Simon Quilty

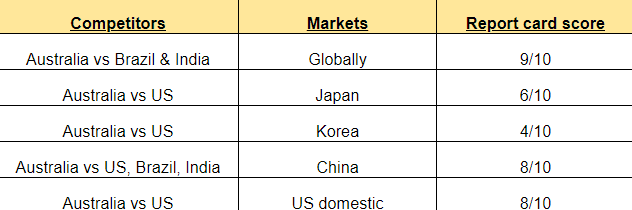

Independent global beef industry analyst Simon Quilty provides his ‘report card’ on Australia’s performance in the premium international beef markets, relative to major export competitors, the United States, Brazil and India. His scores range from a low of 4/10 in Korea, to 8/10 in China…

GIVEN the drought that’s been experienced across much of eastern Australia, the high cost of feed and the higher rates of slaughter, one of the challenges this year has been the competitiveness of Australian beef exports globally.

The following is a report card of how Australia is faring against our three biggest export competitors – the United States, Brazil and India – in the key customer markets of Japan, Korea, China and the US.

The loss of market share to the US in Korea and Japan, outlined in detail below, I believe is no fault of Meat & Livestock Australia, Australian exporters or producers. Instead the ‘die was cast’ on Korea when the US negotiated a favourable Free Trade Agreement in 2007, which came into effect in March 2012. It was the Australian Government and trade minister at the time who dropped the ball, which resulted in the loss of market share being experienced in Korea today.

In 2014 when Australia’s FTA into Japan came into effect, it was hoped that this would offset the Korean FTA impact, in terms of market advantages over the US. But in reality, this has not occurred.

Japan importers have passed this cost forward to the Japanese consumer, and the market today is willing to pay a premium for US beef over equivalent Australian beef. When this is combined with the loss in market share and pricing in Korea, the net effect is a fall in Australia’s global export value by 13pc, compared to the US.

In brief, the key findings of this report, outlined in more detail below, are:

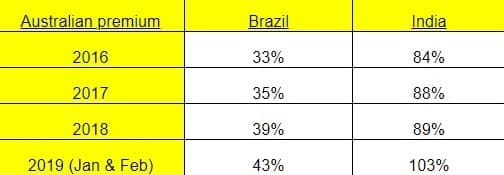

- Australia maintains a growing competitive advantage over Brazil and India, with Australia’s average export price gap increasing in recent months to 43pc and 103pc respectively over these two rivals.

- India’s buffalo beef exports into China via the grey trade has slowed, forcing cheaper India beef into secondary markets it shares with Brazil, which in turn has lowered Brazil’s prices.

- Like Australia, Brazil still enjoys strong export growth into China – this trend looks likely to continue.

- Australia I believe has lost significant market share in both Korea and Japan compared to the US. This has seen Australia’s average global export price fall from a premium in these markets four years ago compared to the US to a 13pc discount this year. I believe tariffs in Korea, the displacement of Australia’s beef in Japan and Korea due to large US export beef volumes, and Japanese consumer preference for US product have been several factors contributing to this negative price differential for Australian beef.

- Australia and Brazil dominate China exports compared to the US, due to China’s no HGP requirement, cattle traceability and minimum duties.

- Australia and New Zealand beef trimming is likely to trade at a premium for the majority of this year on the US domestic market.

Summary of Australia’s global export report card – how are we faring?

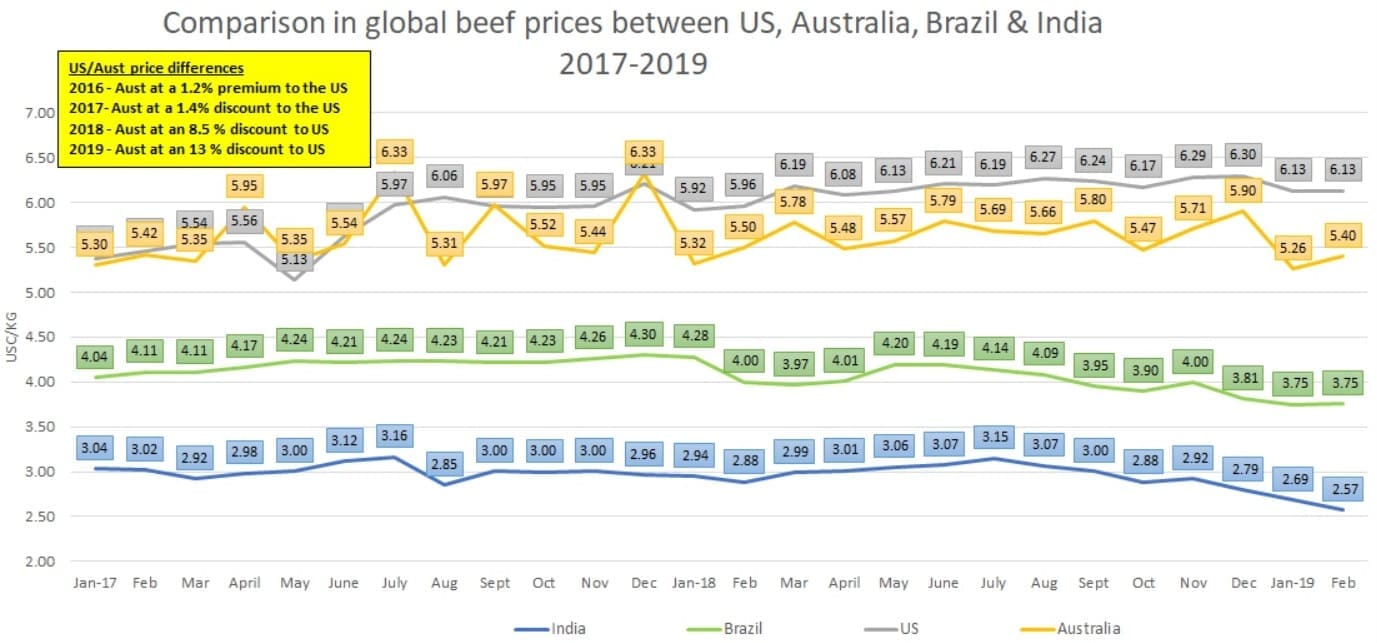

When looking at the value of Australian beef exports compared to our competitors, Australia and the US have remained consistently higher than India and Brazil in terms of global export price per kilogram, measured in US dollars. But what is concerning for Australia is that we fallen behind the US in recent times, and that price gap is widening each year.

Click on image for a larger view

India and Brazil global exports versus Australian exports

Both India and Brazil sit well behind Australia and the US in terms of global average prices. Not surprisingly, given product quality, India’s price is now less than half that of Australia’s, while Brazil’s prices are 43pc less than Australia’s. This is 10pc less than the levels of four years ago.

Why have both Indian and Brazil become cheaper in the last four years compared to Australia?

Key points to note:

- Australia’s premium over India is 103pc (or double). This I believe is related to the crackdown of the grey trade into China.

- China (via Vietnam) at one stage took more than 57pc of India’s buffalo exports but in the last six months (Sept-Feb) a dramatic decline has occurred with only 30pc of Indian buffalo exports going to China (via Vietnam).

- Indian buffalo has been displaced into other secondary markets like Egypt which has seen Indian imports jump 130pc, but as a consequence lowered prices in global secondary markets which in turn has pushed Brazil prices even lower.

- It is not all gloom and doom for Brazil however, as it has increased exports to China directly in 2018 by 52pc compared to the previous year, and explains why the fall in India’s prices has been much greater than Brazil’s, due to the increased direct shipments that Brazil has into China that India unfortunately does not have.

Report card score: 9/10. Australia’s position globally has improved compared to India and Brazil in terms of price.

US exports versus Australian exports into Japan and Korea

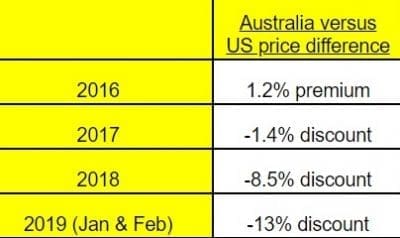

When assessing Australia and the US average global export price it iss clear that Australia has been losing market price ground over the last three years. In 2016 Australia traded at a 1.2pc premium to the US, in 2017 this fell to a 1.7pc discount and then fell further in 2018 to an 8.5pc discount. For January and February of 2019, it is now at a 13pc discount.

So why is Australia’s export beef value falling in relative terms, when only three years ago we were at a premium to US supplies?

When speaking with Australian beef exporters they offered a multitude of different reasons given, including differing exchange rates, freight rates, over supply, restricted access for some Australian exporters to China, differing tariffs in various countries and the impact of drought in Australia that has led to discounting compared to the US.

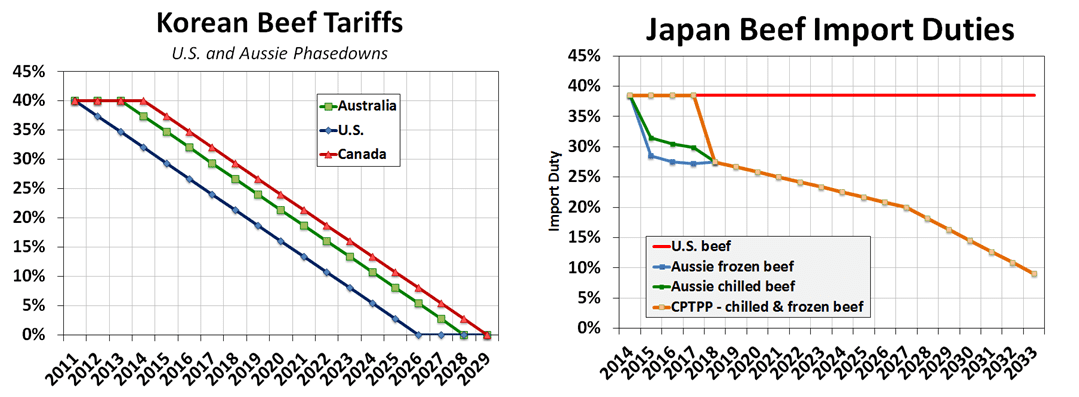

The main reason I believe for Australia’s growing discount to the US has been a change in consumer preference for US beef over Australian beef in both Japan and Korea, and to a lesser extent the duty advantage the US has over Australia in the Korea market. This currently sits at 5pc and Australia’s disadvantage in duties remains in place until 2028, when it phases out to 0pc. The US duty finishes two years prior in 2026.

In contrast Australia has a dramatic tariff advantage in Japan which in 2019 sits at 13.5pc differential and will continue to grow until 2033. So one would think the advantages in Japan for Australia beef exports would outweigh the disadvantages in Korea? On paper I would say yes, but in reality it is a different story and I believe we are losing market share in Japan even with a trade advantage.

Japans US tariff is being passed forward to consumers

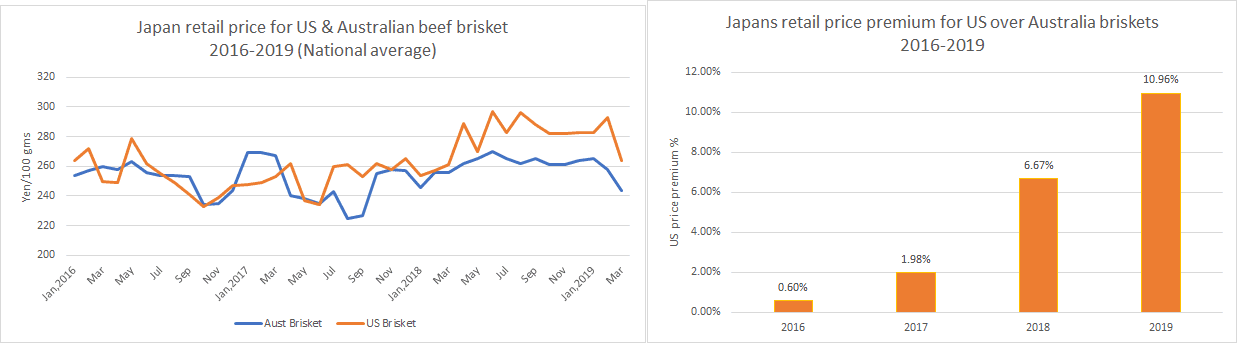

Japan has been selling US beef at a significant premium to Australian beef, at both the wholesale and retail levels. This premium has increased by almost 5pc per year over the last three years. A good example is grainfed US beef chilled Chuck rolls in February which sold in Japan at 1296 yen/kg in contrast with grainfed Australian chuck rolls sold at a 16pc discount at 1087 yen/kg.

Other examples include US briskets whose retail price premium has been increasing over Australian briskets since 2016. In January and February US brisket prices this year are retailing 11pc higher than Australia’s brisket levels.

Click on image for a larger view

So even with the 13.5pc Australian duty advantage, the Japan importer has passed forward the greater US duty cost to the consumer. The net effect to me is that US exporters into Japan receive prices equal to or potentially greater than Australian prices at the time of shipment.

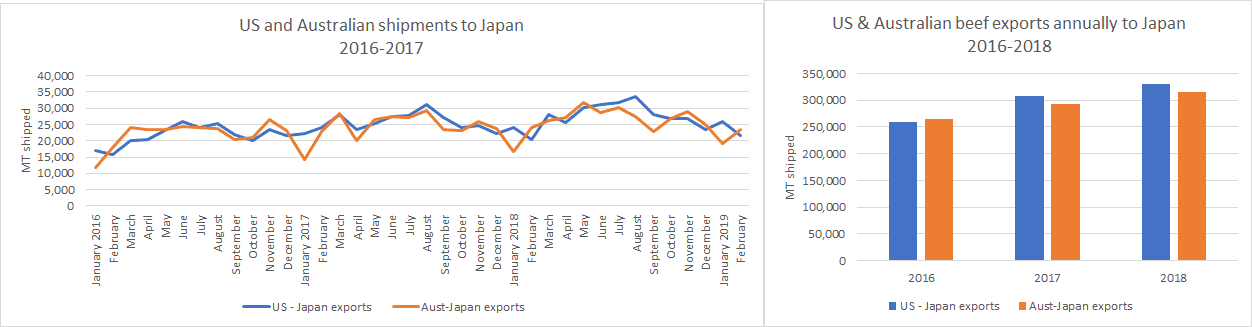

What is troubling for Australia’s market share is that Japan consumers are willing to pay this US premium – such is the high demand for US beef which has seen US export volumes increase in both 2016 and 2017. In both years US beef exports exceeded Australia’s beef export volume even with the headwind of higher tariffs, and the higher price having to be paid by consumers.

Click on image for a larger view

Korea’s tariff is being passed back to Australian exporters

In Korea the US has a 5pc tariff advantage over Australia which gives US exporters a distinct advantage. At the same time there is also a larger volume of US beef being sold into Korea which to me is displacing Australian beef in terms of pricing.

The cost of the increased tariff is part of the problem, but a bigger concern for Australian exporters is the preference by Korean consumers for US beef. This has seen the majority of these costs being passed back to the Australian exporter which is in complete contrast to Japan’s costs being passed forward to the consumer.

Click on image for a larger view

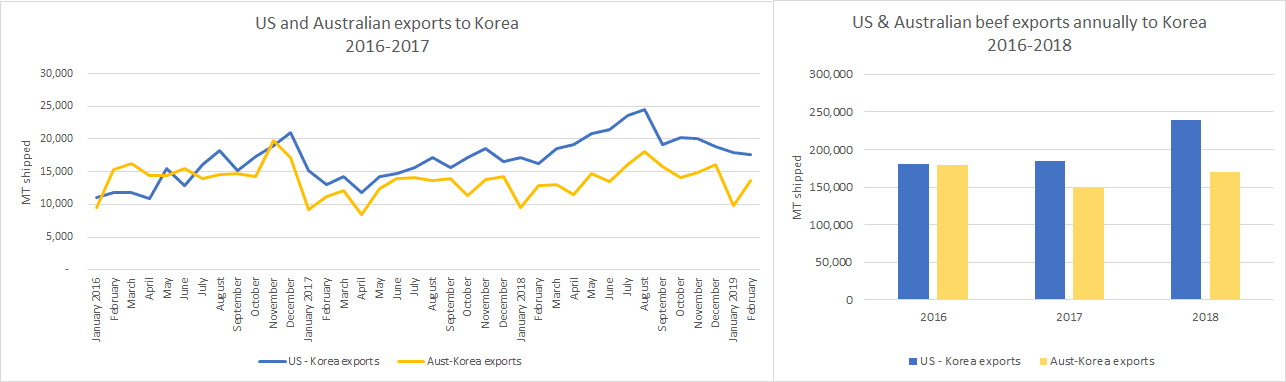

In recent times this price difference has ballooned out to 25pc, with March US average export prices at $3.32 US$/lb compared to Australia’s $2.61 US$/lb. The 5pc additional duty cost is only part of the 25pc price difference, but the displacement of Australian beef both in terms of volume and price by US beef has been the bigger reason for the growing price spread.

US shipments are up 32pc in volume since 2016 and Australian exports are down 5pc. In short, just like Japan, we find that Korea’s consumers have a preference for US beef and once again are willing to pay a premium for US beef over Australian beef.

The key difference to me between Japan and Korea is that the majority of the US/Australian price difference has been borne by discounting the Australian exporter more so than passing it forward to the consumer.

Click on image for a larger view

Isn’t US grainfed beef different product to Australian grainfed beef?

This is the common catch cry from market participants who are trying to justify the price differential, and I agree to a certain extent. US beef exporters typically produce a 140-day grainfed product compared to the 100-day grainfed in Australia, but the current US product and Australian product is no different to what each country produced four years ago, when Australia’s meat traded at either parity or at a slight premium to US beef.

So that argument does not quite work, as it does not explain why US beef is now commanding a huge premium over Australian beef and yet four years ago Australia’s beef traded at a premium into the same market.

I think the answer lies in the dramatic change in Asian consumer needs and taste in the last four years, and the dramatic growth in the spending power of the Asian middle class in that short time period. This is occurring in Korea, Japan and China.

US beef ‘fits the bill’ in terms of the middle class wanting a higher marbled meat and the ability of US processors to produce ‘peas in a pod’ in terms of product consistency and full container loads of single items that Asian importers want as opposed to mixed loads from Australia.

In short, the product produced by Australia and the US has not changed much in four years – it’s the consumer that’s changed.

It should be noted that when BSE occurred in the US in December 2003, we saw Australia’s beef move to a dramatic premium over US beef as bans were put in place and strict cattle age requirements were enforced by the Japan Government. The impact of BSE lasted until about 2008, after which the strict requirements on age were relaxed in part-enabling more US cattle to be eligible for this market. I see the premium paid today for US beef in Japan and Korea to be driven by consumer sentiment, more so than any market impediment that historically impacted market prices like BSE.

I think that Australian processors are recognising this increased demand for higher marbled meat throughout Asia, and the increased demand for middle and longfed beef with also the continued growth in Wagyu being a good example of strong demand for quality.

The growing tariff differential between Australia and Japan will eventually give Australia a strategic advantage, but to date at 13.5pc, it has yet to occur.

One of the other challenges for Australian processors and lotfeeders has been the drought and the high cost of grain in Australia. When discussing with processors the advantages of producing a 140 day grainfed animal versus a 100 day grainfed animal, the common answer is that it has been ‘the law of diminishing returns’ – when it comes to the added cost to get to 140 days, there has not been the equivalent premium in sale price.

In short, with high input feed costs the numbers don’t work for processors to keep animals on feed longer and try to compete with 140-day US product.

Japan report card score: 6/10. Australia’s position into Japan has deteriorated both in terms of price and volume even though there is a 13.5pc duty advantage over US beef. US beef now commands better retail and wholesale prices by an estimated 11-16pc premium, Japanese consumers are happy to not only pay this premium but have increased the volume they consume – Japanese consumers have a genuine preference for US beef.

Korea report card score: 4/10. Australia’s position into Korea has deteriorated even more so than Japan in terms of price and volume. US beef has up to a 25pc premium to Australian beef and has clearly displaced Australian beef from the market, resulting in lower prices and less volume being exported to Korea. Like Japan, Korean consumers have a genuine preference for US beef.

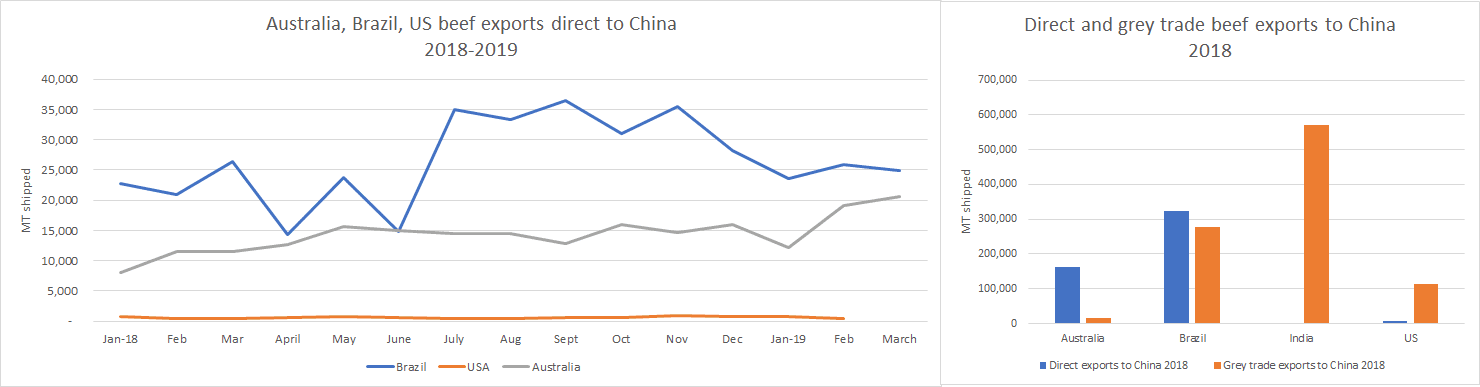

US, Brazil, India & Australian exports to China

The performance of Australia and Brazil direct shipments into China has been far better than US shipments. This in part can be explained by the 37pc China duty that exists on US meat imports (12pc regular duty and 25pc retaliatory duty) due to the US/China trade war, but the real reason is the Chinese ban on HGP beef and the lack of traceability since birth on US cattle.

In reality, it is estimated that within the US only 170,000 head of cattle out of a herd of 85 million head meet the China import protocol requirements.

Click on image for a larger view

Australia’s and Brazil’s performance on beef exports into China has been good – the concern for Australia will be the ability to maintain this momentum in the future given the political issues that exist between China and Australia.

This is best shown by the 16 plants in Australia that are still waiting for China approval and have been for two years. The makeup is 11 meat works and five cold stores.

Last December, Brazil had been given approval for an additional 78 new meat establishments into China which included 26 pork plants, 22 beef plants and 30 poultry plants. So far these have not appeared on the official approval list from within China and Brazil, so I can only assume they must still be pending for approval.

The US usage estimates for ractopamine and/or HGP is more than 97pc of all cattle, and China has a zero tolerance for HGPs. It is estimated that should the US forego HGP usage, the cost is around US$180/head (or A$255/head). If this policy should remain in place by China, it is difficult to see the US ever being a serious competitor in this market.

China report card score: 8/10. Australia’s position into China has improved during the last 12 months, but as African Swine Fever impacts pork, chicken and beef demand, the ability to respond to the expected further demand increase will be crucial. At the moment other countries are expanding their ability to supply China, but Australia’s capacity remains stagnant. Next year’s report card may not look so healthy for Australia.

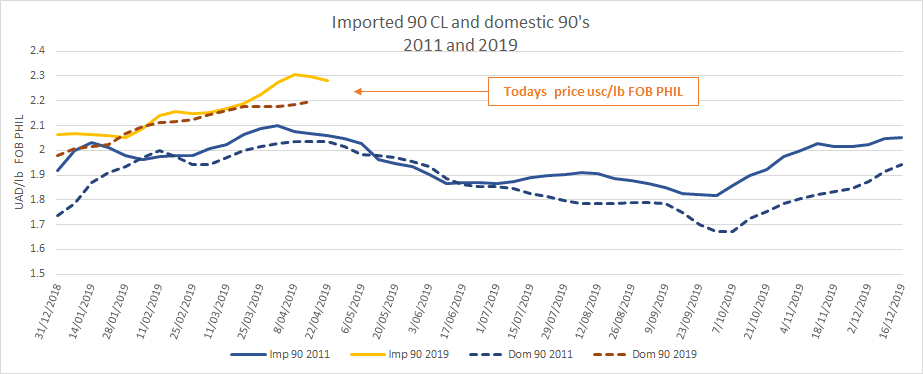

Australia’s export to the US domestic market

Australia performance on the US domestic market in recent months has been outstanding, with imported prices trading at a premium to domestic prices. This is most evident in 90CL (chemical lean) grinding meat values. This, I believe, is because of the reduced shipments of lean beef from New Zealand in the last six months that has created a market shortage.

Both Australia and NZ imported 90CL meat is currently trading at a 6.5 USc/lb premium to domestic 90’s and in the last two weeks has ballooned out to 12.5 USc/lb. This is highly unusual, but it has occurred before. In 16 years, it has occurred five times to be exact, but only once in 2010 to this level of premium. I am expecting Australian and NZ lean meat to remain at a premium for most of 2019. (I will be discussing this in more detail in a separate report next week).

US report card score: 8/10. Australia’s position into the US is strong thanks to the lack of lean meat exported from New Zealand – this premium for imported 90 CL over US domestic meat is likely to remain in place for the balance of the year and could become the new norm if New Zealand and Australian shipments fall further in future years.

Conclusion

Strategically, how does Australia go forward from here in terms of trying to maintain our market presence, but spend our marketing dollar wisely?

When the Australian drought breaks cattle and sheep supply will tighten dramatically and the available marketing funds will also tighten dramatically. I have estimated in previous Beef Central reports that the fall in beef slaughterings could be as much as 16pc, which would mean a significant fall in transaction levies, and would see a significant fall in MLA’s revenue collection and therefore reduced funding of marketing.

Other points to note:

- A sharp rise in cattle prices is expected when the drought breaks and processor margins will suffer. This in turn will lead to smaller marketing budgets by individual companies.

- These two factors combined means a smaller overall marketing pool bucket and therefore points to spending our marketing funds wisely. To me, the situation in Japan and Korea will not change overnight given that US production forecasts for next year are expected to be 2pc higher (USDA) and this trend is likely to continue over the next ten years.

- Regaining a foot-hold in these two markets might be difficult. To me, minimising marketing and promotion costs in these markets and putting these funds elsewhere might be more fruitful.

- I think the trend of Asian consumers seeking high quality fed beef is unlikely to change and Australia’s increased efforts should lie in assisting the Australian lotfeeding sector to expand.

- The growth in the niche markets of ‘healthy grassfed’ programs is also critical, and the success of programs like ‘Never Ever’ programs is good evidence of this. I am seeing this in selected cuts every day in the market, whereby grassfed certificates and certain ‘clean’ programs are being asked for. This trend is also unlikely to change.

- There is a need for simplifying accreditation schemes that are often key to niche marketing for both farmers and processors in terms of specific customer and country requirements and thereby reducing the on-going burdensome costs that audits place on farmers and processors.

- China is a key market that Australia has a strategic advantage in, given the number of eligible cattle we have for this market compared to the US. There is still an underlying concern among some Australian exporters about the political uncertainty that surrounds the government-to-government relationship, so any beef promotions needs to be cognisant of China’s political concerns. Spending marketing dollars in China makes good sense.

- The spread of African Swine Fever through China and the rest of Asia (see Simon Quility’s most recent ASF report here) will create opportunities in beef, mutton and lamb as consumers move away from pork, due potential critical shortages of pork supply and/or a change in consumer preference for other proteins.

The disease is now present in China, Vietnam, Mongolia, Tibet, Cambodia and North Korea. As it spreads it creates opportunities for other proteins to fill the protein supply void. These are where promotional efforts should also potentially go.

The challenges that lie ahead for Australia in beef and sheepmeat exports will be enormous, as supply becomes extremely tight and our market share is likely to diminish no matter what. I think it’s important not to be caught up in the ‘noise’ that often surrounds loss of market share, but to focus our energy (and marketing funds) on where our strengths lie.