AS weekly rates of slaughter across Australia begin to climb again after the Easter break, the question is again arising: Do processors have the manpower to keep up with this year’s supply, and if not, what happens to cattle prices?

It’s a point being pondered as the industry approaches its traditional peak turnoff and slaughter period for the year.

Short processing weeks due to holidays and rain disruptions aside, there’s been a sharp rise in adult cattle slaughter this year since around week six, ending 9 February.

Short processing weeks due to holidays and rain disruptions aside, there’s been a sharp rise in adult cattle slaughter this year since around week six, ending 9 February.

National Livestock Reporting Service data shows that the eight full working weeks since then have averaged almost 131,000 head, up around 20,000 head compared with the same period last year.

Despite some big setbacks due to weather (JBS Dinmore and several others lost a day’s kill due to weather related supply challenges) last week’s seven day kill lifted again to above 131,000 head. The same week last year accounted for only 83,000 (albeit Easter affected), and the year before that, 96,000 head.

Adding to the larger kills, the female slaughter ratio (percentage of females in the overall kill) has exceeded 47pc for each of the past four weeks, and gone as high as 50pc the week before last. Forty seven percent is regarded as the tipping point between herd expansion and contraction.

The results from early first-round muster preg testing, together with cash flow pressures, may have contributed to that recent climb in female slaughter, with empties being tipped into the market, one processor suggested on Tuesday.

Rising prices for frozen manufacturing beef in export markets was another factor in the rise in cow slaughterings, he said.

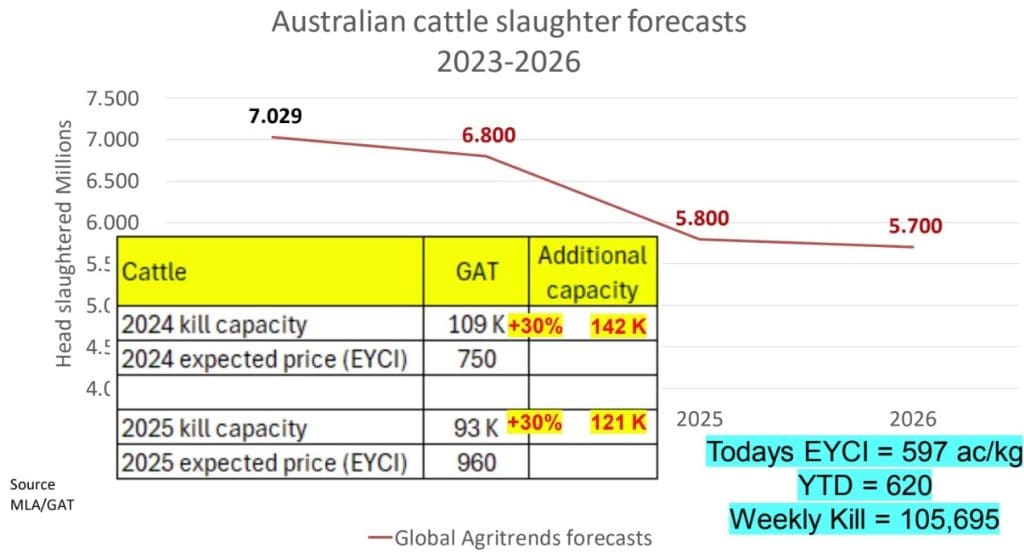

Speaking during last week’s Wagyu conference in Cairns, independent analyst Simon Quilty told the audience that under his calculations, the processing sector needed to find enough labour to process 142,000 cattle a week during busy times this year, in order to “see the industry through” (see graph above).

“Over the past two to three years, it’s been challenging,” he said.

“Fortunately, there’s been an increase in the number of offshore visa holders working in Australia, rising from 49,500 in the middle of COVID to around 68,000 today.”

Not all of those are working in meat processing, however.

There’s also increased production capacity that’s occurring across five major meatworks across Australia – JBS Dinmore being the largest of them. While Dinmore has added a second shift, each shift at the plant is currently working only four-day weeks, with current daily capacity at around 2400 head – still far short of the plant’s two shift full potential of 3400.

Beef Central wrote about the rise in new industry capacity in this article last year.

Mr Quilty put the rise in capacity due to plant expansions, shift additions and expanded labour at around 3000 head per day this year.

“Recent weeks have produced kills around 136,000 – and thank goodness,” he said. “At the height of last year’s production seen around October, kills were around 131,000 – but things are now improving.”

As illustrated in his slide below, Mr Quilty estimates this year will require capacity of around 142,000 head over the next three to four months, as the current southern liquidation goes on, but hopefully pulls up around mid-year.

“So we appear to be close to meeting our needs,” he said.

Other processing sector contacts have told Beef Central that realistic processing capacity this year, given current labour constraints, is likely around 135,000 head, suggesting the supply chain is already close to its physical capacity. Last year that figure was around 115,000-120,000 head.

What happens if slaughter-ready cattle supply drifts too far beyond that 135,000 head figure remain to be seen, but a surplus of cattle to capacity cannot auger well for pricing..

Large migrations of slaughter cattle from one state or region to another could become more commonplace, as local supply cycles ebb and flow, one large export processor contact suggested.

Why is there never any info about WA? We are screwed by a lack of processors, and slaughter rates appear not to be reported. We are part of Australia and pay our levies. When the East was in drought we sent hay. Drought here now and I don’t hear too much about hay heading West. Actually, don’t hear anything west of WA.

Thanks for your comment, John. WA slaughter data is reported weekly by NLRS, along with the eastern states. For a long time, WA processors did not choose to report their weekly kill figures, hence the report was previously called the Eastern States Slaughter Report. That changed around five or six years ago, to today’s National Slaughter Report. Reporting by processors remains voluntary, however – clearly reflected in the WA figures. Last week, NLRS reported a state kill of only 2740 head, or less than 550/day. Clearly light-on.

Regards your comments about beef industry coverage in WA, we agree with you – there isn’t enough – but to be fair, WA tends to operate in isolation from the eastern states in cattle supply/demand, due to the distances involved. Editor

There is another point to ponder. Why would any processor want to increase production.

If there is a constant over supply leading to processors able to name their price and make huge profits, why would they want that to change by increasing production and risk creating a shortage of cattle.

In the past we have seen modern abattoirs like at Murgon bought up by a big player and then never processed a beast ever again. Essentially removing processing capacity from the system.

I also question whether there really is a labour shortage with hundreds of thousands of new people coming into the country every year.

With more and more cattle in feedlots it would make sense we need more processing capacity, but you can simply not snap your fingers and instant processing plant which creates an ideal situation for anti-competitive practices.

A major change is about the only thing that will move us away from the current trend of producers becoming less and less profitable with them fighting over scraps of the wealth a beast earns by the time it is eaten. That could be a significant proportion of land getting changed to another use or a whole new market opening up or live export out of the north goes absolute gangbusters, removing a large number of cattle from the system.

I cannot see all these predictions of boom times ahead coming true any time soon.

Thanks for your comment, Paul. It’s important to remember that cattle price-setting is not simply dictated by cattle supply – level of demand for beef is also a considerable factor. With current declines in US beef production after years of drought, every export plant in Australia is trying to maximise throughput – just look at our graph on 90CL manufacturing beef prices. Editor