Taylor Byrne’s Townsville-based property valuer Michael Chaplain* provides this case study about the likely impacts and challenges of restocking in Queensland’s mid-western downs country after recent rain….

WHILE some grazing areas have still missed out, the recent widespread rains across large parts of Queensland, have left many, like me, stranded to the confines of their offices.

Given the circumstances, I thought it would be topical to conduct a small case study looking at the likely impacts for restocking with a switch for more favourable seasonal conditions after the prolonged drought (going on six years in some districts).

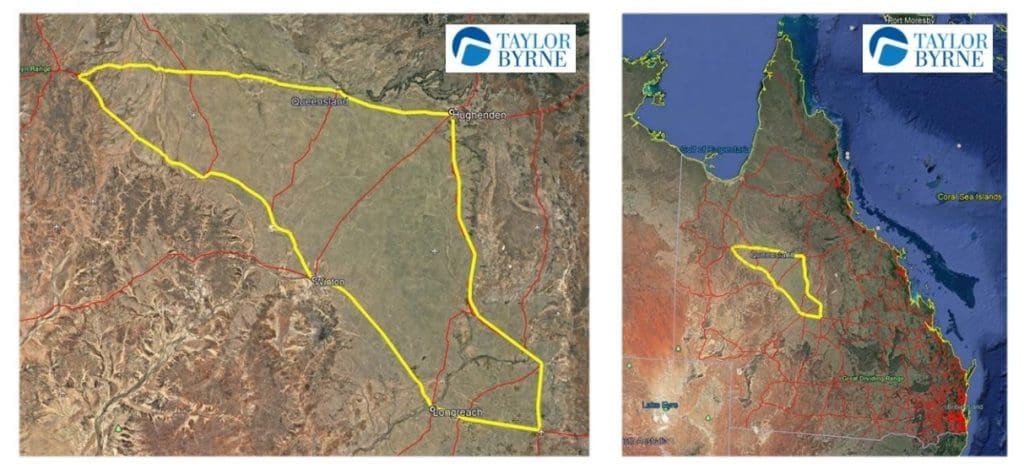

The area of Queensland I have chosen for this study is what I have referred to as the mid-west Downs region, in a rough triangle shape bordered by the Flinders and Landsborough Highways. The region encompasses areas from Hughenden in the north-east, across to Cloncurry in the north-west, and then back down to Barcaldine in the south-east (refer to map below).

Click on image for a larger view

The region in focus takes in an area of 6.1 million hectares (about 15 million acres) and consists of predominately open Mitchel/Flinders grass blacksoil plains which are broken by a few main channel systems and some areas of broken gidgee. This area has an approximate average rainfall between 400 and 500mm (16 to 20 inches), although since October 2012 this has been far less.

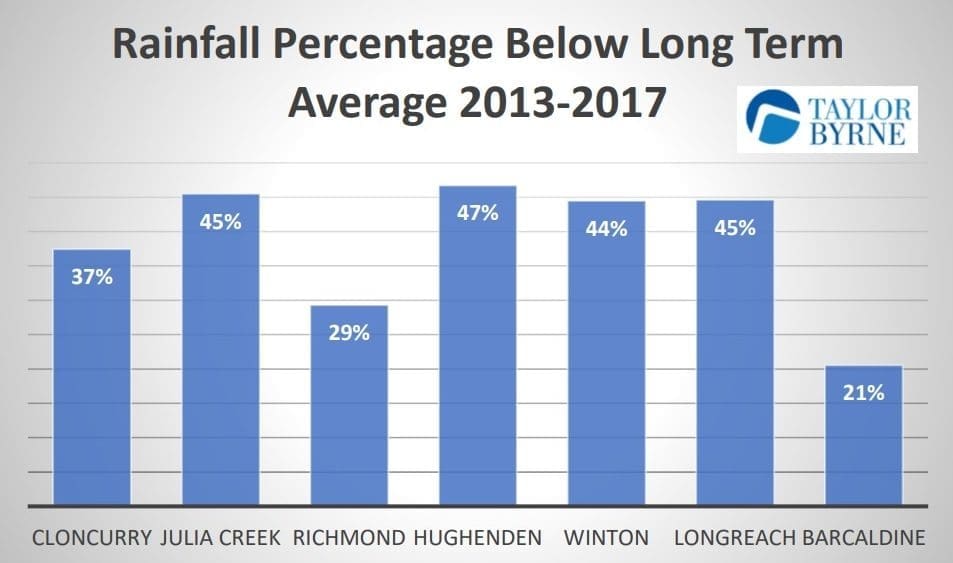

The graph below uses data from the Bureau of Meteorology and indicates the percentage below average rainfall in the past five years (2013-2017) for the study area:

Severe destocking

This area is now well under-stocked after herds have been sold off or relocated over this dry period. Many producers are now back to well under 50 percent of their long-term stocking rates, and many have completely destocked.

To provide a better understanding of how many head this might equate to, I have conducted a quick ‘back of the envelope’ type analysis in the hope that this might give some insight to the potential influence in the property market across this area.

To conduct this study I have made a few key assumptions. The primary one is the long-term average productive capacity of the area; and secondly a percentage reduction in livestock numbers under the long-term average, which could be referred to as a vacancy factor (percentage understocked), a term commonly used in reference to residential rental markets.

I have based my productive assessment on AE (Adult Equivalent – 450kg non-lactating beast at maintenance), although it should be noted that portions of this area are still used for sheep/wool production. Productivity: I have adopted a somewhat conservative stocking rate of 1AE: 10 hectares (25ac) for the overall stocking rate for the area. My calculations on this basis area are as follows:

Percentage Understocked (vacancy rate):

There is no hard data that I am aware of for how far under-stocked the typical producer is relative to their long-term average. Therefore, I have for the purposes of this case study adopted a vacancy rate of 70pc, recognising this may be generous given there are many properties which are entirely destocked. However, this percentage does seem generally supported by conversations with industry stakeholders including stock agents and accountants.

Based on these calculations, this area will be understocked by about 430,000 head, which is a somewhat alarming number.

To put this into perspective, this represents more cattle than Roma saleyards – Australia’s largest selling centre – sells in an entire year. We understand some producers in the study region will have additional breeder country located further north where they can draw replacement stock from, and others will have cattle away on agistment. However, the majority of producers do not have any cattle up their sleeve to restock with, leaving them in somewhat of a restocking conundrum.

In my view, some of the more likely scenarios would include:

- Total buy-back – requiring significant capital outlay and likely be at near record prices

- Partial buy-back and breed up – requiring less up-front capital, however recovery time is longer. This may also be paired with agisting balance land out for additional income

- Sit back approach – sit back and let the stock market cool for 12 months, and then buy back in. This will also give time for land/pasture recovery. This may not be an option for producers who are not in a position to go another extended period with no income

- Full lease/agistment – lease or agist the entire property out as a way of producing immediate cashflow.

So how does this relate back to the property market? Well, if we refer back to our vacancy factor of 70pc (equating to about 430,000 head), it is very unlikely that all these ‘vacancies’ will be filled in the next 12 months – remembering this is only a small sample of the drought impacted land at present.

Based on the scenarios described above, it will be some time (likely three or four years, in my opinion), before we see this vacancy rate drop back considerably. Therefore, simple supply and demand economics come into play: if vacancy rates are high, typically rental values (agistment rates) decrease; if rental rates decrease, returns decline and so the flow-on effect continues.

Therefore, if the above comes to fruition, we expect to see a softening of agistment rates, relative to longer-term average prices, as opposed to some of the inflated, demand-driven ‘drought’ rates which are currently being paid.

Tough pill to swallow

This will be a tough pill to swallow for many producers who had to sell-down at depressed prices during the dry times, and now receive less income while cattle prices are moving back towards record highs.

It does, however, represent opportunities for other producers who can agist land at an affordable rate, which may help to offset the high purchase price on stock.

The information above has probably only provided support to what most people most likely already knew.

Property market impact

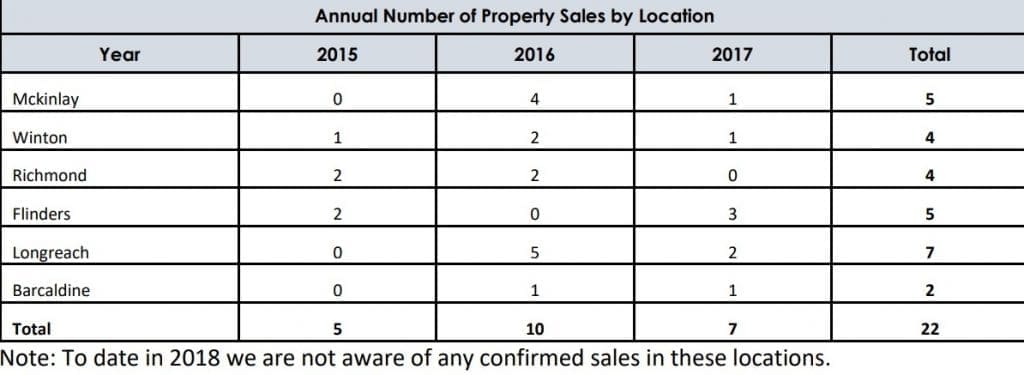

So how is this likely to impact the property market in terms of sales and values? I have extracted the market data over the past four years for the case-study area. This data indicates a total of 22 sales, equating to an average rate of 5.5 sales per year. Again, this market, as with any market, will be impacted by simple supply and demand factors. The rate of 5.5 sales per year in recent years has been absorbed by the market, with values remaining relatively stable.

Click on table for a larger view

The general consensus is that there will be a backlog of properties that have been held back from market due to poor marketability resulting from little or no feed reserves. The rate at which these properties come to market will impact on the absorption rate.

Furthermore, who will the buyers be? Given the high amount of ‘vacant land’, it is unlikely local buyers will be looking to acquire additional land until their current land is filled. Therefore, the majority of buyers will need to come from outside of this area.

This has already started to become evident with a number of the most recent transactions being to non-local Central Queensland buyers. The dramatic increase of land values in Central and Southern Queensland may see buyers from these regions look to the subject area to secure more affordable assets.

No doubt there will be some landowners which have no choice but to sell in order to pay down debt. The way in which these customers are managed by their financiers will likely play a pivotal role in how the market reacts, but it is essential that a strategic and cohesive approach is adopted in these cases.

It is important to highlight that the impacts of this drought stretch far beyond the sample area identified in this study. However I do believe the general market forces mentioned above will be similar across Queensland.

Although these are somewhat unchartered waters, I believe there is light at the end of the tunnel (or rainbows on the horizon) and as with any market, there will always be opportunities for some prudent operators.

* Michael Chaplain is a rural property valuer with Taylor Byrne, based in Townsville. He can be contacted by email here.

Taylor Byrne commenced operations in 1960 in Brisbane and since then has continued to expand throughout Queensland and NSW. The company has 25 offices, with 14 in Queensland and 11 in NSW, making Taylor Byrne one of the largest single entity valuation firms in Australia. It provides a full range of valuation services and is recognised for its strength in litigation and acquisition, mortgage security, family law and asset portfolio valuations.

Mick – good article.

Drought depletes primary producer’s disposable capital which limits produce and property price appreciation when it rains. Recovery takes more than one rain event.

Pretty accurate assessment Michael. Being mostly unstocked or at low stocking rates there should be ample time for pasture to regenerate and drop seed in most cases. A lot of people including us are looking for agistment unsuccessfully as landholders are waiting for a good growing season first

Interesting reading, but having traveled this area for the past seven years or more, feel the most important point is being missed, and that is that the grasses on these black soils need a rest to come back to some form of sustainability. Feeding them down now will be hard not to do after all these years of bare ground, but the long term effects of doing so could be devastating.

In absolute agreeance, and being in the sheep industry, I can’t see why this won’t apply as well!

I believe Michael Chaplain has summed the situation up very well!

This is a very accurate article on the current state of play.