Large scale cattle upload on Wave Hill last year

OVER 29 years of ownership, was the revered Wave Hill/Cattle Creek aggregation in the Northern Territory a good capital gain investment for vendor, Western Grazing?

As outlined yesterday, a syndicate led by Jumbuck Pastoral Co has paid $104 million for the Victoria River district properties, totalling 1.25 million hectares, together with 40,000 cattle.

Beast area value

In the wake of yesterday’s result, people have been doing some back-of-the-envelope sums on what the deal represented in beast area terms, and capital appreciation over the 29 years that the holdings were owned by the Oxenford family’s Western Grazing.

First-glance sums suggest the sale price, minus cattle value (40,000 cattle @ $1100 = $44m), represented a land-only beast area value of $1090 (when measured at the ten year average herd size of 55,000 head), and $1200 at a more conservative 50,000 head stocking rate.

Both figures can be considered relatively attractive by local VRD standards, Beef Central was told, but beast area value inevitably declines the larger a holding becomes, and the aggregation includes a large area of very light-carrying desert country. As a comparison, some good quality VRD country in smaller parcels sold last year closer to $1400/beast area.

Capital gain

Following yesterday’s item, we’ve looked into the historic sale records of the Wave Hill aggregation, and come up with a few interesting (we think) conclusions about adjusted land and cattle value.

Ignoring operating profit and capital improvements, and looking simply at the gross value adjusted for cattle numbers, the aggregation appears to have shown an average annual value return well above the norm for the extensive northern pastoral zone.

First, some history. The late Brian Oxenford bought the Wave Hill/Cattle Creek aggregation during the dispersal of the Vestey’s pastoral empire in 1992. The properties were passed in to him at auction for $8 million, having failed to meet the reserve, and were subsequently bought for around $15 million.

Being a private person by nature, Mr Oxenford was not present in the Brisbane hotel auction room at the time. Instead, it is said he rented a hotel room upstairs from the auction room, and had one of his office staff attend, telegraphing his bids by phone.

Click twice on image for a larger view

Given that 29 years has now elapsed since that purchase, did Wave Hill/Cattle Creek prove to be a good investment? For the purposes of this item, we are ignoring trading profit and capital investments on improvements, and focusing solely on capital gain on the land asset and cattle.

It’s hard to remember what northern cattle were worth back in 1992, but it’s likely good breeders were making no more than $300/$400 a head.

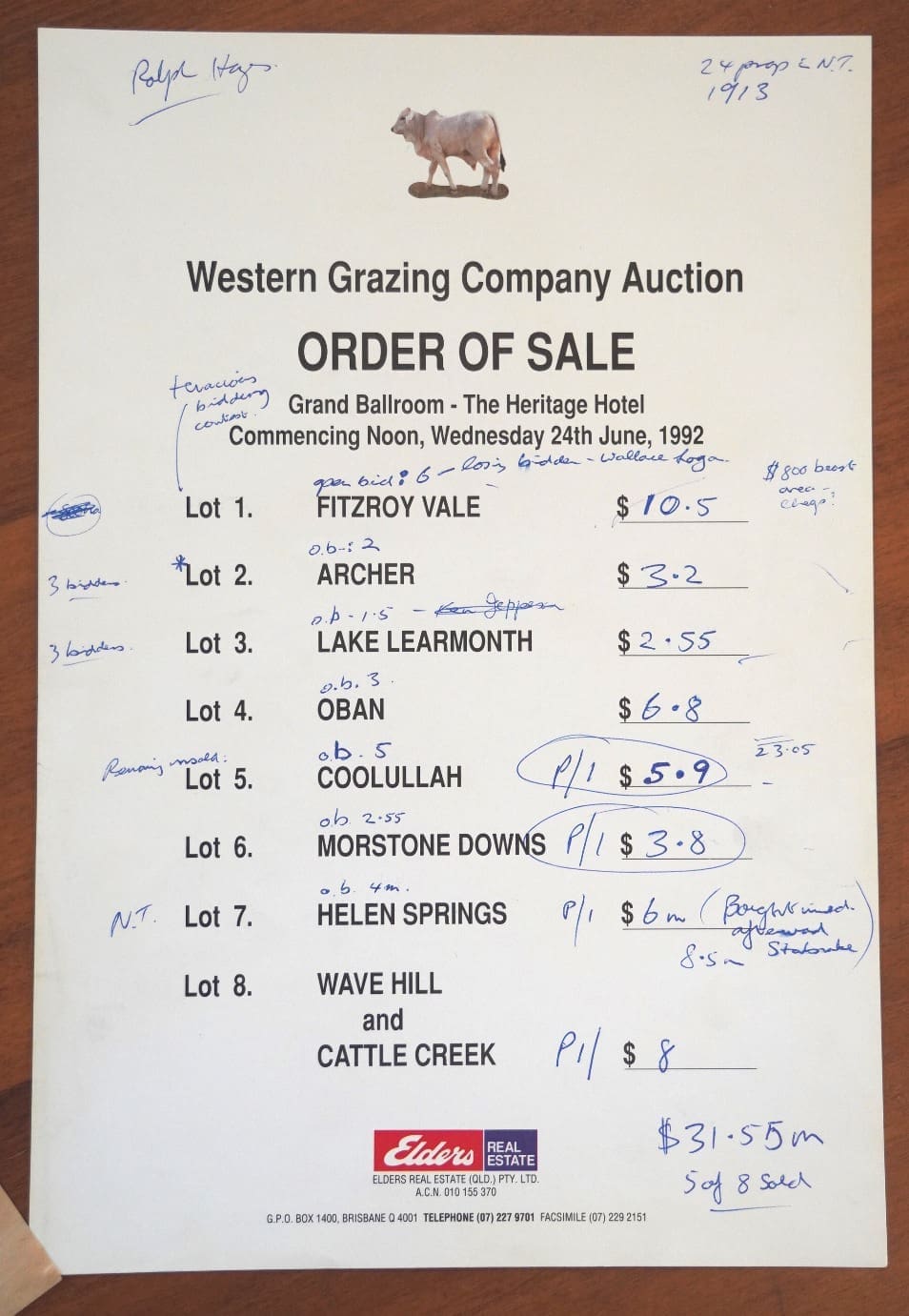

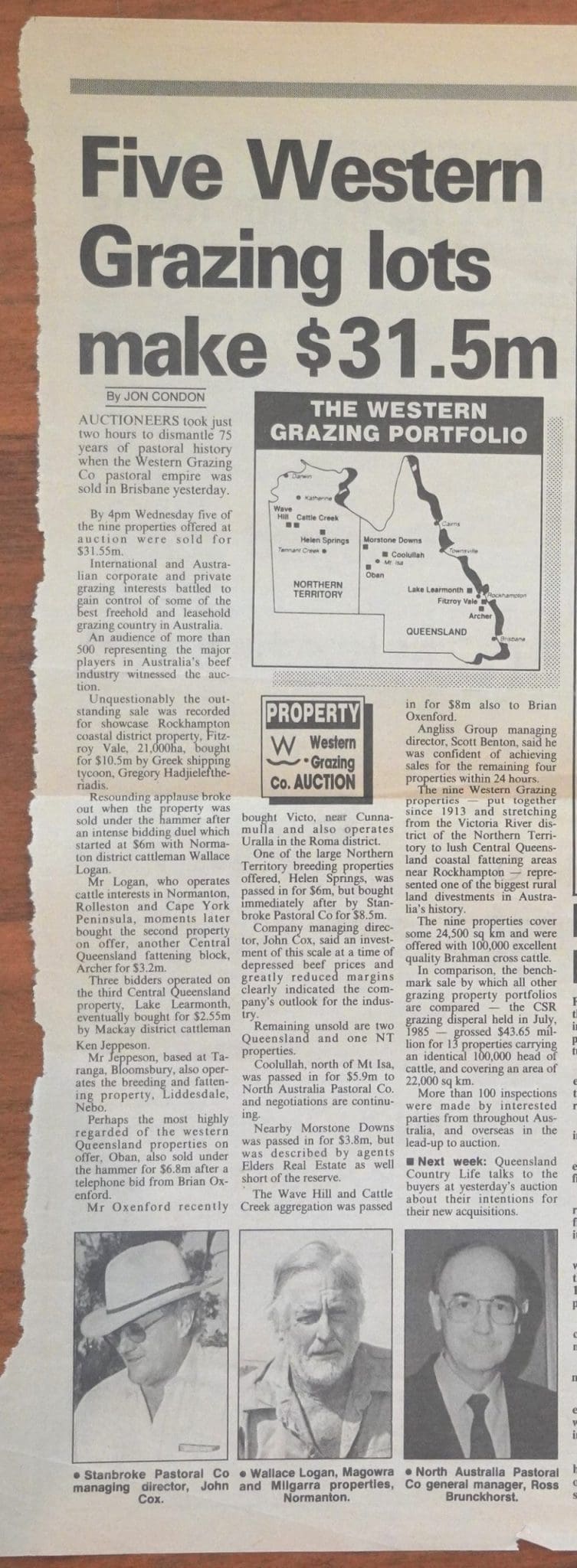

The 1992 purchase of Wave Hill/Cattle Creek for $15 million represented an enormous amount of money for a cattle property at the time. It was easily the most expensive of the eight showcase Vestey’s properties offered on the day (see image), finishing well above Fitzroy Vale, near Rockhampton, which sold for $10.5 million.

Click twice on image for a larger view

Sale records showed that the combined Wave Hill/Cattle Creek holdings were sold in 1992 with some 28,000 head of Brahman cattle, mostly breeders. The relatively low herd count may have been due to the fact that the BTEC disease eradication campaign was still in its final stages.

Yesterday’s sale story references 40,000 head of cattle included in the $104m sale to the Jumbuck syndicate.

Estimated carrying capacity of the aggregation back in 1992 was 35,000 head, compared with the 57,000 head the properties have run on average over the past ten years (at least prior to the 2020 drought).

Worth noting from the 1992 sale literature, vast areas of both properties were in fact unfenced at the time. The southern half of Wave Hill, for example – roughly 2700sq km – had no fences at all, not even boundary fences. Waters at the time included 62 bores, compared with 76 equipped bores referenced in yesterday’s story.

There’s obviously been substantial capital improvement investments made in the years since then, especially in fencing and herd control, waters (particularly poly pipe) replacement of mills with solar pumps and motors, additional sets of yards, and genetics. It’s impossible to price those into this simple calculation, but improvements seen during the recent sale process were described to Beef Central as ‘adequate’, without being ‘excellent.’

To try to make a more direct price-change comparison, we’ve deducted $13.2 million from yesterday’s sale price, reflecting the 12,000 head difference in herd size between 1992 and now (valuing the herd at $1100/head).

Ruling out productivity improvements and a host of other factors that contribute to a property’s true net worth, that gives an adjusted sale price yesterday of $90.8 million, suggesting the land asset and adjusted cattle numbers have increased by $75.8m over the past 29 years, or an average of $2.6 million a year.

On a $15 million investment back in 1992, that looks to be an exceptional result, and more than anything, reflects the massive change in northern cattle values, and by extension, land values, during the live export boom years that have followed.

- Scroll to bottom of page to read reader comments.

Just a couple of things not yet contemplated;

1) The land itself (Wavehill) is not Freehold, its only rented from the NT (the State). It is not crown land (see s 132 Pastoral Land Act)

2) The purchaser paid at least the Freehold value for the land; as Michael says below $20.27 per Acre.

3) Since 1992 major changes have occurred which has changed the equity value of rented leased land in the NT i.e. Native Title

4) In March 2019 the High Court (set out in Timber Creek) see the Court Orders;

http://eresources.hcourt.gov.au/downloadPdf/2019/HCA/7

At section 3(1) see that the “the objective economic value of the non-exclusive native title rights and interests of … is 50 per cent of the freehold value of the land”

5) That means in Law the NT, in equity terms over its “Pastoral Estate”, the value of its rented land that forms the pastoral leases, is now only 50% of the Freehold value of the land.

I think its a mistake to value Rented land that is subject to Native Title as you would Freehold land, particularly when the Lessor of the Land (the NT Gov.) onlty holds a 50% equity in the land they are renting to the Lessees.

I am wondering if the parties involved here have considered these facts?

Rod, I agree …

A few short comments:

a) A 6.91% pa compound nominal return; not accounting for inflation. Thus, the real return is less …

b) An implied average farm-gate price on the hoof, of around $1,094 per head sold.

c) An implied walk-in, walk-out BAV of around $1,816.

d) An implied land-value (bare, but improved) of around $20.27 per Acre.

e) An implied premium above long-term fundamental value for the going-concern operation (with all things necessary), of around 20%.

A fair investment price was paid for size, location, and quality of the asset; and whilst taking a long-term view.

Congratulations to the Vendor and the Buyer(s).

May the seasons stick with you …

IMO

A fair assessment Jon. You would recall of course, that it wasn’t until the mid nineties when Live Export values caused a dramatic readjustment of pastoral leases. Prior to this and BTEC, properties were basically valued on the hooves on the lease. Improvements, weren’t even considered. cheers, David Heath

$15M invested for 29 years to yield $90.8M represents a compound interest rate of 6.4% p.a.

Many thanks for doing the sums, Bob. Editor

Firstly I congratulate the late Brian Oxenford & his family on a great business decision back in 1992.

As former pastoral manager for Vesteys, a couple of points:

Wave Hill/Cattle Creeks’ cattle numbers were below optimum in 1992 due to a poor season in 1991 and a failed wet season in 1992, with the sale conducted June ’92. Numbers had been reduced considerably in the previous 18 mths. At time of sale both stations were well clear of BTEC and confirmed free of both TB & Brucellosis.

It is interesting that stock density/bore has increased from 565 to 750, perhaps reticulation away from bores has allowed this.

Interesting points that add some historical context, Bill – thanks for your contribution. Editor

Approx. 7% annual compound growth? Sustained over 30 years, despite season and market turbulence, it’s been a good safe investment. That’s on the very likely assumption the operations have been cash positive. The MacLachlan Family are patient experienced operators and in the Millers, have retained very respected and experienced management. A good combination for success.

The sad thing is that not enough of the investment community and superannuation funds have recognised the value of agriculture in recent times. There is about $3 trillion in superannuation today, which is a long term investment for many Australians, much of it invested in low yielding bonds and shares. If fund managers understood agriculture there would be little need for overseas ownership of agriculture assets.

Agree

I agree totally Val.

It is not the lack of understanding by Superannuation investors that is the problem. It is the hindrince of legislation. At all times industry funds must have a certain percentage of liquid assets that can be accessed I think! within a few days if required. Therefore long term land investments rarely meet their criteria. SMSF’s on the other hand are only allowed to own real property and have all sorts of hoops and requirements in owning land and leasing back including that the asset needs to be revalued every year for Market value purposes.

I don’t believe that current land prices actually reflect true productivity values of what properties are capable of when taking into account seasons, cattle market fluctuations. Too many current property purchases I believe are based on the premise that resale will always be higher than current pricing. Interest rates may stay low for a period, cattle prices I think will stay up in the 80% + percentiles but neither will stay that way or stable. Interesting times ahead!