AS the United States beef industry descends deeper into its drought liquidation-driven cattle shortage, US feeder cattle prices have risen dramatically in relative terms against Australian equivalent feeders.

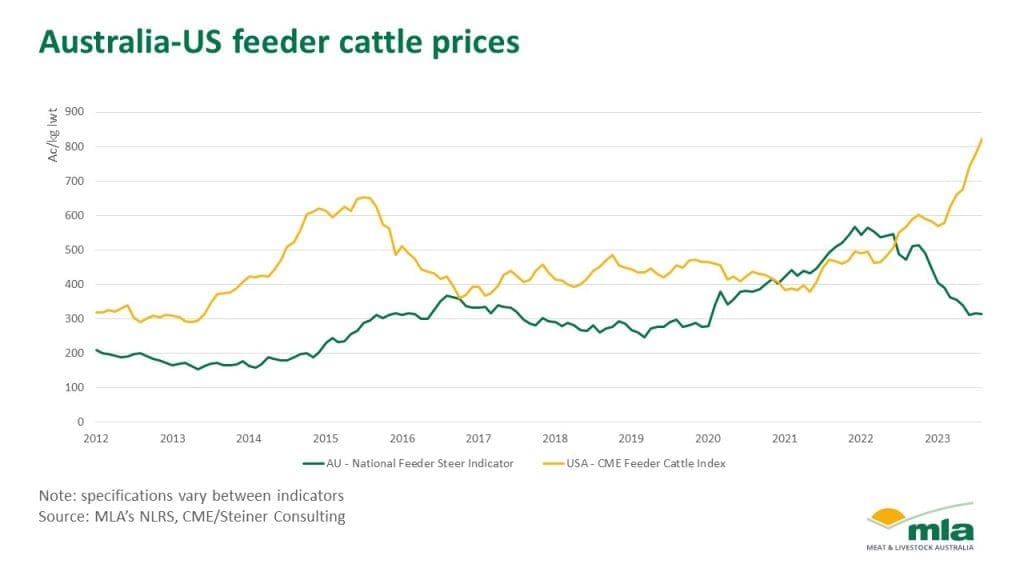

As the graph above shows, US feeders are now at all-time record highs, worth two and a half times what they are in Australia, when measured in Australian currency.

Australian feeder cattle prices have deteriorated sharply during 2023, with the NLRS feeder steer indicator (saleyards-based) sitting on Friday at 303c/kg liveweight – its lowest point since 2020. The indicator is down another 15.4c/kg over the past month, and back 190c/kg on this time last year.

In contrast, US equivalent feeders last week (as measured from the CME feeder cattle index) were worth around A825c/kg liveweight, when converted to A$ equivalent. That’s risen from around 560c/kg only six or eight months ago.

Right now, the difference in price on a feeder steer on either side of the Pacific is around 500c/kg, worth around $2250 on a 450kg feeder.

Click on image for a larger view

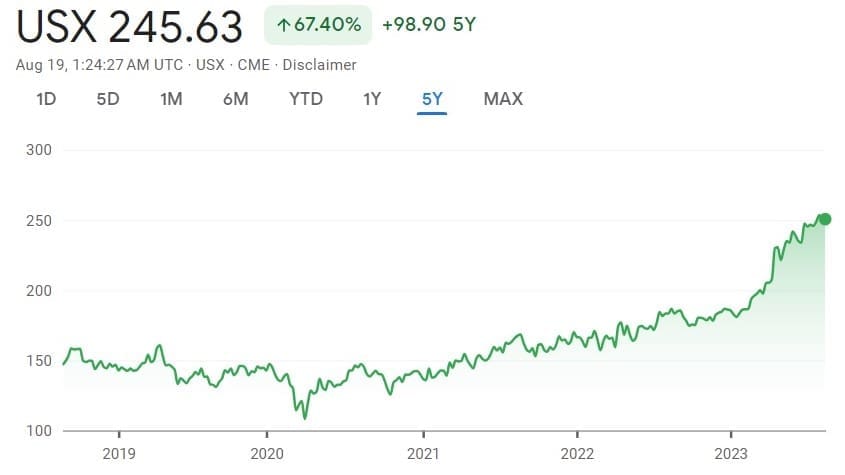

The second graph published here plots the CME US feeder cattle contract in US$, over the past five years. It currently sits at US245.6c/lb. The graph shows the extreme rise seen since April, now well into record territory as the US herd decline impact is seen, and up 37pc on this time last year.

Earlier this month we saw email threads where 350kg feeder steers in the northern US state of Wisconsin were selling for the equivalent of A$7.50/kg liveweight – all time record highs.

Previous cycles

While there have been other periods in the past ten years where US and Australian feeders have diverged widely (see period around 2015 on the first graph, also driven by response to drought), none have happened as deeply, or as sharply as they have this year.

The graph also shows that during 2021-22, there was a period when shortage of feeders in Australia caused by our own drought in 2019-20 saw Australian feeder prices at a premium to those in the US, for about 15 months.

Sharp rise in feeder numbers

In contrast, there’s been there’s plenty of evidence of a sharp rise in feeder cattle coming to market in Australia over the past month, driven largely by the dry conditions.

Feeder cattle numbers offered at NLRS-reported sales almost doubled last week, compared with a month earlier (8200 head versus 4300 head).

Listings of feeder steers on AuctionsPlus jumped 135pc last week, where 811 steers heavier than 400kg were offered. Last week’s offering was more than double the typical 200-400 head range catalogue seen since May.

US feeder price movements

MLA analyst Tim Jackson said while Australian feeder prices had deteriorated considerably this year, it has been the acceleration in US feeder prices in recent months (yellow line) which had been the biggest impact on the trend.

“It’s put a rocket under the feeder price spread,” Mr Jackson said.

“It’s put a rocket under the feeder price spread,” Mr Jackson said.

Since this time last year, about 60 percent of the divergence in price between the two countries was due to the lift in feeder prices in the US, with the remaining 40pc due to Australian price performance.

“Mixed in with that is a little strengthening in the US$ (the graph here is presented in A$ terms), but the same trend is evident, regardless of which currency is applied,” he said.

This time last year, the A$ was worth about US68c, around 3.5c higher than today.

Mr Jackson said in outright terms, today’s feeder price spread was wider than it has ever been. However when measured in percentage terms, periods in 2014 and 2015 were still slightly wider, because the numbers were coming off a lower base. At its extreme in late 2014, the US feeder price premium was 322pc higher than Australian prices, following the US’s previous drought-driven shortage. Back then, Australia’s feeder steer indicator was sitting at only 190c/kg.

US female slaughter remains high

Mr Jackson said there was an interesting dynamic occurring in the US industry, with destocking continuing in earnest this year helping fuel demand and price for feeders.

“The US female slaughter ratio (the percentage of females included in weekly kills, with 47pc being the tipping point between contraction and expansion) is still well above 50pc,” Mr Jackson said.

“But at the same time, slaughter had come right back, because the destock has been so substantial.”

Feedback from US market watchers is that US processors are presently just trying to get whatever slaughter cattle they can, paying big money for all cattle in an attempt to maintain throughput, in a rapidly dwindling supply pool.

That’s only re-incentivising US cattle producers to continue to sell females, in what is already a drastically depleted national cow herd. Recent figures have put the US beef cow herd at 50 or 60 year lows, depending on the source.

That’s just digging the US herd recovery hole even deeper, and heightening the demand for feeders even more.

“No-one’s really sure where it is going to end up,” Mr Jackson said, “but it’s all signalling, at the very least, that the US beef industry is getting very short on supply of raw material.”

Beef competition

The good news for Australian beef exports is that the feeder price divergence will help make Australian beef exports – particularly grainfed –much more competitive against US beef supplies in markets like Japan, Korea, China, and even the US itself.

As part of this, there is a growing feeling in the Australian export trade that we might see more Australian chilled grainfed cuts entering the US over the next 12 months (as opposed to frozen manufacturing beef used for hamburgers, which dominates our current trade into the US).

One large grainfed beef supply chain manager thinks greater grainfed chilled cuts exports are “absolutely on the cards” for the next couple of years, to fill the looming gap in US production.

That’s particularly likely, given Australian cattle on feed reached the second highest level on record at the end of June, reaching 1.256 million head.

“This is looking likely a really long, protracted period of low supply out of the US beef production system,” MLA’s Tim Jackson said.

Much of Australia’s current grainfed exports to the US tended to be niches like longfed Wagyu, he said, but less so in more mainstream, higher volume 100-day grainfed beef.

Independent analyst Simon Quilty agrees that there are prospects ahead for more chilled Australian grainfed beef into the US.

However he suspects there is a lot more Australian grainfed chilled beef entering the US than current trade data indicates.

One of Australia’s largest grainfed beef supply chains has indicated that it often exceeds MLA’s own grainfed chilled volume data on its own, suggesting there may be some reporting irregularity.

On Australian feeder cattle prices, Mr Quilty sees 2023-24 as being in a ‘holding pattern’ around 330-340c/kg liveweight, climbing rapidly to 470c in 2025, before hitting record highs of 610c/kg in 2026, and 630c/kg in 2027.

“These are optimistic numbers, but as the US tightening in beef supply occurs after three years of savage drought, I truly believe our feeder prices can get to these levels,” he said.