The 2023 outlook has total beef production at 2.308mt cwt, up 25pc on 2021 levels as herd numbers build.

Looking ahead

As southern conditions dry off over summer, saleyard throughput typically rises as restockers look to turn off cattle. While historically an increase in supply puts downward pressure on prices, the BOM three-month outlook is forecasting favourable conditions and above-average rainfall into summer, which could see pasture and grain availability allow producers to retain stock.

Given recent activity in the young cattle market has been primarily fuelled by restocker activity, prices are likely to follow the availability of feed moving into summer.

While demand from feedlots continues to push into the younger cattle market, the heights of the EYCI reflect the purchasing power of producers and thus, prices are likely to fall as restocker interest recedes.

Looking ahead, the EYCI is expected to reach 1020¢/kg cwt by the end of 2021, an indication that prices will fall away in the short term but remain historically high for the foreseeable future, MLA’s Projections update says.

The demand for domestic cattle is also likely to be influenced by shifts in the global trading landscape. With an already diminishing supply of prime cattle, saleyard prices are expected to benefit from the ongoing competition as lotfeeders, restockers and processors all look to secure cattle.

MLA is worth every dollar we give them:)