Simon Quilty

Latest China market report by independent meat and livestock industry analyst, Simon Quilty

THE CHINESE government in recent months has adopted a number of important initiatives that will see larger import volumes of all food types from around the world, as the impact of African Swine Fever starts to be felt in tightening protein supplies and rising Chinese domestic pork prices.

China’s sow numbers fell 23.9 percent in May compared to a year ago, and total hog numbers fell 22.9pc year-on-year.

I believe these latest inventory figures point to increasing evidence of a much larger fall in China’s total swine inventory by year’s end, and in fact could be closer to 35-40pc rather than previous estimates of 30pc.

This revised rate of liquidation due to ASF is supported by other analysts who see this week’s increased rate of decline in the China sow population as concerning.

If we look to Vietnam as a more transparent ASF window of what is ‘really’ going on within China, and the losses incurred, Vietnam over three months has had a 2.2 million head loss out of its swine population of 34 million head.

Re-applying this rate of loss to China over a 17-month window from August 2018 to December 2019, it would be a 37pc loss – equivalent in China’s hog herd to 160 million head (see below on Vietnam update).

Other key indicators that also point to this bigger pork supply shortfall are:

- The 46pc decline in nurser/starter (piglets) feed ingredients for January to April period and

- Piglet prices 63pc higher than last year at 38.35 RMB/kg.

In other words, piglets are in short supply which all points to an emptying hog supply pipeline in China.

A recent report by the cleverly-named Dim Sums economic assessment (see below) states that Guangdong Province, China’s second-largest feed producing province, saw its swine inventory fall 40pc due to panic slaughtering of hogs due to the local severe ASF outbreak in February and March.

This liquidation remained high also in April and May indicating that the March hog inventory figure might be even lower today.

Some key initiatives in recent months that indicate China is building a bigger food import pipeline I have outlined in this report, and are as follows:

- Tariff exemption of food imports from the US, in particular for pork

- Expansion of approved countries and suppliers as China imports start to play a bigger role in managing the food deficit.

- Cold-chain supply expansion has commenced with a blue print for further expansion over the next four years.

Chinese Govt grant import tariff exemptions to agriculture companies and items

The Chinese Government sent out a directive in May inviting Chinese import companies to apply for 12-month exemption from paying the current 50pc import tax that has been imposed on imports due to the ongoing US/China trade war. This new China policy, I believe, is all about reducing the cost of US products and in particular US pork for Chinese importers and consumers.

The Chinese government has requested all applications to be received between June 3 and July 5 to apply for the exemption – for a wide range of goods including beef, pork, chicken, fruits, seafood and dairy products. In total there are in total 492 exempt items, and the list of agricultural items is extensive.

Applicants seeking tariff exclusion must submit documentation and commercial data describing how additional ad valorem tariffs on Chinese imports of US agricultural goods (1) face challenges seeking alternative sources of goods, (2) cause serious economic damage to the applicant, and (3) cause major negative structural impacts on the relevant industries or lead to serious social consequences.

This, to me, is one of many steps to be taken by the Chinese Government to start importing large volumes of US pork and any other protein products from the US to meet the expected protein shortfall due to African Swine Fever. The critical date seems to be July, and I would not be surprised if product on the water arriving in June and July will be exempt under this new import scheme.

China’s approval of processing plants is growing globally

China continues to expand its supply base globally for all proteins. The following table carries the latest list of approved facilities for each species. It should be noted that in many supplier countries, there are dual plants for both sheepmeat and beef. I have itemised these separately in each category and made a footnote below of number of dual plants in each country.

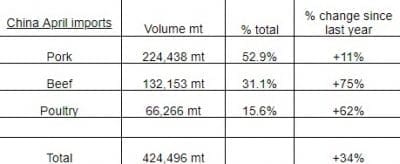

China’s success in widening its supply base is best reflected in the latest April import figures for China, showing the country’s ability to ramp-up imports when need be (see below).

Footnote: In some instances dual facilities may also include cold stores. Dual facilities are as follows: Uruguay has 10 dual beef/lamb plants, Brazil has 1 dual pork/poultry plant, New Zealand has 32 dual lamb/beef facilities, Australia has 8 dual beef/lamb facilities and Mongolia has 35 dual mutton/beef plants.

China’s import market responds

The benefits of this expanded global supply base is best seen in China’s April imports, with beef imports from all suppliers 75pc higher than last year, poultry up 62pc and pork 11pc higher.

What’s interesting to note is that the number of approved China global pork plants is almost the same in number as approved beef plants. This implies that beef imports are a high priority for the China government, and the April import figures reflect this sentiment as well.

China’s cold storage facilities expand

In February this year the Chinese government released a five-year blueprint to revitalise the agricultural sector by improving the quality of produce with a push for more cold-chain storage and logistic facilities over the next four years.

Beef Central wrote about the handicap on trade caused by lack of cold-chain infrastructure in China during this earlier marketplace visit.

The report highlighted the focus on constructing pre-cooling facilities, storage and freshness retaining infrastructure in key production regions. It also highlighted the need for government to work with logistics companies and encourage them to invest and build cold chain facilities, cold storage and refrigerated trucks.

According to recent statistics, China’s cold storage capacity in 2018 was 53 million tonnes, up by 10pc since 2017. Under the proposed government cold-chain blueprint, this pace of growth is expected to continue for at least the next four years and beyond.

Cold storage issues has been discussed for many years as one of the key problems with exporting to China, and in particular for chilled beef, lamb, pork and chicken. This proposed blueprint seems to recognise these shortcomings and is looking to address this problem.

Dim Sums report: ‘Differing ASF Impacts in Guandong and Sichuan’

Recent provincial surveys in China are showing ASF is moving at different pace in various regions. A survey done in May in Guangdong and Sichuan Provinces highlight these differences – both are key pork-producing and consuming regions, with Guangdon being the second largest feed producing province.

The Guangdon survey report highlighted that serious outbreaks occurred during February 2019 spring festival which led to panic slaughter and saw the severity of the epidemic peak in March and remain severe in April and May. It is estimated that Guangdon’s March swine inventory had fallen 40pc from a year earlier, double the national decline.

The Sichuan survey showed that ASF had less impact in this province, attributed to Sichuan’s remote location, mountainous terrain and small scattered farms. Due to the isolation, when an outbreak occurs the culling that follows in surrounding farms is minimal. In addition, strict biosecurity has also worked, and as a result the swine inventory decline is closer to 10pc. Sichuan backyard farmers reportedly had a 30pc decline in swine inventories while large farms had little change.

The Guangdong report said the widespread sell-off of pigs is the reason why prices have not risen. The Guangdong report also said panic slaughter of hogs has filled pork storage facilities to capacity in that province.

The Sichuan report says pork inventories are not as large there. There is concern that frozen pork inventories could contain the ASF virus. A Sichuan manager said testing of pork inventories ordered by the government has not started yet.

Some people say 90 percent of the pork held in inventory is infected, but a slaughterhouse manager interviewed during the survey doubted it is that prevalent. Infected pork will have to be destroyed, the manager said, since there is nothing else to do with it.

Comment: This is a very insightful report and I would recommend reading it. Some additional points I picked up were firstly, sows are especially vulnerable to ASF and in some districts sow numbers have declined as much as 60pc.

Secondly, heavy rain is a big contributor to the spread of ASF virus. April saw big rain through China and a noted increase in ASF transmissions. Thirdly, another dangerous period for spreading ASF is festivals with large people traffic moving throughout China and Asia, and it is no coincidence that the most serious outbreaks occurred during the Spring Festival in February this year (in China, Vietnam and North Korea).

I am also surprised by the Sichuan manager’s comments that testing of pork inventories had not started, and this in part could explain why domestic frozen pork stocks have not been moving quicker out of storage and the stagnant prices in recent months. The claim that 90pc of pork in inventory might be infected is surprising, but even if it is 50pc the fact it will be destroyed after testing highlights to me how precarious the next six months of pork supply in China will be.

To subscribe to this report send an email to Dim Sums: Rural China Economics and Policy

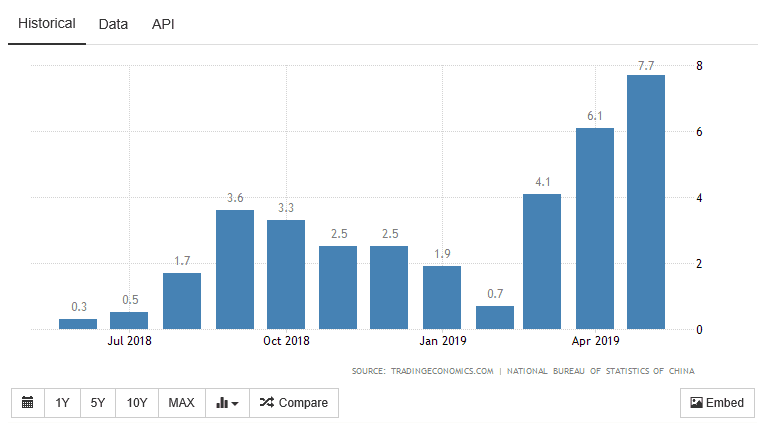

China food inflation moves higher in May

China’s food inflation in May jumped to 7.7pc which is the highest food inflation figure since January 2010. Fresh fruit and pork were the main drivers both up 26.7pc and 18.2pc respectively, compared to May last year.

In November last year Beef Central published my paper titled: “China’s rising pork prices are a headache today as they were in the past – managing social unrest.”

This paper looked at history and what the impact of Blue-ear disease was in China in 2006-2008, and in particular focused on rising inflation driven by pork prices, which saw retail prices jump more than 50pc and wholesale pork prices increase by as much as 95pc.

At the time, these rising pork prices fuelled inflationary fears that eventually led to higher CPI levels, and the need to look at importing food products as a means to lower domestic price. It’s no different to today.

Click here to view the paper I wrote last November – I believe it has more relevance today than 7 months ago.

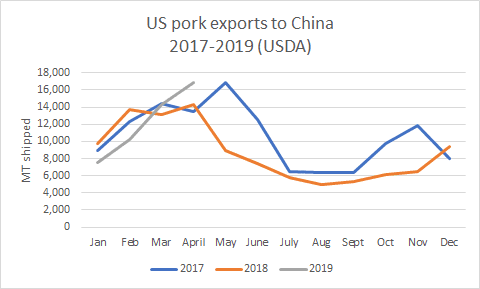

USDA pork export sales and shipments remain robust

USDA figures released this week have US pork exports to China at 2300MT, which is down on last week’s 17,400MT. The previous week was 39,200MT and 31,400MT four weeks ago.

Total forward US pork sales for the calendar year are 277,300MT, with 75pc of these pork exports occurring in April and May, highlighting to me a shift in China policy on US pork imports and its desire to increase imports regardless of the US/China trade war.

In comparison, the actual US pork shipments this year for January to April are 97,352MT which is down 26pc on last year, but the pick-up in April to me is an important sign that a China-driven pork export program from the US is possibly underway. Note: these figures do not include offals.

When I was giving the ASF seminars in the US in April, there was much talk among participants that a China pork import program was either about to commence, or had already commenced. These April figures tell me that it is highly likely that the early stages of an import program of some sort may have already commenced in April.

China looks to punish Canada

Chinese customs have increased inspections of Canadian pork due to the diplomatic crisis between the two countries, saying that pathogens in pork was the reason.

This is on the back of the arrest last December of the top Huawei executive who is being extradited to the US in relation to Iran sanction violations.

Earlier in the year China blocked shipments of canola into China as diplomatic tensions rose.

South Korea on high alert with ASF on its doorstep

South Korea claims that North Korea has ignored any calls for joint efforts to stem the spread of ASF, after an outbreak has occurred within North Korea.

South Korea’s agricultural ministry has been closely monitoring 340 pig farms near the North Korean border with blood tests being taken on all farms which returned negative results.

In an attempt to control the disease, South Korea has introduced large scale fencing and trapping around the region to prevent wild boars spreading the disease. It is estimated that 6300 pig farms exist in South Korea.

Brazil’s beef export ban to China is lifted

Brazil’s export ban on beef to China was lifted late Thursday last week, after a ten-day self-imposed ban after the discovery of an atypical cow with BSE.

The decision to lift the ban was after a series of meetings with Chinese authorities that concluded on Friday. Brazil officials said shipments would resume immediately.

China is the only country among Brazil’s buyers that enforces a health protocol requiring suspension of beef imports when an atypical case of BSE occurs. As a result of this recent ban, Brazil’s government will look to negotiate a new health protocol with China authorities to avoid export disruptions like what has occurred in the last 11 days.

In my view, China could ill afford to have Brazil’s ban remain in place given the importance Brazil has become as a beef supply country.

Vietnam ASF losses increase

Vietnamese officials recently reported that 2.2 million pigs have been culled due to ASF outbreaks with a total of 2332 ASF cases reported in 30 provinces.

In May the Vietnamese Army was mobilised to take part in efforts to cull infected pigs in a timely manner, in an attempt to keep the outbreaks from spreading further. The Minister for Agriculture said ‘Vietnam had never faced such a dangerous, complicated and costly disease in the country’s animal husbandry history’.

If Vietnam is the window into what has gone on in China, and given that Vietnam has lost 5pc of its total hog herd in 2.5 months due to ASF, it stands to reason that in China the potential losses in a 17-month period during August 2018 to December 2019, should this rate of loss be the same, China would have lost 37pc of its own herd.

Conclusion

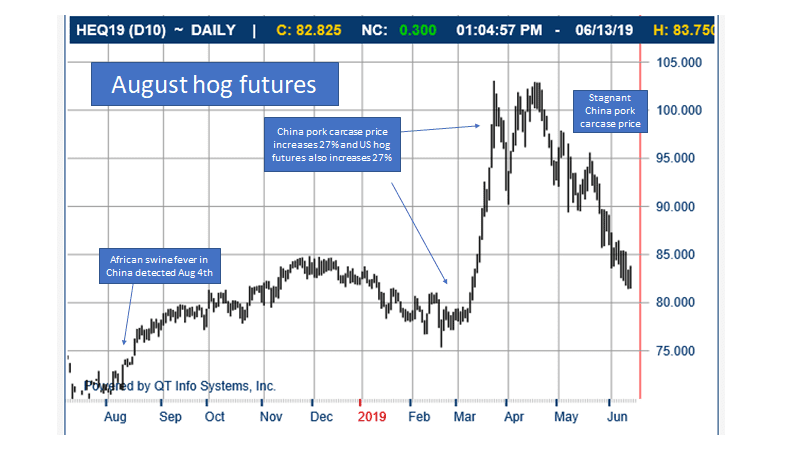

The elephant in the room is US hog prices and why haven’t US hog prices improved if all of the above factors are likely to lead to much higher US pork exports to China and a tightening of supply in the US hog market. Yet in recent weeks US hog futures have done the opposite and fallen.

I think the answer to this quandary is timing, and the fact that US markets had thought pork exports to China would increase a lot sooner. This is what drove the futures market much higher in February and March (see below).

Then, as the China pork carcase prices remained stagnant during April and May, it saw the US hog market losing momentum due to heavy US domestic production and the ongoing issues closer to home with Mexico and the tariffs imposed.

I think the US market is reluctant to make the same mistake twice and is waiting to see genuine follow-through in forward export pork sales, actual export numbers and a tightening of US hogs as pork is diverted to China. This has yet to happen.

The reason for the stagnation in China pricing is outlined above with increased China hog slaughter in February and March, large frozen domestic pork inventories that are being held in storage throughout China, and falling consumer demand for pork (estimated to be down 15pc).

To me, this in many ways changed a fortnight ago with China pork carcase prices starting to improve, which indicates falling supply. Hog kills have started to fall, and it can only be assumed that frozen pork inventories are starting to fall as well.

Some key aspects to watch in coming months:

- Once China’s government inspection and testing of frozen pork stocks occurs and if stocks are found to be ASF positive, it could lead to some sharp declines in frozen supplies as positive product is likely to be destroyed to avoid re-contamination occurring.

- The empty pipeline of pork supply has in some ways been masked by the larger kills and frozen inventories, but as these fall away and the China market looks for more finished hogs that no longer exist, it’s at this point that domestic pork supply could fall off a cliff. China monthly inventory numbers are critical.

USDA export pork sales are an important indicator, but it is widely accepted that they are not reliable. Actual pork shipments will be the truer indicator and unfortunately these have a six-week delay, so to me August is the critical month to watch in terms of pork price movements in the US as genuine US pork export be known.