Source: MLA. Click on images for a larger view

THE collection of co-products harvested as part of the beef slaughter process – sometimes called the ‘fifth quarter’ – have fallen sharply in value over the past couple of months, with conservative revenue declines of $50-$100 a head quoted this morning by an experienced export trader.

With a couple of exceptions, there have been significant declines in value in edible offals, rendered products like tallow and meatmeal, hides and pharmaceutical products since May.

Lack of demand out of China, due to challenging Chinese economic conditions, and currency challenges in other large offal markets like Japan and Korea are part of the reason, while the hides market worldwide continues to represent only a fraction of what it did up until the COVID period.

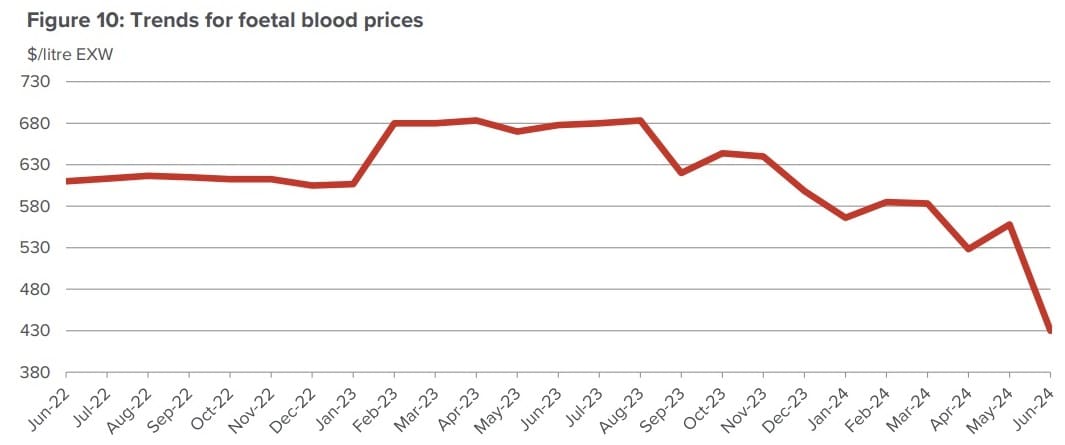

One of the worst affected co-products segments has been foetal blood, used for pharmaceutical and pathology work worldwide (and more recently, as a growing medium for the production of cell-based meat).

While the graph above is now somewhat dated, covering the period to the end of June only, the trend can be clearly seen. Foetal blood that was worth $680/litre this time last year was trading around $430/litre at the end of June, and even less in July.

“Demand out of China for foetal blood has really stalled,” an export commodity trader told Beef Central.

“Coupled with that, production of foetal blood across Eastern Australia had grown rapidly in response to earlier demand and prices, which has now led to oversupply,” he said.

“Coupled with that, production of foetal blood across Eastern Australia had grown rapidly in response to earlier demand and prices, which has now led to oversupply,” he said.

“Foetal blood, as it stands to day, is worth around 50pc of what it was only three months ago. Some foetal blood customers have come back to Australian processors recently saying they can’t take any product, at all.”

While foetal blood is perhaps the most extreme case, there are a basket of other edible and non-edible by-products where prices have come under price pressure.

Depending on whether a processor was harvesting foetal blood or not, recent declines in offal and co-product revenue could easily be $50 to $100 a head since the May-June period, and for some, that figure might be conservative, the trader said.

Prior to recent price declines, depending on whether foetal blood was harvested by a processor or not, the combined ‘fifth quarter’ revenue from an export animal could have been $250-$300 a head, or more.

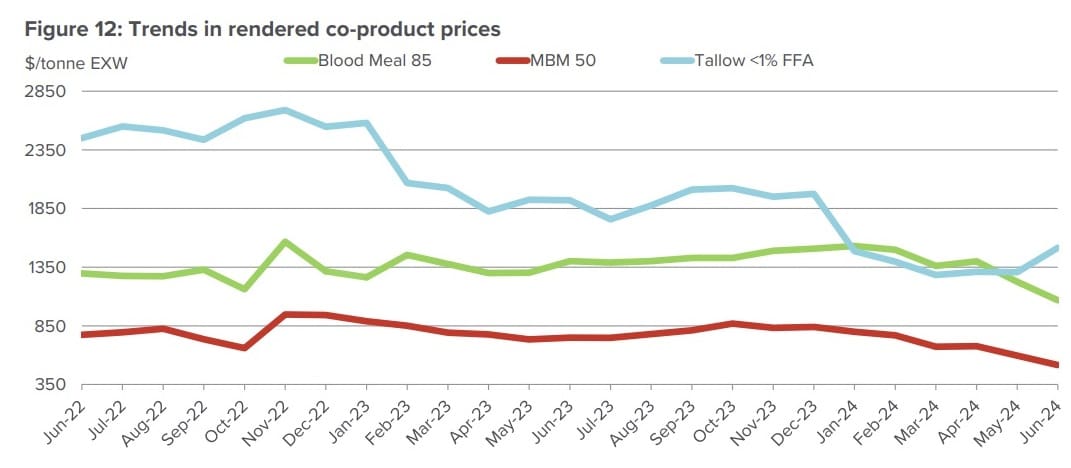

Rendered by-products like tallow and meat & bonemeal have also trended lower this year, with many items down 24-37pc over the past 12 months.

Tallow prices during July have continued a recent modest rise (see blue line in graph above) on the back of stronger demand out of the US, based on a slightly weaker dollar, and bio-diesel demand. But longer term, the price trend has been sharply down, falling from around $2600/t to $1350 in May, before recovering a little to to $1500 in June. However bloodmeal and MBM, also part of the rendering process, have softened further since February/March.

Tongues an exception

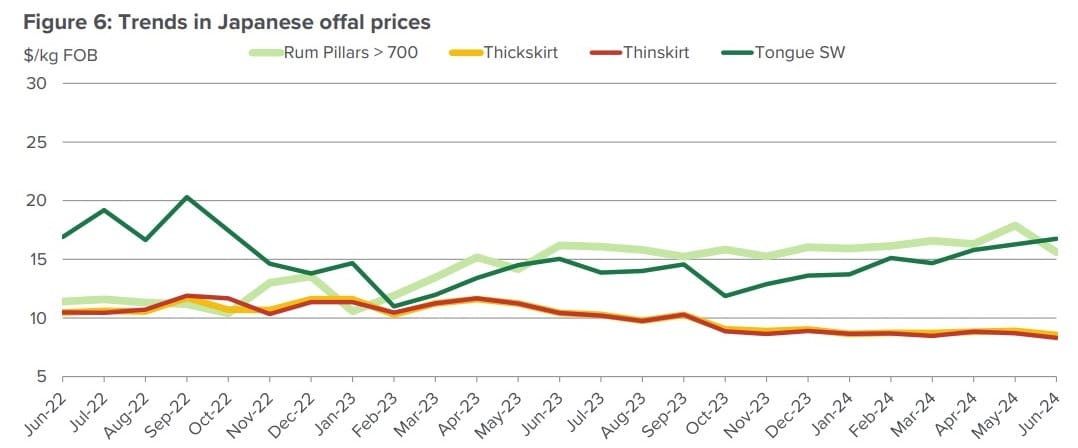

One of the few exceptions to the broader co-products trend is tongues, which are getting some traditional seasonal support from Japan’s yakiniku season and Korea’s Chosok festival period, the trader said.

The graph below shows tongues (dark green line) into the Japanese market rising about $5/kg FOB since October last year.

“There’s maybe another $3-$4 a head in tongue value at present,” the trade contact said. “Perhaps a little of that is now being reflected in declining supply to Asia out of the US for tongues and other items – much the same as for beef,” he said.

“But we are not really seeing the offset yet, in terms of price, because of the deflationary mode and low currency value in both Japan and Korea. While their cold storage stocks are being eaten away, we still expect to see both Japan and Korea come back a little more aggressively for both offal meat and muscle meat by the end of the year. Right now, they are still very quiet, but it might change by around September,” the trader said.

“As US supply starts to wane, Japan and Korea will need stock replacement. Prices may not get much firmer, but they could at least stabilise.”

“But right now, North Asian markets continue to say that they aren’t able to pay any more, with the weakness being seen in the Yen and the Won. And they still have the ability to offset beef items and offals with other proteins – it’s pretty apparent.”

The Korean market for thick and thin skirt meat, which is stronger than Japan, is still relatively flat – again impacted by currency movements making imports look more expensive.

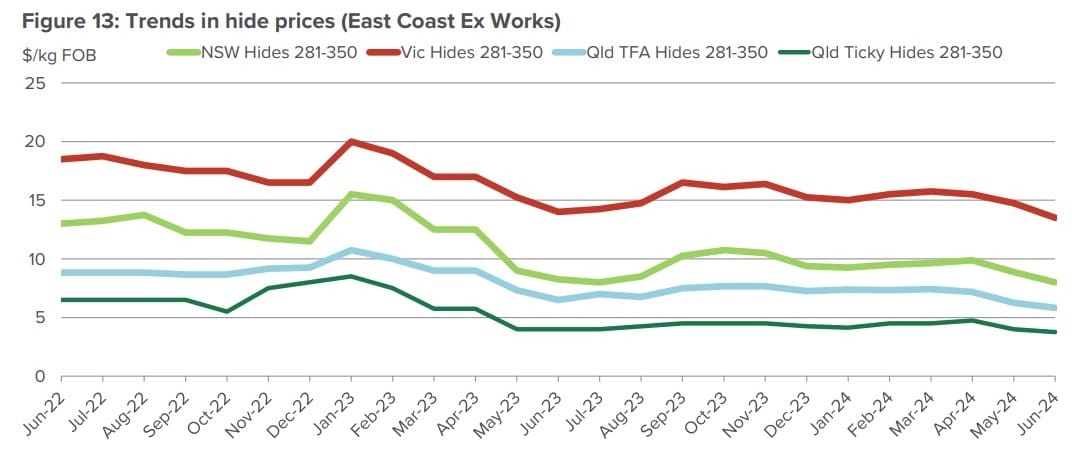

Hides a ‘basket case’

Beyond the edible co-products, hides values remain an “absolute basket case”, as they have since the COVID era. Click here to view an earlier article on the reasons why.

While prices back in mid-2022 in the graph below were already dramatically lower than in earlier years, they have continued to decline during 2024.

Good quality Victorian hides (tick-mark and scratch-free) that were worth $20 in January last year are now making $14, and ticky Queensland hides have slid to give-away prices between $3.75 and $5.50.

“To many processors, especially in the north, hides are now on the cost side of the ledger, not the income side,” the co-products trader said. “It costs more to dispose of them than they are worth.”

“For those players who do have small options for trading hides into China, the market remains very flat, sitting on very high stocks. European and US requirements are also very flat – at best – and that’s unlikely to change for the next six months, at least.”

Not too many years ago, Australian hides were making anywhere from $45 to $90 each, depending on quality and size.