WHILE the Australian beef industry sails into two or three years of dramatically lower beef production due to the effects of drought, other big ships in the world’s fleet of beef producers and exporters will more than compensate for the deficit.

As the graph below compiled by Steiner Consulting shows (click on image to enlarge), world cattle numbers are expanding.

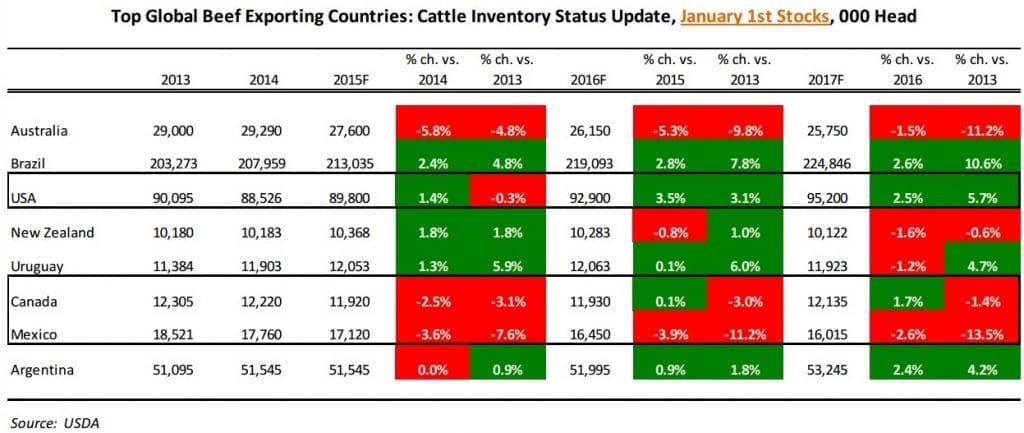

“Even as Australian cattle numbers are expected to be down in 2016 and 2017, supplies from other countries are growing and will more than offset the reduction in Australian beef supplies,” Steiner says in its latest weekly imported beef report compiled for MLA.

According to the US Department of Agriculture figures, the Brazilian cattle inventory as of January 1, 2016 will be up another 6 million head (+2.8pc) and then another 5.8 million head (+2.6pc) at the start of 2017.

United States cattle inventories also are expected to be up 3.1 million head at the start of next year as herd recovery gathers pace, and then expand 2.3 million head (+2.5pc) the following year.

In contrast, the table shows Australian herd size down 1.45 million head in January next year (-5.3pc year on year), and almost 1.9 million lower by 2017 (a further reduction of 1.5pc). Comparisons against 2014, when the herd size peaked at 29.29 million head, look even worse, back 11pc by January 2017.

New Zealand is also showing a small check in numbers next year, -0.8pc, mostly due to dairy herd reduction. Other significant exporters like Uruguay, Canada and Argentina are all forecast to rise between now and 2017. The only other country ‘in the red’ for the next two years is Mexico.

For the eight countries combined in the table, herd size in 2015 was 433 million, rising to 449m by January 2017 – a 4pc increase.

Source: Steiner Consulting, USDA. Click on image to enlarge

The increases in US and Brazilian numbers are important, as they come at a time when world demand appears to be softening, Steiner says.

“Lower crude oil prices have negatively impacted economic growth in a number of emerging/developing economies that rely on raw commodities for a portion of their incomes. Brazil has been shipping significant amounts of beef to China in the last two months and that trade is likely to expand in 2016,” it said.

Also, despite the timing remaining uncertain, Brazil could resume shipments of chilled and frozen fresh beef to the US market. The large herd and access to two new markets could allow Brazil to ramp-up its slaughter and exports in 2016, Steiner said. US authorities were reported this month to be visiting Brazilian beef plants as part of the pre-entry process.

Grinding beef prices still trending lower

In the US imported manufacturing beef market, prices continued to trend lower last week, as values for domestic lean grinding beef continued to plummet in the face of ‘extreme anxiety’ as to the outlook for US domestic fed cattle and beef prices in 2016, Steiner reported.

On Friday, MLA’s weekly report had 90CL frozen cow beef at US190c/lb, down from US277c/lb this time last year. In A$ terms, last week’s price was A589.4c/kg, down from A705c/kg a year ago.

“Volatility in US cattle futures is extreme as market participants lack any sort of conviction about short and medium run trends,” it said.

“As a result, even the smallest news (either bullish or bearish) is greatly amplified. Prices for cash cattle in the US market have been quite lower than earlier expected, and this has added to the bearish sentiment,” Steiner said.

Despite this trend, cattle futures were up sharply last week, largely on short covering activity.

The sharp decline in both domestic and imported manufacturing beef prices had left end-users with extremely expensive inventory on hand (and high priced commitments), last week’s report said.

“For now, end-users will look to work their positions down rather than book more meat. Market participants indicated that even though overseas suppliers talk about tighter future supplies and have reduced their offerings, they also are well aware of the dynamic in the US market and have lowered asking prices in order to keep product moving,” Steiner said.

It will be a few more weeks before plants in Australia and New Zealand shut down for the Christmas holidays. Reduced slaughter in Australia will tend to limit the supply of beef available in the US market.

“Still, the sharp decline in US domestic grinding beef prices for the moment will blunt some of the bullishness from overseas suppliers,” Steiner suggested.

“New Zealand and Uruguay will have quota available again at the start of the year and slaughter in both these countries has seasonally increased in November. We expect weekly slaughter in both NZ and Uruguay to ramp-up in the next four weeks and this will tend to keep imported beef values under pressure, at least for a bit longer.”