Simon Quilty

Independent analyst Simon Quilty, just back from a series of speaking engagements in the US covering the impact of China’s African Swine Fever outbreak on the global meat trade, sees evidence the Chinese Government has commenced a major imported pork buy program that will see large quantities of US pork exported to China. “All of this has significant global ramifications for beef, poultry and sheepmeat demand,” he writes.

EIGHT months ago in August after the announcement of China’s second outbreak of African Swine Fever in Henan province, I wrote that I was amazed how quickly changes in global meat markets can occur – and the outbreak of ASF in China is one of those moments that can take your breath away.

It is unfortunately often at the expense of one market that opportunity in other markets is created.

My thoughts have not changed since then, and in the wake of pig herd liquidation in China, the China Government buy program that is now unfolding is likely to be the largest protein buy program in the history of US pork exports. It will far surpass the last such event in following China’s outbreak of Blue-ear disease in pigs in 2007-08.

All of this has significant global ramifications for beef, poultry and sheepmeat demand.

Here are some key indications that China’s pork buy program is already underway:

Last week US pork export bookings to China surged by 73,779t, up from just 22,674t the previous week. This is the highest weekly pork export volume to China in six years.

China hog prices have jumped 25pc in recent weeks and China’s inflation is on the increase. China’s central government this week has insisted that all domestic frozen pork stocks in meatworks and cold stores throughout China be ASF-tested, ensuring that this product is sold by July 1 – clearing the way for more cold storage space for imported pork.

The rapid depletion of China’s sow herd due to ASF is pointing to an evolving large protein supply gap that is estimated to be close to 8.2 million tonnes needed in 2019, with estimates on China pork imports at 4.5 million tonnes – up 60pc on last year’s imports. US pork exports are expected to be close to 1 million tonnes into China and Hong Kong in 2019, and with rising hog prices, this supply gap is growing quickly.

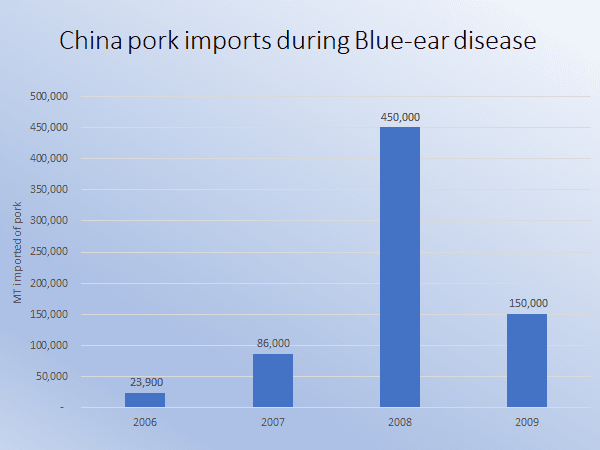

Blue-Ear disease in 2006

The last major China buy program was back in 2006-08 when Blue-ear disease impacted the nation’s pork population. I believe the lessons learnt back then will give us a good guide today on how this new Government buy program will work. As stated by the Chinese government in a 2008 report, “’The purpose of the import program is to stabilise domestic pork prices and ensure market supply.” Under the Blue-ear disease outbreak, this was achieved in late 2008. But the time-line to achieve the same result in 2019-20 with ASF is likely to take years, not months.

How would a new China Government pork buy program look?

The following are my thoughts on how a China buy program might look:

- Key alliances will be formed between countries and individual companies to ensure that a commitment on volume (not necessarily price) will occur over the next several years. The most obvious pork supply countries being the US, EU, Canada and Brazil, which make up 90pc of global pork exports.

- Product exported is more likely to be as carcases than as individual whole muscle cuts, as the cost of de-boning these carcases in China would be considerably less than in the US and/or Europe. A three way cut carcase is most likely for ease of preparation and packing.

- The other advantage of exporting carcases is that under USDA reporting requirements, carcases are exempt – so that any export sales would remain unknown for at least two months until the regular monthly US export data becomes available. This will provide a certain amount of ‘anonymity’ to dedicated US suppliers in a China buy program.

- Ractopamine-free dedicated export kill facilities are likely, whose sole purpose will be to supply the China pork buy program.

- Duties will be non-existent under a China Government buy program. The 62pc duty will no longer apply – the reason is simply why would the Chinese Government apply duties on themselves at time of crisis? In short, government imports are exempt from tariffs.

- Depending on the import volume, which I imagine will be large, then a China buy program will require significant cold storage space within the US and China. This might well see shortages of space for other products and other market participants (i.e. beef from Australia) as China destined frozen pork takes priority over local US production.

- In addition, a China buy program will see the need for large quantities of refrigerated containers, shipping vessel space and trucks to distribute throughout China – thereby ensuring an effective cold chain storage supply system. In some instances any additional cold storage capacity required may still need to be built in coming months.

The role of imported pork to control pricing in China

Back in 2008 under the Government buy program, 450,000t of pork was imported as a means of controlling China’s domestic pork pricing. In a China Government report at the time, it was stated that “In order to stabilise domestic pork prices and ensure market supply, China Governments import arm imported pork from the US and other countries three times that year. By August 2008 the import plan had been completed.” The report went onto say that “Due to the recent sharp drop in domestic pork prices, the rebound in supply has led to a significant decline in China pork imports.”

In other words, the import plan had been highly successful, but what was not evident was that a massive vaccination program occurred in China at the same time, with 300 million pigs being vaccinated over six months, with four vaccinations per pig (1.2 billion vaccinations in total).

In anyone’s language, it was an enormous effort and shows what China is capable of doing when given a solution to a problem of this magnitude.

How long is this buy program likely to last and how high can China pork prices go?

Unfortunately there is no vaccine or cure for African Swine Fever. Given the rate of liquidation due to unusually high domestic slaughterings, disease losses and culling, there is no clearly defined end point to the current buy program.

Equally, it is difficult to know how high prices could go, given the liquidation process is far from over.

As a guide, I have looked at the last three previous pork price cycles in China.

In the 2006-08 Blue-ear disease episode, pork prices rose by 198pc, and the cycle lasted 23 months.

In 2010-11 due to PEDV, the cycle lasted 17 months and prices rose 103pc, and in the most recent disease cycle in 2015-16, the cycle lasted 15 months and increased 99pc.

I can only assume that given the severity of ASF that we can expect a cycle to last at least 3-5 years (or longer) and for prices to more than double (some analysts have talked of a 300pc rise in pork prices in China).

Ractopamine in US pigs – will this hold back trade?

The presence of the feed additive ractopamine in US pork production, a growth promotant which is banned in China, raises the question of what percentage of US pork production could be prevented from export.

The latest estimate is close to 50pc of production with the belief that this restriction will not hinder a China buy program. It should be noted that Japan, South Korea and the US markets all deem meat from livestock fed ractopamine safe for human consumption – hence the estimated 50pc of ractopamine-free US production available for China seems to be more than enough suitable livestock at this stage to meet the needs of the China buy program.

China pork production estimate falls 30pc – Will history repeat itself?

In the last week a MARA official (China Department of Agriculture) said that in late February ‘irrational’ culling of sows on breeding farms was reducing core production capacity across seven Chinese provinces. In this report they cited a 26pc year-on-year fall in sows inventory in Henan – the largest pork producing province in China.

If this figure was applied nationally, it would equate to a 186 million less pigs produced, or 43pc of the national 2017 inventory figure of 430 million head. Comments made by the Agricultural Ministry’s husbandry bureau expressed concerns saying that large cutbacks had occurred by backyard farmers, big commercial companies and key provincial nucleus breeding herds.

Social unrest in China was a real concern in 2007 due to high food costs, and in particular high pork prices, with Premier Wen at the time speaking publicly about the need for a market ‘adjustment’.

Various initiatives were taken by local governments and Beijing – ranging from monthly payments of 20 yuan to low income families to providing subsidies for pig producers to encourage rebuilding of the herd.

The estimates recently published by Globalagri Trends of a 30pc decline in production, later repeated by Rabobank, points to pork imports in China for 2019 having to be close to 4.1 million tonnes. It is estimated that the US will contribute close to 1 million tonnes of that total.

In 2008 with Blue-ear disease, the China government undertook policies to encourage rebuilding of the swine herd, such as financial subsidies, rectification of circulation channels, restriction on exports to ensure domestic pork supply. As a result, China’s domestic pig prices fell slowly during 2008 and by year’s end had fallen 15pc. The government reported that rebuilding started to commence again.

Unfortunately, in 2019, this is unlikely to occur given that no cure exists for ASF and that there is little confidence in the breeding sector. For many farmers the collateral they have is the livestock they own (land is state owned) and the uncertainty over whether the animals a farmer owns will be alive tomorrow (should they contract ASF), then few banks will be willing to take on such risk and lend to breeding operations.

In recent weeks we have seen hog prices in China rally 25pc and more importantly due to the lack of sows (and therefore piglets) piglet prices have rallied 81pc during the same period. In other words ‘the well is running dry’ in producing piglets due to sows being liquidated and are not been replaced.

ASF is now impacting greater Asia as the disease spreads over China’s borders

ASF has spread in recent weeks to Cambodia, Mongolia, Tibet and Vietnam and it seems inevitable that all countries surrounding China are likely to be infected within the next 3-6 months, including both North and South Korea.

I have referred to these countries as Stage One, with Japan, Taiwan and the Philippines as Stage Two. On the same basis of a 30pc fall in production in all these countries during the first 12 months, I have estimated a protein deficit of 1.3 million tonnes and 1.6 million tonnes respectively, is likely to occur.

When added to the estimated 8.2 million tonne deficit in China, the need for more animal protein in Greater Asia becomes almost overwhelming.

Current frozen pork stocks in China are either being locked up or having a fire sale

Anecdotally, there have been reports of large quantities of frozen pork in cold stores throughout China, which were produced when China’s pork production jumped in Q4 2018 and Q1 2019. China Department of Agriculture reported that slaughterings in the last quarter of 2018 saw kills up 47pc in Q4 of 2018, as farmers panicked to sell there pigs, which saw liquidation of both sows and hogs in almost unprecedented numbers as farmers looked to either exit the industry or reduce their exposure.

In recent days the Henan government has declared that no current frozen pork inventory in cold stores that was produced between January 2018 and March 2019 (last 15 months) can be released. In other words this pork is deemed to be ASF-contaminated, and I assume will be destroyed. The quantity involved is unclear, but given Henan province is China’s largest pork producing region, it can only be assumed that the amounts involved are sizeable.

In complete contrast, the Chinese central government has insisted that all frozen pork stocks must be tested for ASF by July 1, by both meatworks and cold stores, thereby ensuring that domestic frozen pork inventory will be removed from cold stores by July 1. Question marks remain over the accuracy of testing, but none the less this could be bearish in the short-term as frozen product is released onto the market over the coming weeks as owners of this meat look to offload in preference to having it found with ASF.

Once again quantities are unknown, so it is difficult to assess the degree of downside in market prices, but I think it is fair to say it will be short lived.

What is clear to me is that the government is creating freezer space in China to handle the large volumes of imported pork expected in coming months, and to me provides further evidence that the China buy program is imminent, or has already started. The downside to this is that all frozen domestic pork in China is potentially contaminated with ASF, and that re-infection is likely as this domestic frozen pork gets consumed and the scraps and swill created will re-infect the current pig population, leading potentially to a second wave of outbreaks, deaths etc, and the cycle continues.

Regionalisation and compartmentalisation – will this work?

The discussions between governments across the world on regionalisation and compartmentalisation is aimed at isolating ASF infected facilities and ensuring surrounding regions can continue to trade and export thereby minimising the disruption to markets.

Regionalisation might involve an entire state and compartmentalisation involves individual facilities or clusters that might be fenced-off should an ASF outbreak occur. As far as I am aware these discussions are still in there early days, and require acceptance of this status by key import countries, namely China, Japan and Korea. To date I do not believe any acceptance has been given.

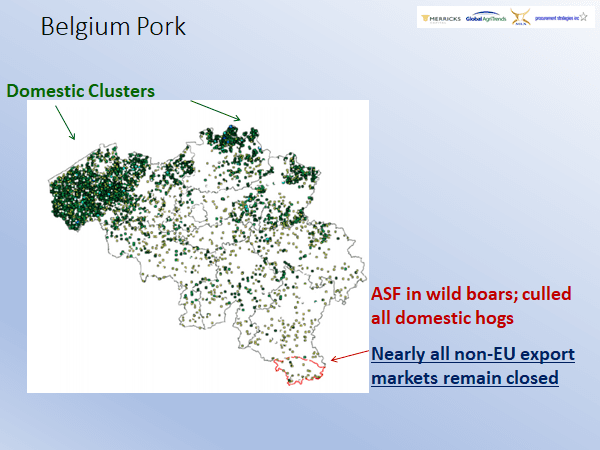

As a sobering reminder of the difficulties with regionalisation is Belgium, which has had 723 cases of wild boars contracting ASF, which have been isolated in the southern part of Belgium – all domestic hog production occurs in the northern part of Belgium. There seems to be little or no chance of contamination to Belgium’s commercial pork sector yet nearly all non-EU export markets remain closed to Belgian pork. So it is clear that regionalisation has not been accepted by many of Belgium’s former export markets.

The fear for North America should it contract ASF is a similar outcome to Belgium, whereby export markets would be cut off from US processors. US pork exports account for 23pc of total US pork production, so the importance of export markets remaining open to US hog producers and pork processors cannot be overstated.

Regionalisation may prove to be more beneficial for US imports than exports

The irony is that regionalisation in the US may see more benefits for imported pork than for US exports. Assuming regionalisation is accepted by many countries and should large volumes of US pork going into China’s buy program lift US domestic pork prices significantly, it is likely US pork manufacturers and distributors will seek alternative sources of supply. This could see an increase in US pork imports from countries that have a mutual recognition of regionalisation but struggle to sell pork globally (such as Belgium) thereby providing a cheap source of imported pork products for US importers.

This is based on the premise that the US remains free of ASF and as a result could see unusual global pork trade flows for both export and import pork items over the next five years, with varying country policies globally either accepting or not accepting regionalisation as stated, creating trade flows that once never existed and may now potentially occur due to quickly changing global market nuances.

Does the USDA want to play the role as global ASF policeman?

One of the challenges I see with regionalisation is ensuring the integrity of the watch dog who will oversee the protocols required for regionalisation (and compartmentalisation) to work. Should a country request regionalisation, it will I believe, require a detailed assessment of bio-security systems within the country, assessing the severity of the disease within the infected region (or compartment) as well as adjoining regions and ensuring that necessary bio-security changes are made and maintained.

To me, the only truly trusted global organisation to carry out this assessment is the USDA – no different to the role it has played over many years with global foot and mouth disease.

As a meat trader I have observed with respect the USDA setting global standards and maintaining them. In the past, should the USDA give approval to a former FMD supply country, then the rest of the world has been happy to follow suit. ASF to me will be no different.

My point is that given the enormity of ASF, does the USDA have the resources to provide this role and do they want to be the global ASF policemen? Without USDA performing this role, I struggle to see regionalisation (let alone compartmentalisation) working with any degree of success.

‘A rising tide lifts all boats’ – poultry, beef and sheepmeat

There is no doubt to me that once the China pork buy program gets into full swing, it will see global prices of pork rise and should Blue-ear be a guide, it is likely to see prices increase greater than 198pc. But as pointed out at the beginning of this report, even with a record volume of imports this year into China, it still creates close to an 8.2 million tonne deficit in animal protein.

Poultry is the obvious go-to in terms of the ability to ramp up production and respond quickly to changing market conditions and meet this protein deficit. Growth in the poultry sector is likely to occur quickly both within China as well as externally. There are signs within China that poultry is already expanding quickly, with poultry feed sales expanding, but these are constrained by the lack of breeding stock and environmental restrictions.

Poultry imports may well be the next step in the China buy program, and the recent decision by China to lift a four-year ban on French poultry imports is one of many potential means of meeting the expected large protein deficiency.

Poultry prices in China are close to record levels and the USDA recently forecast a rise in demand of close to 9pc in 2019. This looks to me like an understated forecast that could be easily doubled or tripled in 2019-20 to give a truer estimate.

The impact on US beef prices is a little more difficult to quantify from a US point of view, as beef from only 170,000 head of cattle is eligible for China (out of a 95 million head herd). So much of the improvement in the US beef market will rely on global displacement, whereby greater beef exports from Australia, New Zealand and Brazil will go into China during 2019-20, and US beef will be the back-fill in Japan, Korea and other key beef markets that compete directly with China

This, I believe, is likely to take another six months or more before the full effects are seen on the US domestic beef market.

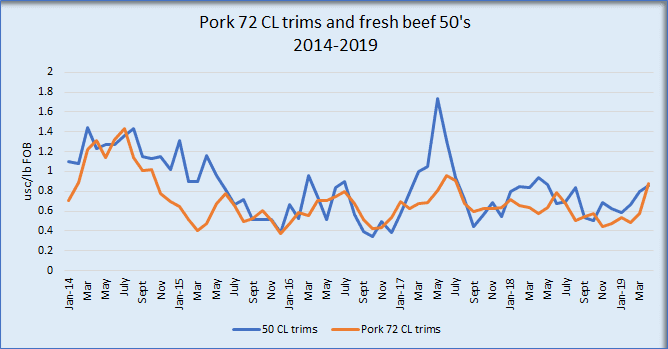

One exception to this might be the US grinding meat complex, which could see upward price pressure sooner than later, whereby 50 CL trims which have a strong price relationship to pork 72pc and 42pc trims could potentially rise in tandem with pork trims, should pork availability tighten dramatically under the China buy program.

When the tight availability of imported lean meat due to Australia and New Zealand selling large quantities directly to China away from the US market are added, this combined impact could see a strong US grinding meat complex throughout 2019 that in turn will force all other domestic trim prices higher.

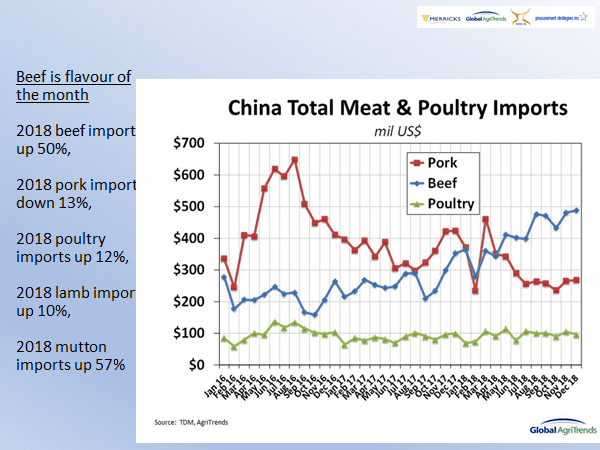

When assessing the import figures into China for 2018, many of the trends of increased demand were in play before ASF occurred, but there is no doubt the disease saw an added surge in imports and will continue to do so in coming years to fill the protein void.

Sheepmeat, both as mutton and lamb imports, were up 57pc and 10pc respectively in 2018 and there is no reason why this trend won’t continue.

Other lessons learnt from the last major China buy program – Blue-ear disease 2006-08

The following were lessons learnt from the past Blue-ear disease episode 2006-08:

- In 2007 Premier Wren called for strategic pork and live pig reserves that could be used in the event of severe food shortages. Today these pork and live pig reserves are problematic because frozen and fresh pork carries the AFS pathogen for up to 1000 days, so domestic pork reserves are potentially a liability. Imported pork is to me the only true solution to guarantee clean pork.

- In 2007, virulent strains of Blue-ear disease (PRRSV) emerged also in Vietnam and the Philippines. The spread pattern in Vietnam (2007-10) suggested the occurrence of new strains in the northern part of the country earlier in 2007. This coincided with the Tet-Holiday, one of the major ‘harvest times’ in pig production in Vietnam and increased people and product movement in the country. Once again in 2019-20 holiday periods will be the most likely periods of high risk for disease spreading, whereby people traffic will increase dramatically as family’s cross borders, regions and countries to visit relatives.

- In 2008 under the China buy program, private enterprise accounted for 40pc of the import program and government owned enterprises accounted for 60pc of pork imports. I see this next China buy program to be no different, as the initial imported volumes may occur under the higher tariff situation and by the Chinese government importing direct avoids the 62pc duties. Private enterprise is likely to play its role later, once the US-China trade war is resolved and tariffs have been removed.

Anecdotal evidence keeps growing

The Jilin province has estimated hog inventories down by 50pc – local pig brokers are talking that trading numbers are now 25pc of what they were before ASF (down 75pc). Today there are empty barns where farmers have cleared out all breeding pigs, because they are afraid of the disease. China’s Department of Agriculture recently estimated Jilin province hog numbers down 28pc.

Tight cash continues to be a problem with farmers saying they are unable to feed there pigs, or are only feeding them every few days. In one province an estimated 338,000 pigs starved to death in January.

Conclusion

I believe the pace of change in the global protein markets over the next 3-6 months will be dramatic as US pork prices are likely to go significantly higher and force change in other proteins – this in turn will see the growth in China of other protein supplies such as poultry (including ducks) and aquaculture. Recent data shows that feed supply is up in those regions that specialise in this type of production as the market looks to expand into other protein sources.

The answer to China’s 8.2 million tonne protein deficit lies I believe in many alternate protein sources with poultry being the largest beneficiary, but aquaculture, beef, sheepmeat, increased pork imports and eggs all in the mix. Eggs are a well-recognised but understated protein source in China that is very much part of the Chinese everyday diet, and may expectantly play a crucial role in filling the looming protein gap.

Either way I look at the medium to long-term outcome, it is all bullish protein prices for many years to come with some potential short-term downside in the next few months as China’s domestic frozen stocks come to market. After July 1, it looks like blue skies for global pork prices after what can only be described as a stormy last 8 months.