FOUR key factors would drive cattle and sheepmeat prices for 2020 and 2021, independent meat and livestock industry analyst Simon Quilty told a webinar hosted by NSW Local Land Services on Wednesday evening.

Simon Quilty

African Swine Fever, COVID-19, and the supply and demand disruptions caused by these diseases and other factors like drought would dictate cattle and meat price trends this year and next, he suggested.

The latest outbreak of African Swine Fever had happened last week in two northeast states in India, he said. In March, ASF was found in East Timor and Papua New Guinea, just 550km from Australia.

“ASF is now present in 13 countries, which collectively account for 532 million pigs. China, alone, accounts for 441 million of those. In the majority of these countries, the expectation is for pig losses of 50-60pc, representing around 255 million pigs lost,” Mr Quilty said.

“That type of deficit is going to create a major global protein shortage. It’s already been seen in China, through the enormous protein importation that have occurred over the past 12 months.

“The Chinese government is desperately trying to keep domestic pork prices down, having some impact by regularly releasing frozen pork stocks out of storage for the past 12 months. But there is a finite limit to those frozen stocks, and the role of beef and sheepmeat, as well as imported pork, will be important,” he said.

Beef, surprisingly, had become the key ‘filler’ in the absence of domestic Chinese pork – much more so than chicken.

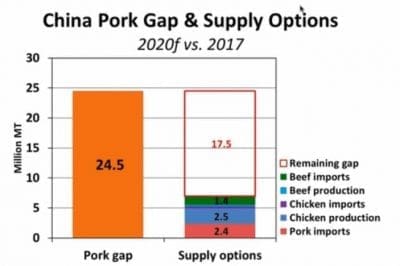

“Effectively China has a 24.5 million tonne protein supply gap to fill, as a result of ASF,” Mr Quilty said.

“As the graph above shows, even if the Chinese increase imports of beef, chicken, sheepmeat and pork, and manage to increase domestic pork production to try to fill the deficit, we believe there is still a 17.5 million tonne protein deficit to fill, each year for the next three years.”

COVID-19

Until a vaccine is found for COVID-19, seasonal disruption to both northern and southern hemisphere beef markets could become an ongoing problem for many years, Mr Quilty said. This would create opportunities for packing and processing facilities that manage to remain free of COVID-19.

“That sums up what we have seen recently in North America and Brazil,” he said.

“It’s all about the disruption to demand and supply, and what that is doing around the world.”

“If, as some people believe, the virus spread will slow in warmer temperatures, there will be an oscillation globally, affecting agriculture markets. As the northern hemisphere moves into its summer, for example, infection rates may fall away naturally.”

But 88pc of the world lived in the northern hemisphere, and 95pc of Chinese beef imports come from the southern hemisphere.

“As the southern hemisphere moves into its winter months, the expectation is that the flu season will get worse. The end result is that we could see an improvement in beef demand in the northern hemisphere over the next six months, and increased disruptions in the southern hemisphere, as more and more COVID infections occur in meatworks across Brazil, Argentina, Uruguay, Australia and New Zealand.

These points are covered in greater detail in this earlier Beef Central article.

“The answer, to me, is for processors to remain COVID-19 free, and they have a distinct market advantage,” Mr Quilty said

Disruptions to demand

Mr Quilty told the webinar audience that in his 30 years as a meat trader, he had not seen market failure like that seen in the global food service sector this year as a result of COVID-19.

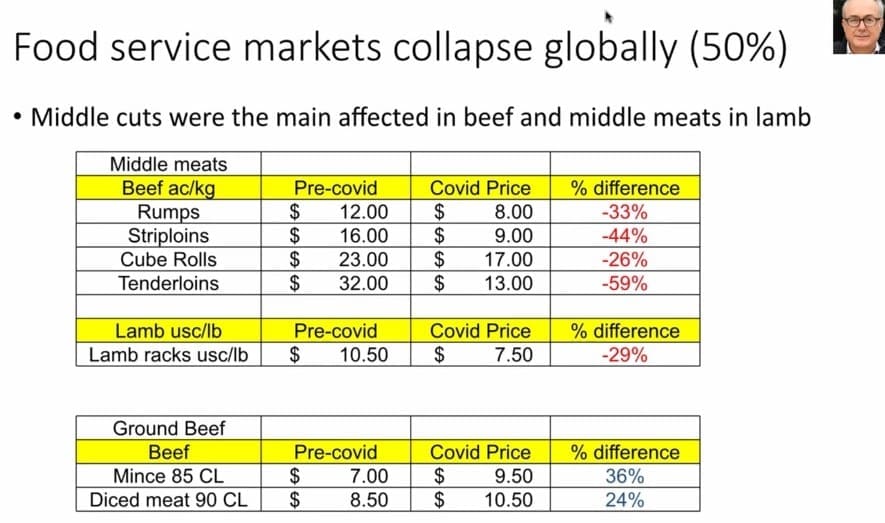

“Food service (restaurants, casual dining outlets, fast food etc) typically made up 51 pc of beef sales. In pork, the figure is around 25pc, and in lamb 35-40pc. So food service is absolutely critical, particularly in selling items like the middle cuts – striploins tenderloins, cube roll, and rumps – all of which traditionally go into foods service.”

“Literally, these food serviced markets have shut down, overnight. As a result, we have seen some dramatic impacts in Australia on the market.

One of the results in the US right now was high unemployment, currently sitting at 25pc, due to COVID-19 business closures.

“When there is high unemployment in North America, there is a downturn in meat consumption – for pork, chicken and beef. Right now, the value of beef is two and a half times that or pork and chicken in the US market, and one of the real concerns is that with high unemployment in north America and around the world, people will look for cheaper proteins, than eating beef and lamb.”

On top of meat plant closures, port, freezing and transport blockages had caused key problems in supply.

“February really was the worst stage for this, in terms of China, while the US is still in the middle of it, as we speak. But I’d like to say we are through the worst of it,” Mr Quilty said.

What has been the impact here in Australia?

Because Australian is 70pc reliant on export, middle cuts were easily the worst affected, he said. Some had come back onto the domestic market, because they simply could not be sold in other places.

Rumps, for example, had fallen 33pc compared to pre-COVID figures; striploins fell 44pc; cube rolls 26pc; and tenderloins fell almost 60pc.

If we were to talk about Wagyu, the figures look even more dramatic, in terms of the fall in prices, because there simply isn’t a home for them in the export trade,” Mr Quilty said.

In sharp contrast, ‘comfort foods’ like ground beef prices (being sold through retail outlets, where there was a real desire for that cheaper product, which freezes well) were up 36pc, and diced meat up 24pc. “That’s where the real demand has been,” he said.

US market performs differently

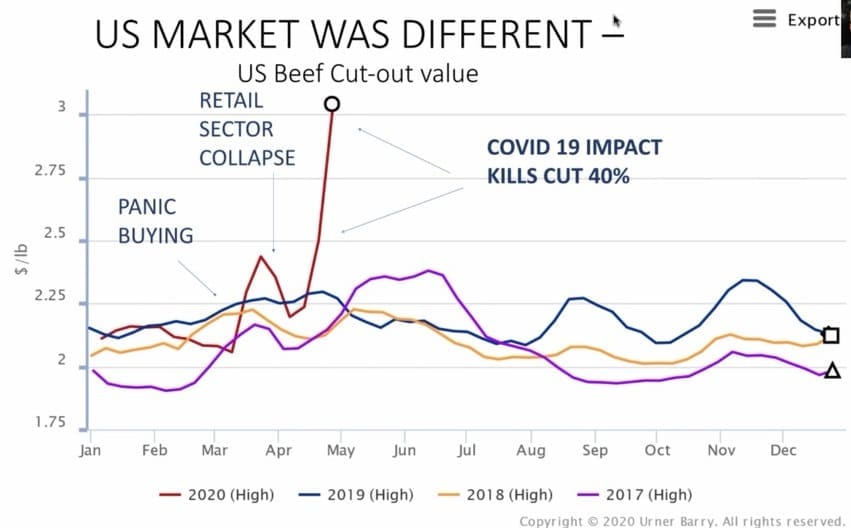

The US market had performed differently to the rest of the world, however.

While the US food service sector did shut down, the retail sector expanded (by another 10-15pc), and took additional beef and lamb.

There had been several phases in the past two months, Mr Quilty said.

First there was panic buying, like that experienced in Australia in March (see graph). Prices picked up dramatically, as a result, and this was followed by the collapse in the US food service sector. As COVID started to take its toll throughout the meat industry in North America, supply became so tight that even though food service was shut down, there just was not enough supply to meet the retail needs.

“As a result of all this, meat prices in the US have gone through the roof. But that had not been without its cost – a dramatic fall in cattle prices across the US – about 20pc.

US supply declines

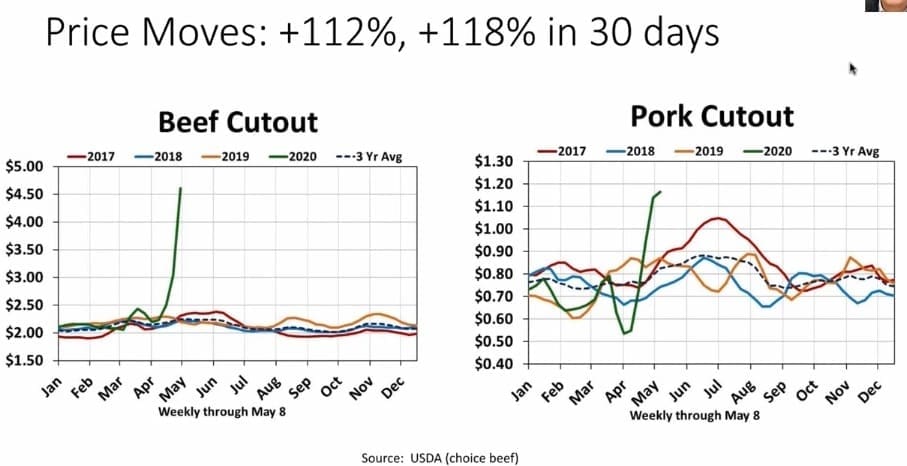

For reasons around COVID-related plant closures discussed above, US beef production was down 32pc last week, and 40pc the previous week, versus the March average. Pork production was down a similar amount, for the same reasons.

“The small improvement last week versus the week before suggests that some meat plants are starting to get the problem under control,” Mr Quilty said.

“But as of early this week, there have been 30 US meat plants affected by closures or cutbacks. That has led to retail shortages, and meat price surges in North America.”

The impact had been dramatic, in terms of retail and wholesale meat prices. The US beef cutout (wholesale prices for every individual item, as if the carcase had been glued back together) were up 112pc on the past 30 days (see graph).

“Retail prices showed the biggest one-month increase since 1974, with USDA Choice peeled knuckles up 136pc over the past month, and Choice tenderloins up 130pc. Contrast this with tenderloin prices in Australia than have fallen 40pc in value,” Mr Quilty said.

At the same time, US cattle prices have collapsed. While America has been feeling the pain of a 20pc decline in cattle price since January, in Australia, year-on-year, heavy steer prices were up 11pc, and feeders up 24pc.

“So what is the net effect when the US has falling cattle prices and rising beef prices? Someone is making some money – and right now it is the US processors. In the past week, they made (on average) US$1500 a head on slaughter steers, and anticipated to go to $1700/head next week,” Mr Quilty said.

“That is extraordinary – margins never seen before in the North American market, and simply because there is that restriction of processing, and the cattle cannot be killed, and slaughter-ready cattle are backing up through the system. It’s believed right now that there are 600,000 head of cattle backed up through the system. In the next two weeks, that could grow to 1.5 million head.”

“No wonder US cattle prices are falling – and in the meantime meat prices are skyrocketing, right across America.”

Green shoots appearing

Despite the challenges, beef demand was starting to improve globally, and there were good reasons for that, Mr Quilty said.

“We now have what I’d describe as a supply-driven market, rather than demand-driven.

“Global COVID restrictions are starting to lift, and we have supply getting tighter out of Australia and the US, through our feedlot sector.”

The IMF had recently come out with a report predicting global economic growth of negative 3.4pc for 2020 (up from +3.3pc forecast back in January).

“However the IMF’s outlook for 2021 is amazing – they have gone from a January prediction of +3.4pc, to +5.8pc. That is the bounceback effect,” Mr Quilty said.

But behind all this is the underlying assumption that a COVID vaccine is found in the meantime – otherwise that growth figure would not occur next year.

Within the IMF forecasts, it predicts China economic growth next year at 9.2pc, providing the engine-room for global growth. The US is forecast at 4.7pc and Australia, 6.1pc.

Mr Quilty said he had been trading meat into the US over the past three weeks, and product that three weeks ago was worth US220c/lb CIF, which was on Wednesday worth 240c.

“In three weeks, we’ve had a 10pc rally in 90CL beef, and we are starting to see all the benefits of that tight supply in North America made available to supplier countries like Australia and New Zealand,” he said.

It’s very much like what happened in 2014, when the market went into a supply-driven phase, due to the lack of cattle supply in the US. Right now, Australia is experiencing the same thing.”

The USDA has recently dramatically revised its figure for US beef production for this year.

“It’s a stark turnaround. They have now removed 762,000t of beef from their 2020 forecast – a 5.5pc reduction on 2019,” Mr Quilty said.

“Even before these figures were put out, US meat traders were saying, this market feels like 2014 – that’s the reason why.”

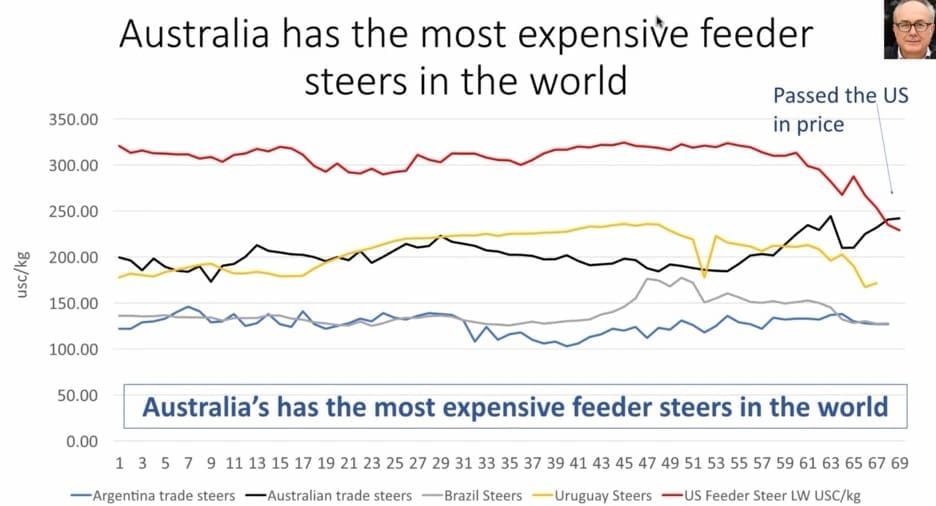

Feeder steer prices

Right now, Australia had the most expensive feeder steers in the world, Mr Quilty told the webinar.

Beef Central covered this topic in this earlier article.

“In comparison with our competitors like Brazil, Uruguay and Argentina, we’re currently 75pc above the value of Brazilian and Argentinean cattle, as we speak,” he said.

“We are 31pc above Uruguayan cattle and 3pc above the US in value. The remarkable fall in US prices has been brought on by COVID-19, in which kills in North America have fallen 40pc in the past three to four weeks.

“That would be the equivalent of losing JBS and Cargill, together, in the marketplace. And so the impact has been quite dramatic in terms of cattle prices in North America.”

As a result of this ‘market failure’ in North America, Australia had stepped forward as the number one country in the world, in terms of feeder prices. Under normal terms, the US would be well ahead of Australia, Mr Quilty said.

“The fact we have had a devastating drought has been a huge part of that, so there are a lot of factors driving why Australia’s feeder steer prices are high, but this makes it a struggle to be competitive in international markets when feeder prices are at this level.

The record high peak in the market came on 12 March, NLRS data shows, when feeder steers go to 405c and heavy steers 341c and cows 268c/kg liveweight.

Mr Quilty made predictions back in 2018 that the EYCI would rise to 750c in early 2020. While the market has in fact ‘overshot’ that prediction by 15c, ‘nobody would be complaining’, he said.

Currency factor

A critical part of current Australian feeder cattle pricing is currency. The A$ is down 19pc against the US$ since March 2018. Over the same time frame, the Brazilian currency is minus 41pc, the Argentinean Peso minus 70pc – extraordinarily low currencies – as a result of the trade war and COVID-19, making South American supply even more competitive.

“Looking at it another way, 78pc of China’s beef imports are coming from countries with currencies that are on average 45pc below the US$, compared with Australia at 19pc, Mr Quilty said. “It’s a stark reminder how important currencies are, and how competitive South American countries are in world beef trade.”

It begs the question: are we going to see falling prices next year in North America? This topic will be covered in a second webinar featuring Simon Quilty being held next week. Stay tuned for a report next week on Beef Central.