WHAT it costs a beef producer each year to operate their property, per animal unit, has a big impact on the bottom line.

The cause of a less than desirable profit per beast (adult equivalent or AE) will either be attributable to low income, high operating costs, or both.

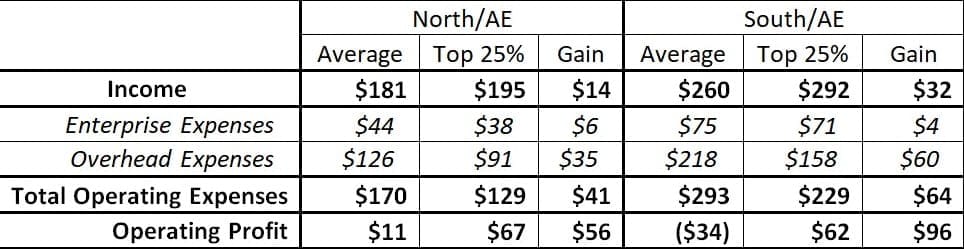

The table below presents the Average and Top 25 percent income, operating (enterprise and overhead) expenses, and Operating Profit (Earnings Before Interest and Tax, EBIT) per animal unit for specialist beef producers in Southern and Northern Australia, drawn from The Australian Beef Report, published earlier this year.

The results show that for both the Northern and Southern Australia, the difference (gain) between the Average and Top 25pc EBIT lies mostly in total operating expenses. This demonstrates that the performance of the average is limited by high operating expenses when compared to the top performers in both regions. This is primarily caused by the average being limited by lack of operating scale.

Even the most productive herds will struggle to generate sufficient income to overcome total operating expenses of greater than $200 per AE. If total operating expenses are this high, the immediate thought is to begin cost-cutting, but it is not that simple.

A good understanding of what drives operating expenses is required if costs are to be reduced without compromising productivity and income.

The operating expenses are best understood if they are divided into enterprise and overhead expenses. Enterprise expenses are those that are spent directly on herd-related activities such as vaccinations, mustering, and supplementation. Overhead expenses relate to the general operations of the business such as administration expenses, fuel, and wages.

The Australian Beef Report provides detailed information on the cost structure of specialist beef businesses from across Australia which can be used to understand the cost drivers of beef businesses.

Better performing herds generally have lower enterprise expenses than the average, indicating targeted and effective expenditure on the herd.

However there is more variation in overhead expenses than in enterprise expenses. So, if a business is limited by high operating expenses, it is normally overhead expenses that are the major problem. This is shown in the table above, where overhead expenses are the biggest distinction between the Average and Top 25pc for both the North and South.

Overhead expenses are governed by operating scale (average number of AE run) and labour efficiency (average number of AE run per full-time equivalent employed).

The effect of operating scale follows the ‘economies of scale’ principle, whereby costs per unit of output decrease with increasing scale. In other words, the general running costs of a beef business such as checking waters and running the accounts are spread over more animal units, making each animal unit cheaper to run.

It is important to note that the relationship is initially very steep, before flattening. That is, the benefits of increasing scale are initially great, but are exhausted when a scale of around 2,000-3,000AE (17,000 – 25,000DSE) are reached.

Most producers operate well below this, as 49pc of specialist beef producers in the North and 84pc in the South have less than 800 head of cattle. The issue of operating scale is discussed extensively in the Australian Beef Report as one of the two barriers to profit for beef businesses.

Labour-related expenses account for more than 50pc of expenses in all beef businesses. The cost of labour has tentacles that reach far beyond wage expenses. Workers (owners or employed) drive vehicles that use fuel, incur wear and tear, and have to source materials to fix the wear and tear.

Analysis of the Australian Beef Report data shows that each labour unit adds $120,000-$140,000 to the running costs of a beef business, with only around half of this as the wage component. Labour efficiency of around 1,500-2,000AE/FTE (12,500-17,000 DSE/FTE) is required for a beef business to have a competitive cost base.

Scale and labour efficiency are intertwined, as smaller businesses tend to be less labour efficient. Scale is essentially fixed and may not be feasible to change depending on individual circumstances.

Labour efficiency isn’t as fixed, but improvement may still require some capital outlay in the form of labour-saving technology. If we consider an example of an 800AE business, then only 0.53 full-time equivalents, or one person working approximately 127 days a year, could work in the business if the labour efficiency target 1,500AE/FTE is to be achieved.

If a business is under-scale, the most effective approach to reducing overhead expenses is to improve labour efficiency by treating it as a part-time pursuit.

Strong beef businesses are characterised by high income driven by productivity, and competitive costs. As discussed, the two barriers to competitive overhead costs are operating scale and labour efficiency. You cannot effectively starve profits into a business by cutting costs, in fact there aren’t usually many costs to cut in beef businesses.

Ensuring your herd expenditure is well targeted and improving labour efficiency are the main options available.

The Australian Beef Report

The Australian Beef Report details the current performance of the industry and what profit focussed producers can do to improve their long-term performance.

The Report is a valuable, independent study of the Australian Beef Industry that will open readers’ eyes. Authors Ian McLean and Phil Holmes have identified that the industry can be effectively broken up into two groups, the Best and the Rest. They have also identified that there are only two basic barriers to profit, and how to address these barriers is spelt out very clearly in the report.

Hi John and Ian

It is quite easy to show that a profitable pasture development in northern Australia can have lower profit per AE than profit per hectare. The application of the profit per AE measure alone would suggest many pasture developments are unprofitable, when they are likely to be quite profitable. Focusing on profit per AE can be equally as misleading as focusing on profit per hectare. Neither measure is all that useful when looking at the future direction of a beef property. Profit is maximized in the short term in northern beef production systems, as it is in all livestock production systems, at the production level where the marginal costs of extra output is almost equal to the price received per unit of output. This analysis is more time consuming and complex than a gross margin analysis but there are free models available from DAF that allow such analyses to be undertaken and this process is much more likely to identify the most profitable direction for a northern beef producer to target over time.

Fred Chudleigh

DAF Queensland

Hi John,

I agree that for southern systems profit per hectare should be the primary focus.

However in northern systems, where overgrazed pastures cannot easily be replaced or repaired, stocking rate is capped by long term carrying capacity. Therefore the animal unit should be the fundamental unit of measurement. Profit is northern systems is maximised when profit per animal unit is maximised.

The other advantage of expressing data on an animal unit basis is that we can compare across all regions of Australia, as we have done in the Australian Beef Report, this can’t be meaningfully done on a per hectare basis.

Regards

Ian McLean

Bush AgriBusiness Pty Ltd

We should be concerned about profit per hectare not per animal.