PLANT based meat producer Beyond Meat has delivered more disastrous financial results, highlighting prolonged weakness in the global plant based meat category.

Fourth quarter earnings delivered late last week showed another 19.7 percent year-over-year decline in revenue, to US$61.1 million.

Gross profit plummeted to US$1.4m, from $10m in the same quarter last year. The gross margin plunged to just 2.3pc, down from 13.1pc a year ago.

Net income jumped to $410m up from a net loss of $45m in the year-ago period – but that was buoyed by a $548m non-cash gain on debt restructuring. Adjusted pre-tax earnings showed a loss of $69m, which was much worse than last year’s loss loss of $26m.

Net income jumped to $410m up from a net loss of $45m in the year-ago period – but that was buoyed by a $548m non-cash gain on debt restructuring. Adjusted pre-tax earnings showed a loss of $69m, which was much worse than last year’s loss loss of $26m.

The company ended its fourth quarter with $217.5m in cash, cash equivalents and restricted cash, against $415.7m in total outstanding debt.

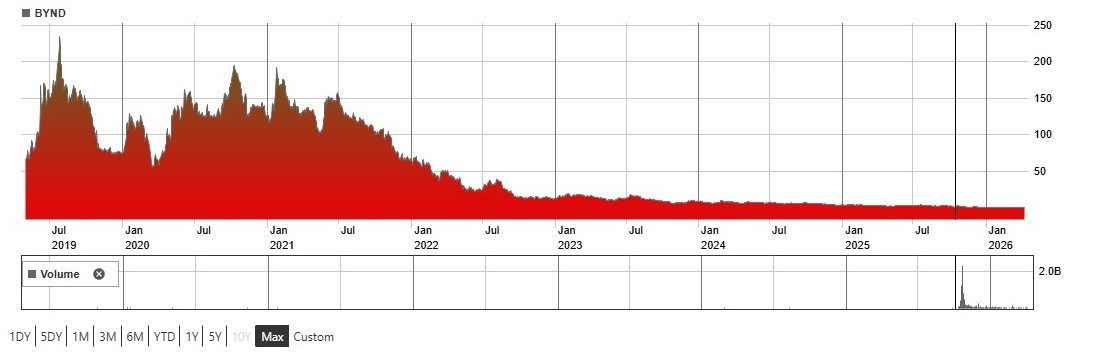

Beyond Meat has had a spectacular history on the New York Stock Exchange, by any standards. Floated at US$25 per share in 2019, the company saw its share price skyrocket to more than $196 at its fever-pitch height in 2019, when plant based meat pledged to make conventional meat irrelevant.

The shares spiked again in 2021 during the tech boom to around $180, but since then, as can be seen in this graph, the decline has been both sustained and deep. Stocks today are worth about US60c, down another 27pc year-to-date, and losing 99.7pc of their value from their highest point.

In a limited guidance to the market, the company last week said it “continues to experience an elevated level of uncertainty within its operating environment.”

The big surge in demand for animal protein that’s been experienced over the past year or two has only added to Beyond Meat’s challenges.

Chief Executive Officer Ethan Brown told the market the results reflected ongoing headwinds in the plant-based meat category, along with the financial impact of restructuring initiatives to put it on a path to sustainable operations.

Chief Executive Officer Ethan Brown told the market the results reflected ongoing headwinds in the plant-based meat category, along with the financial impact of restructuring initiatives to put it on a path to sustainable operations.

“We enter 2026 with reduced leverage and extended debt maturity, and having added liquidity to our balance sheet,” he said in the earnings release. “We intend to build on these improvements through the continued pursuit of top-line stabilisation and margin expansion.”

“We enter 2026 with reduced leverage and extended debt maturity, and having added liquidity to our balance sheet,” he said in the earnings release. “We intend to build on these improvements through the continued pursuit of top-line stabilisation and margin expansion.”

Last month Beyond Meat was warned by the NYSX about possible delisting, based on the stock’s performance.

The company is also recently rebranded itself to “Beyond, The Plant Protein Company”, which it believes will allow it to enter other food categories, including not only meat substitutes but other areas of plant-based food and drinks.

A month ago Mr Brown told financial media “It’s just not the moment for plant-based meat.” He told the Associated Press that he still believes plant-based meat could become a much more dominant choice in the coming years, but that Beyond has to navigate what he referred to as a “period of confusion” around plant-based foods.

Climate solutions rating

In April, the company’s BeyondBurger and BeyondSteak products became the first plant-based meat products to qualify as ‘Climate Solutions’.

The ratings were based on the criteria and safeguards outlined in the Climate Solution Framework, developed by the Exponential Roadmap Initiative in collaboration with Oxford Net Zero. A climate solution, as defined by ERI, is a product that contributes to emission reductions at a global level by producing significantly lower (at least 50pc less) emissions than the weighted average of current market options.