A decline in monthly shipments to the US was one of the reasons behind a large drop in Australia’s overall export beef trade in April.

A decline in monthly shipments to the US was one of the reasons behind a large drop in Australia’s overall export beef trade in April.

DAFF figures released yesterday afternoon showed that overall beef exports to April 30 reached 71,937 tonnes, down from about 83,300t in March, and almost 74,000t in April last year. That’s a drop of about 13 percent on March performance.

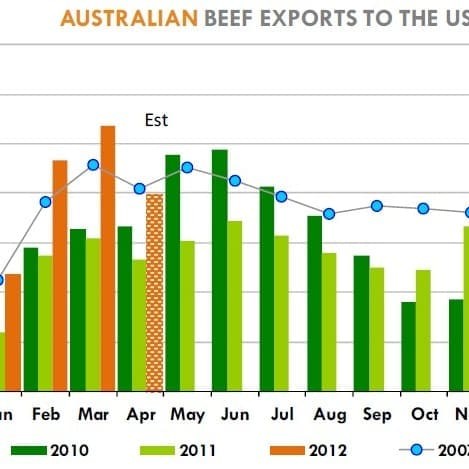

It should be pointed out, though, that March trade to the US was unusually high, with exports that month reaching 26,786 tonnes, well above the five year average (see graph).

Last month’s figures settled back towards the longer-term trend, totalling 19,154t. Compare that with exports to the US in April last year (13,250t, also evident in the graph, in lime-green), which was the start of a period where currency was making it difficult for Australian grinding beef to compete in the US market, and the US itself was entering a drought-driven cattle liquidation phase. This boosted domestic supply of grinding beef.

Part of the explanation for the drop in trade to the US last month can be found in two acronyms: BSE, and LFTB.

The controversy and media hysteria over the Lean Finely Textured Beef process has impacted on the grinding beef demand, generally, while the discovery of a fourth case of (atypical) BSE in the US put a dampener on trade during the closing stages of the month. Neither are expected to have long-term impact on trade or demand patterns, for beef into the US at least.

In other key markets, Australian beef trade into Japan last month reached 24,700t, just short of March’s 25,000t, and April last year (the last month before the Tsunami impact really stated to be felt) of 26,300t. Trading conditions for Australian beef in Japan remained difficult last month, with increasing shipments from competitively-priced US exporters, and the robust A$ making Japanese buyers cautious about their commitment to Australian beef, especially grainfed.

Trade into Korea also held up surprisingly well last month, given that the US now enjoys a 2.67pc tariff advantage over Australia since the signing of the Korea/US Free Trade Agreement on March 15. Our exports reached 7542t, down only modestly from 7900t in March, and 10,900t in April last year.

In other markets:

- The former Russian CIS states took 4470t of Australian beef in April, a big jump from 3200t in March but well short of April last year when we exported 6950t.

- Indonesia again suffered badly from import quota restrictions, with just 1391t shipped during April, well back on 2400t in March, but considerably better than 770t in April a year ago. Contrast this with 2010 and 2009, however, when monthly beef shipments during this time of year averaged 4000- 4300t.

- Total Middle East took 2260t last month, down from 3030t in March.

- The combined EU markets displayed solid growth in April, with shipments reaching 1431t, up from just over 1000t in March, and 1316t this time last year.

A recent EU Commission short-term Outlook forecasts that EU cattle prices will remain high in 2012, despite a decline in exports of both meat and live animals. The EU Commission says it expects domestic carcase prices for all categories to remain higher throughout 2012, due largely to limited supplies, with increased competition for earlier marketed finished cattle helping to offset higher feeding costs.

EU beef and veal production is forecast at 7.92mt for 2012, down 4pc on 2011. After a strong year for beef and veal exports in 2011, particularly to Russia and Turkey, EU beef and veal shipments are predicted to contract 29pc in 2012, to just 235,000t.

In contrast, EU beef imports are forecast to recover somewhat in 2012, as tight domestic supply and a gradual recovery in availability of supply from traditional suppliers helps to rejuvenate import volumes. However, while imports are forecast to increase 10pc, or 30,000t in 2012, overall EU per-capita beef consumption is still predicted to fall another 2pc.

Like many other markets, EU cattle prices reached record highs in 2011. Tight global supplies of beef in 2011 led to falling imports into the EU, while the very weak EU currency assisted exports, forcing domestic cattle prices higher.

HAVE YOUR SAY