Meat & Livestock Australia has produced the discussion piece published below, examining the implications for the Australian beef industry from Brazil’s recent breakthrough in gaining access to the US export market for chilled and frozen beef.

Beef Central broke the story in this item, first published last Saturday week, and since covered in this monthly column from our US market analyst, Steve Kay.

Beef Central broke the story in this item, first published last Saturday week, and since covered in this monthly column from our US market analyst, Steve Kay.

Our US market analyst, Steve Kay, from US Cattle Buyers Weekly, will offer his own perspective on the development in his monthly column in coming days.

Brazil has sought access to the US market for 20 years, but until now has been blocked due to Foot and Mouth Disease and BSE concerns.

Beef Central this week asked McDonald’s director of worldwide supply chain management, expat Australian Andrew Brazier, for the company’s initial take on the Brazil access developments.

Here’s our questions, and Mr Brazier’s responses:

Q: What implications, if any, are there likely to be for McDonald’s in sourcing of frozen 90CL?

A: McDonald’s supports local production for local markets where we can, Australia, Ireland and Canada are examples of this. But the reality is McDonald’s needs to source its beef from all over the world to meet our demands of a safe, assured supply of beef for our 70 million customers every day. Brazil, like Australia, is part of the solution that enables us to do that. Trading lanes open and close all the time, whether due to geopolitical activity, disease concerns and so on. I wont be looking to put all our eggs in one basket when it comes to sourcing options and we will continue to buy a significant portion of our beef from our Australian partners.

Q: Is Brazil likely to be added to the McDonald’s US suppliers list, at any time?

A: We already have a good number of abattoirs that are on the McDonald’s Approved List* in Brazil and supply various markets in Latin America and around the world with Brazilian beef. We have been sourcing from Brazil for the McDonald’s system for many years We don’t go into regions to look for short term opportunities. Our philosophy is to partner long term with suppliers that share similar values that support those all along the beef value chain while helping to meet today and tomorrow’s customer expectations.

*McDonald’s requires 3rd party audits of our raw material suppliers/abattoirs around HACCP/GMP, animal welfare, BSE firewalls to a global standard. So regardless of whether a facility is located in Australia, USA or Brazil we hold our suppliers to the same expectations.

Q: Does Brazil access represent a long-term threat to Australian supply to McD US? What about to other McD markets?

A: In general terms Brazil will continue to fight for access to markets with an Australia presence. China yesterday, USA today, Japan tomorrow? They are effective because they have government support and the industry is united and motivated. Specific to McDonald’s, we don’t view our beef supply chain as a commodity driven business. In looking for a safe, assured supply of beef we need long term partnerships with diversity in our sourcing regions. So we will continue to utilize and support Australian and Brazilian beef in our supply chain where we can. Our focus is on making sure that the McDonald’s business continues to grow, and with it, our beef volume requirements which benefits everyone.

MLA sees impact as ‘minimal’

Published below is a summary prepared by MLA about the Brazil market access development.

Somewhat unusually, it does not appear to rate the prospect that Brazil may in fact be prepared to pay the full 26.4pc duty to get considerably larger amounts of chilled/frozen beef into the US market, well beyond the 64,000t quota it will operate under.

THE US this week granted access for fresh and frozen Brazilian beef, following the determination that their animal health and food safety protocols meet equivalence with US standards. Brazil has sought access to the US market for 20 years, but until now has been blocked due to Foot and Mouth Disease and BSE concerns.

What does the decision mean?

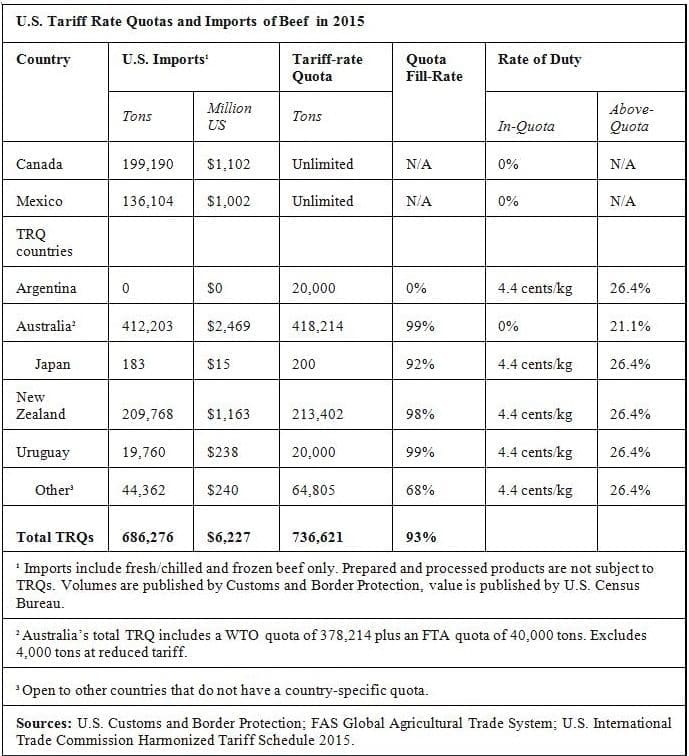

Unlike Australia, Canada, NZ, Mexico, Uruguay, Japan and Argentina (currently excluded from the market due to FMD), Brazil does not have its own country-specific quota for beef exports to the US. It will compete for access under the ‘Other Countries’ quota, currently totalling 64,805 tonnes. This quota is also accessed by countries such as Nicaragua, Honduras, Costa Rica and Ireland, and has not been fully subscribed in previous years.

Brazilian plants will need to demonstrate a commercially-acceptable lotting system for maintaining the independence and traceability of lots tested for E. coli. With subdued demand for imported beef in the USA this year, and the quota restrictions, these elements suggest volumes of Brazilian beef shipped to the USA over the remainder of 2016 will be modest. Brazilian authorities estimate 2017 will see up to US$400 million worth of Brazilian beef exports to the market.

The implications

While in the short-term exports are expected to be minimal, it is too early to speculate on the market impact of fresh and frozen Brazilian beef exports to the US market given the multitude of factors including Brazilian beef prices, US beef prices, currency movements, market demand and quota access. However from 2017 onwards Brazil expects to be a low-cost competitor to those countries, such as Australia, supplying lean manufacturing beef for further processing, including hamburgers, into the USA.

Depending on the relative impacts of Brazilian production levels, exports to other markets, US beef production, and currency movements, Brazil could ship product to the US out-of-quota, despite the 26.4% tariff. Uruguay has demonstrated this is feasible in the past, shipping more than their 20,000 tonne quota at times. However, with increased access into markets such as China and Saudi Arabia, it is not clear how much Brazil will seek to supply in addition to the ceiling placed by the ‘Other Countries’ quota allocation of 64,805 tonnes.

The countries most significantly and immediately challenged in terms of quota access will be those currently supplying under the ‘Other Countries’ quota, including Nicaragua and Ireland, although the former does have the potential to access additional amounts under Central American Free Trade Agreement (CAFTA), should the ‘Other Countries’ allocation be filled.

MLA’s trade communication, business development, and brand building activities over many years in the US will continue to keep Australia’s strong import position in good stead. Our focus on differentiating Australian product on the basis of provenance, food safety and quality assurance systems, traceability, meat quality, and sustainability will continue.

Australia and the US

Other than Canada and Mexico, which have free access under NAFTA, Australia maintains preferential access over all import competitors with an allocation totalling 418,214 tonnes in 2016. This comprises the WTO tariff rate quota (TRQ) of 378,214 and an additional 40,000 tonnes under the AUS/USA Free Trade Agreement which commenced in 2005. Under this agreement, Australia will effectively have free access to the US market from 2023 under the FTA when out-of-quota tariffs go to 0%.

Following two strong years of exports to the USA in 2014 and 2015, Australian exports are down 36% for the first six months of 2016, in line with reduced Australian beef production and increased US domestic beef production and lower prices.

However, Australia has increased its exports of chilled grassfed beef (as a proportion of total beef exports to the US) in 2016 to 20%, up from 17% in 2014 and 2015. This comes as a result of the dominant position we’ve carved out in the premium grassfed beef market in the US, boosted by collaborative and generic marketing of Australian grassfed beef by exporters, importers and MLA. Brazil is unlikely to be a meaningful competitor in this segment in the short term, due to Australia’s existing trade and end user relationships, and quality and perception issues.

The table below illustrates the different quota and duty parameters for a selection of countries.