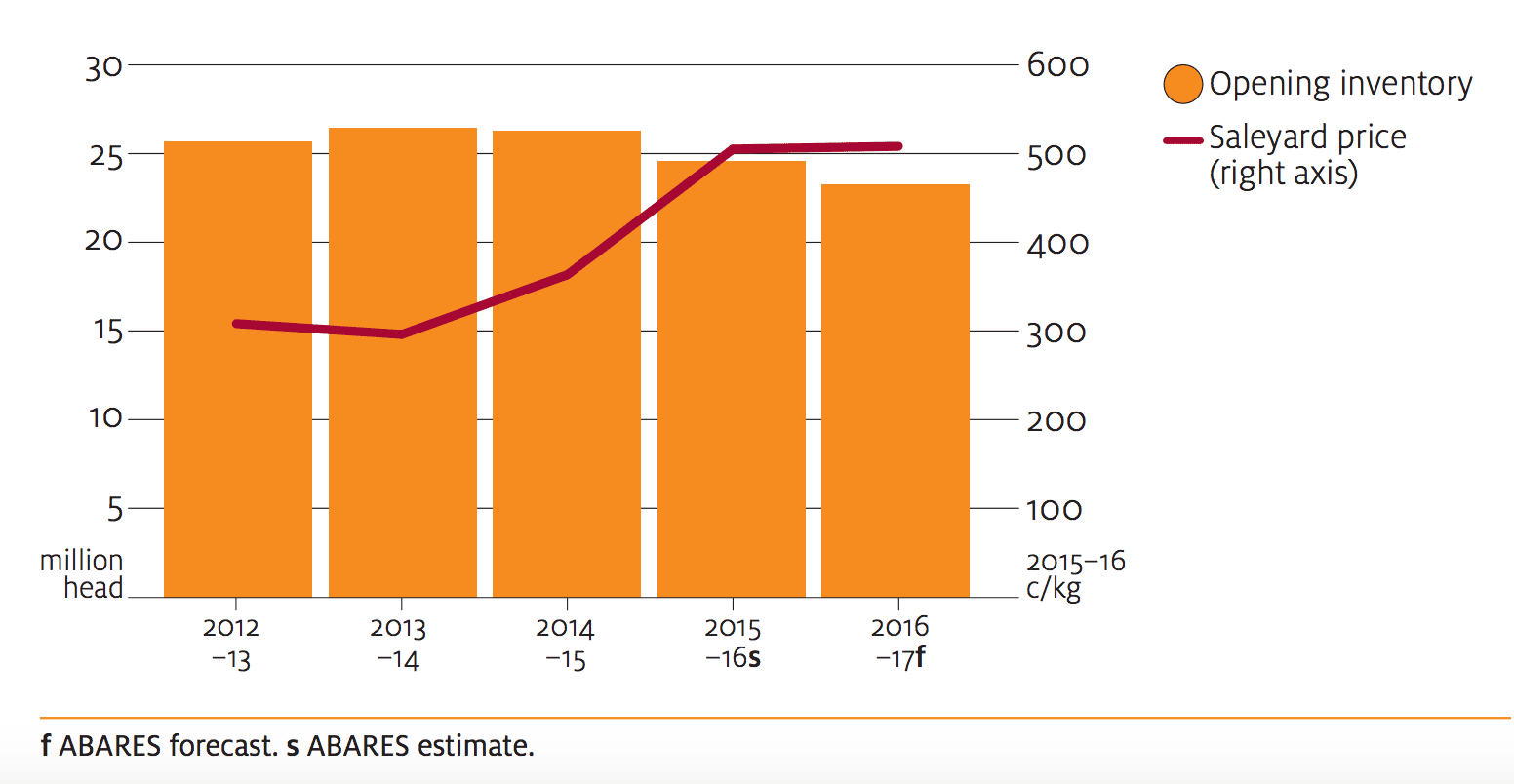

Opening inventory and weighted average saleyard price of beef cattle, 2012–13 to 2016–17. All charts from ABARES. Click on charts to view in larger format

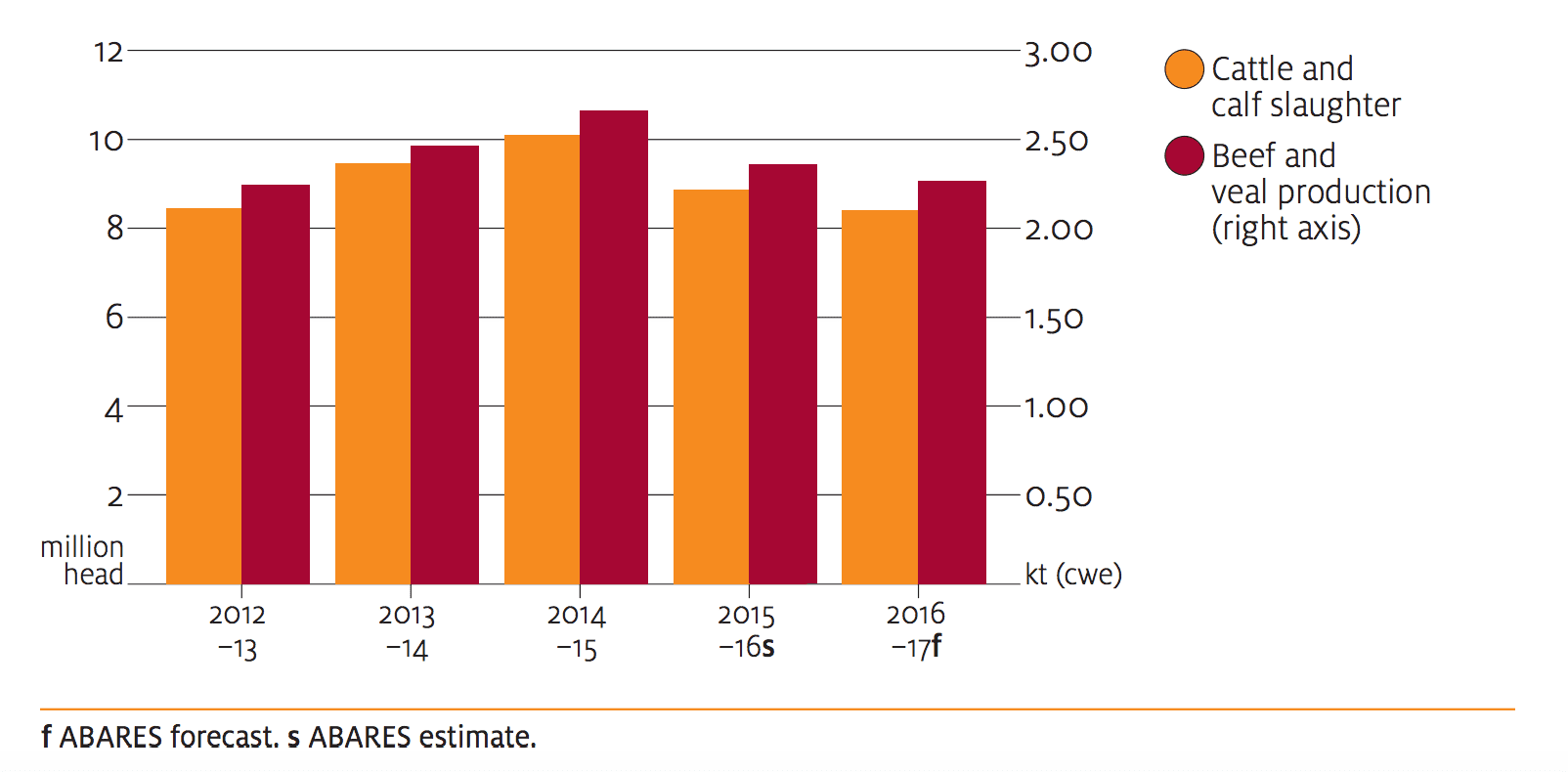

Cattle and calf slaughter and beef and veal production, Australia, 2012–13 to 2016–17

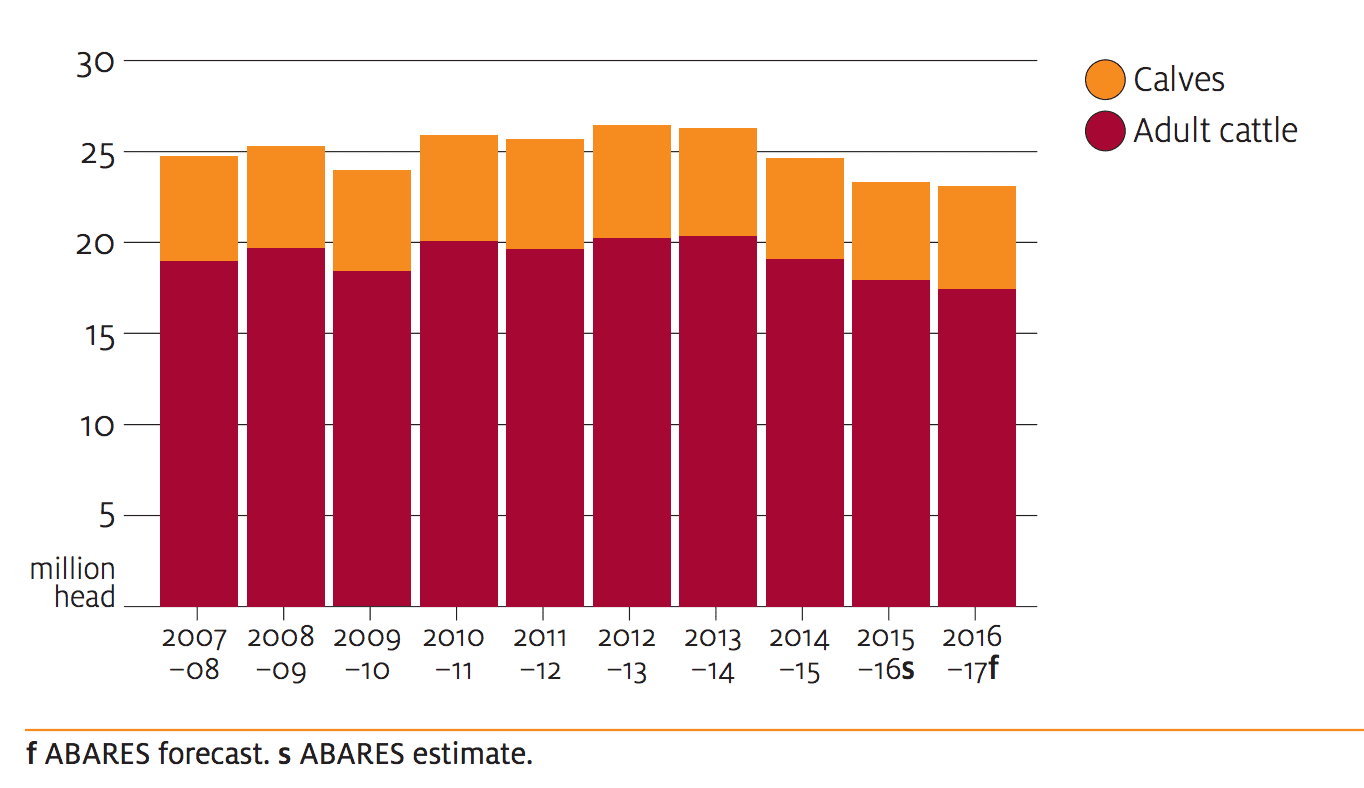

Beef cattle and calves as at 30 June, Australia, 2007–08 to 2016–17

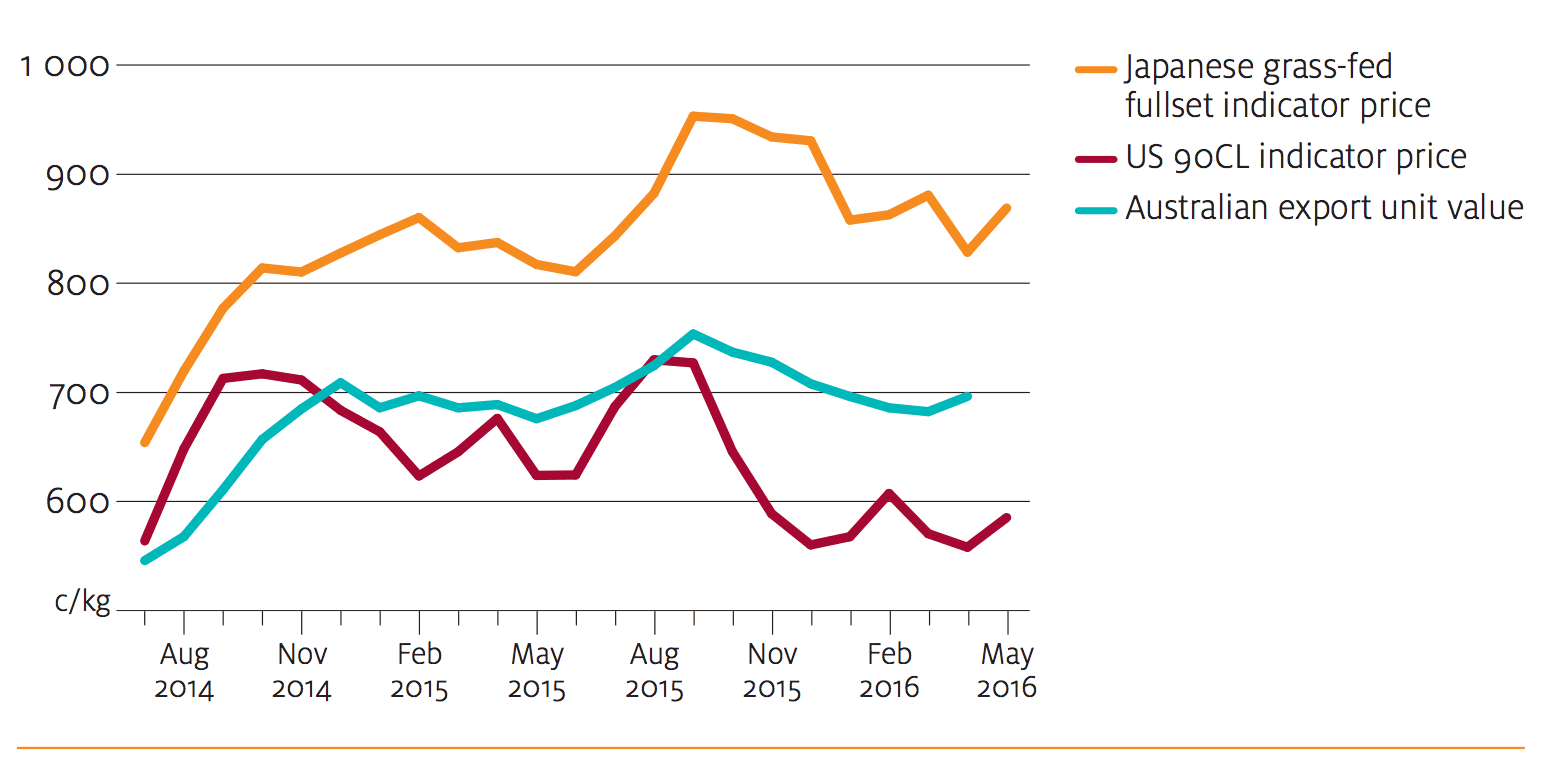

Average Australian beef export unit value and international beef indicator prices, July 2014 to April 2016

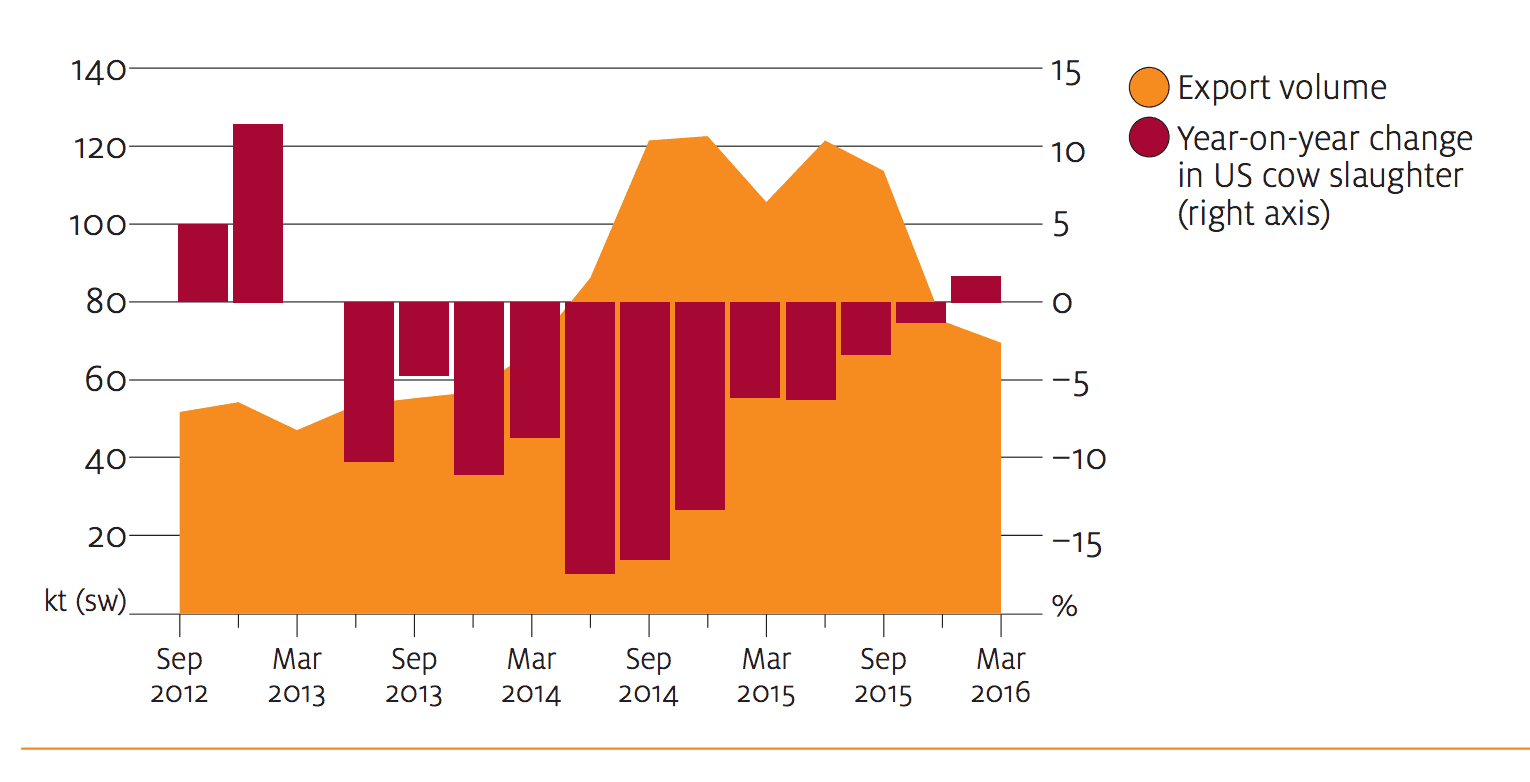

Year-on-year change in quarterly US cow slaughter and Australian beef exports to the United States, September 2012 to March 2016.

Australian saleyard cattle prices will be pulled in opposite directions by supply limitations and diminishing export returns in the next 12 months, according to ABARES’ mid-year market outlook statement.

On one hand, assumed wetter seasonal conditions, underpinned by forecasts of an emerging La Nina, will encourage more herd rebuilding and place further limits on available supply to market, putting upward pressure on saleyard prices.

On the other hand, increased supplies in primary export markets will continue to exert downward pressure on Australian beef export prices.

The supply side is set to win the price tug-of-war in the short term, ABARES’ latest price forecast, released this morning, suggests.

The weighted average saleyard price of cattle is set to finish the 2015-16 year at 505c/kg, a massive 41 percent higher than the previous financial year. (And well above ABARES’ prediction one year ago of a 425c/kg price average).

The increase in herd rebuilding activity has given ABARES reason to believe saleyard prices will rise a further two percent this year to average 517c/kg in 2016-17.

However it notes that the impact of downward pressure being exerted on Australian beef export prices has already been felt in the market.

After reaching a peak of 535c/kg in September last year, when widespread rainfall across eastern Australia triggered a surge in restocker demand, saleyard prices then began to fall away, dropping by about 10pc to a level of 480c/kg in April this year.

The decline largely mirrored a corresponding 8pc fall in average export unit values for Australian beef and veal between September 2015 and April 2016.

A forecast increase in beef supplies to Australia’s major export destinations from other sources is expected to continue to place similar downward pressure on Australian beef export prices in 2016-17, ABARES says.

Forecasts for 2016-17 in today’s outlook include:

- Cattle slaughter is forecast to decline by a further 7pc to 8.2 million head, with the share of female cattle in the slaughter expected to reduce markedly.

- Fewer female cattle in the slaughter, together with relatively high feedlot turn-off and an assumed improvement in seasonal conditions, is expected to result in an increase in average slaughter weights.

- Australian beef and veal production to decline by 4pc to around 2.3 million tonnes.

- Beef cattle herd to fall for fourth consecutive year, from an estimated at 23.3 million head on June 30, 2016, to 23.1 million head on June 30, 2017.

- Australian beef and veal exports to fall by 6 per cent to around 1.10 million tonnes (shipped weight).

- Australian beef (mainly manufacturing beef) exports to the United States are forecast to decline further in 2016–17 to around 290 000 tonnes, 15 per cent lower than in the previous year, mainly due to increasing US domestic beef production. Average export unit values are also forecast to decline by around 4 per cent, resulting in the value of Australian beef and veal exports to the United States falling by 18 per cent in 2016–17 to $2.1 billion.

- Australian beef and veal exports to Japan are forecast to fall by 4pc to 255,000 tonnes, due to high retail beef prices compared with poultry and pork, and increased export competition from the United States.

- Australian beef and veal exports to the Republic of Korea are estimated to increase by 4 per cent to 180 000 tonnes, reflecting declining domestic production in Korea which is unable to meet growing demand.

- Australian beef and veal exports to China are forecast to increase by around 4pc to 135 000 tonnes. However, Australia’s share of total beef imports into China is forecast to continue to decline, primarily as a result of expanding imports from Brazil. This will also place downward pressure on export unit values in the coming year.

- Live cattle exports are forecast to increase by around 5 per cent to 1.18 million head, valued at around $1.3 billion. Growth in live cattle exported to Vietnam is forecast to slow as live cattle prices remain relatively high.

To read the full forecast on the ABARES website click here