CHINA is making a surprisingly rapid recovery in pork production after the devastating effects of African Swine Fever last year, an international meat trade webinar was told this morning.

The annual Meat Import Council of America conference held every October normally attracts a large gathering of international exporters, importers and traders, including a contingent from Australia, but was held online this year due to COVID.

Len Steiner

US-based industry analyst Len Steiner delivers a presentation to the conference each year outlining world meat supply and demand trends and a forecast on cattle and meat prices for the year ahead.

Among a broad range of topics he covered this year, he suggested Australian lean grinding beef exports to the US next year are likely to retain a price premium over both domestic US trim, and competing imported product from South America (more details below).

As part of an examination of the China market in global meat supply and demand, Mr Steiner said a year ago (after the onset of African Swine Fever) China was outbidding other import competitors for available beef supplies.

“But they don’t seem to be buying as much at this point in time, from Australia or New Zealand – despite leading the world in the recovery from COVID and the recession it caused,” he said.

“Part of that may be political – Australia has been vocal about some of the developments in Hong Kong, for example – and the Chinese have let Australia know that they do not appreciate those comments.”

New Zealand had also shifted a little. For a long time the US had been NZ’s biggest and most consistent customer. Last year that was not the case, as China exports grew, but this year, the US would again be NZ’s largest market, he said.

Rapid Swine Fever recovery

While China’s pig herd was decimated a year ago by African Swine Fever, recovery had been surprisingly swift, and this would potentially impact world meat trade in coming years.

Prior to 2018, China had somewhere around 55 percent of all the hogs on earth, Mr Steiner said.

While precise estimates were difficult to source, statistics suggested China had about 418 million pigs in July 2018, before falling by 37 percent to 264 million by September last year due to the direct and indirect impacts of Swine Fever.

By January this year, the Chinese pork herd had increased to around 283 million head, and Steiner Consulting’s current estimate is that the national herd has now recovered dramatically, to around 375 million head. That suggests Chinese pig numbers are now back to within 10pc of pre-ASF levels.

“They have made a lot of progress lately,” Mr Steiner told this morning’s webinar.

One of the reasons for this was the collapse in Chinese ‘smallfarmer’ pork production, replaced rapidly by large commercial-scale pork production enterprises which could practise bio-security to keep the disease at bay.

“The typical sow shed in the US is a low, flat building. In China, they are now building three-storey sow sheds. They look like a Holiday Inn,” he said.

“It’s a different approach to pork production than what has traditionally been seen in China. They are making rapid progress in recovery. The Chinese are obviously learning how to live with, and effectively manage for the disease.”

At the same time, another reason for the rapid headway in pork production was that pork prices in China had been so high. Retail pork prices are currently around 112pc of what they were a year ago; hog prices 136pc; and baby pigs 174pc higher – almost three times the price of a year ago, Mr Steiner said.

Despite recovery in the pig herd, beef imports to China continued to grow, with roughly 75pc of Argentina’s beef exports now destined for China; about 55pc of Uruguay’s; and 60pc of Brazil’s exports (when Hong Kong is included). A year ago, more than 50pc of NZ’s beef exports went to China, now back to 45pc, while Australian exports represented about 20pc of all exports.

Click on image for a larger view

COVID impact

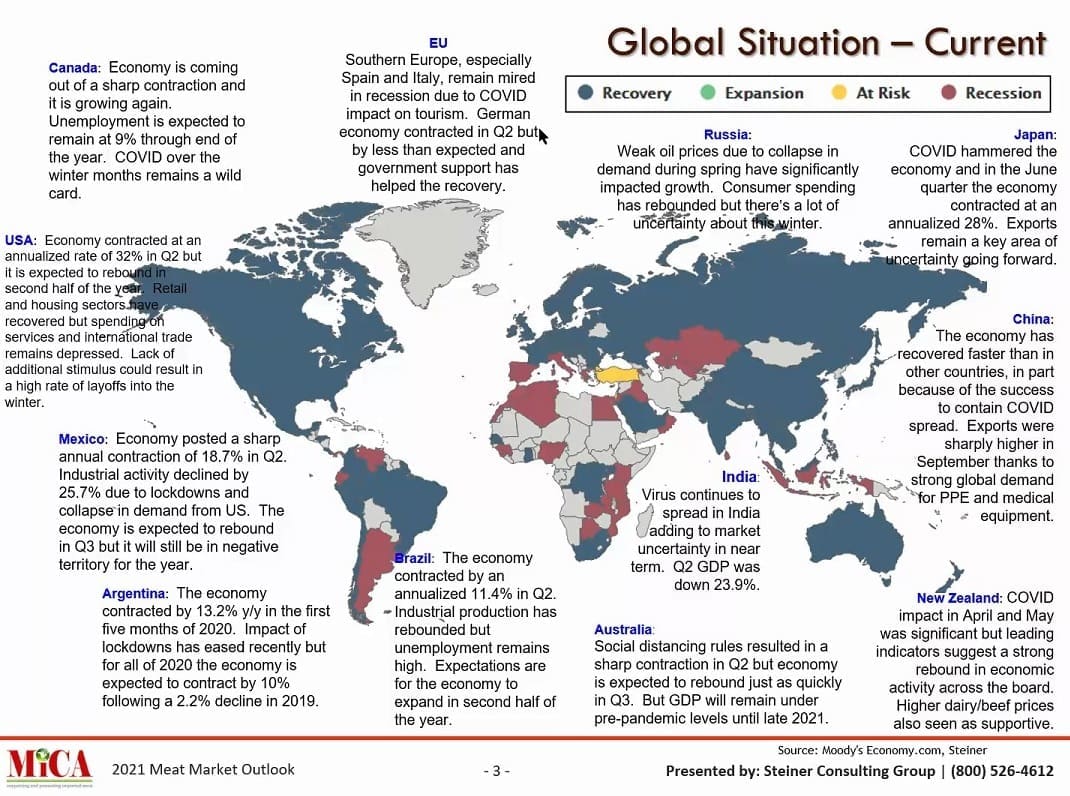

Moving focus from ASF to the other major trade influence this year, Mr Steiner drew attention to the impact that COVID had had on world meat supply and demand in 2020.

“This time a year ago, the US and Canada were doing well, China was on fire, Australian exports and New Zealand were strong, and most of Europe was doing well,” he said.

“Today, things aren’t nearly as rosy,” Mr Steiner said.

Worldwide, the pandemic had caused big problems for all economies, and politicians had been caught between the need to shut down people-movement to hasten the control of the virus, versus taking a softer line to minimise damage to their economies. The effects of this were particularly evident in parts of Europe and the US at present.

“COVID has had a negative effect on the world economy. But whereas normally recessions are bearish for meat prices, this COVID-driven recession has been odd – because parts of the economy remained very strong, at the same time as food charity lines were growing for people who had lost their jobs.”

In terms of recovery, China seemed to be leading the way, as measured by its success in limiting COVID re-infections, and its economic performance measured by GDP.

In 2020, every world region was negative for GDP growth, but for 2021, every region was forecast positive for GDP growth, according to forecasters Moodys.

“The expectation is that COVID will subside, and we will figure out a way to get it under control. Nothing is for sure but it feels like progress is being made on a vaccine,” Mr Steiner said.

As far as the US economy was concerned, better-educated people on higher incomes were tending to cope better with COVID, often able to work from home and use tools like Zoom, whereas people on lower incomes were suffering much more.

This had had an odd impact on meat demand, Mr Steiner said.

“Some of the meat cuts that you would expect to suffer during a recession are not being hurt, and other items that in a ‘normal’ recession would hold-up pretty well, have not done so well,” he said.

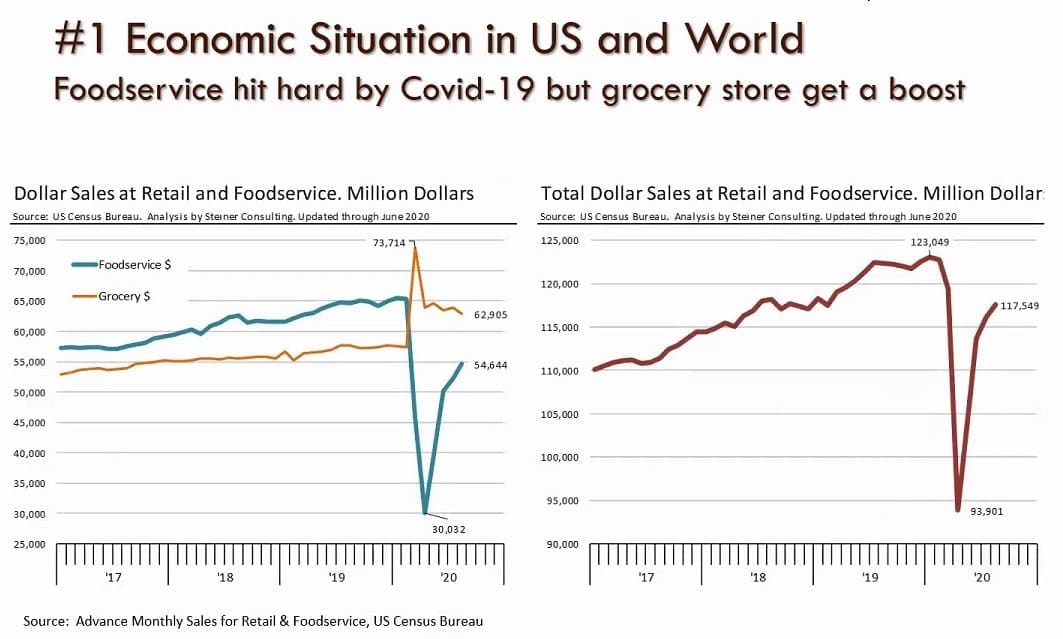

Food service clobbered

As had been seen worldwide, the US food service sector (everything from restaurants and hotels to quick service restaurants like McDonald’s) had ‘really got clobbered’ by COVID in the US since April.

Click on image for a larger view

As this graph shows, US food service sales (blue line) collapsed in April, but had certainly come back since then. Conversely, retail grocery sales had moved in the opposite direction in April-May, and while they had since settled back a little, remained significantly above what they were pre-pandemic.

When the combined spend for retail/food service in the US are added (right had graph), the total consumer spend remained below pre-pandemic levels, Mr Steiner said.

“It depends on the type of food service outlet, and where they are. While there has been some recovery in US food service, not all restaurants are doing well,” he said.

“Fine dining has been decimated, while quick service and limited casual segments (including operators like McDonald’s and Burger King) – especially those that had drive-up windows – are again doing pretty well.”

“If the customer can drive up to a window, grab a bag of food and go, they are comfortable with it. But try to make them come into a restaurant, or any hospitality venue, and the US consumer is nervous about it, and that really hurts takings,” he said.

Even fine-dining steakhouses in the US were doing take-out business, which was “better than no business at all – but it’s not filling the void,” Mr Steiner said.

At the retail end, the elevated trade meant supermarkets were no longer having to run cheap promotions (on ground beef, for example) to drive traffic.

“Some people who previously spent money at restaurants are now spending less money at home, on food. It’s part of the reason why they have all this extra money to spend on hot tubs, home remodelling, a recreational vehicle or all the other consumerables that have been mentioned in the press recently,” Mr Steiner said.

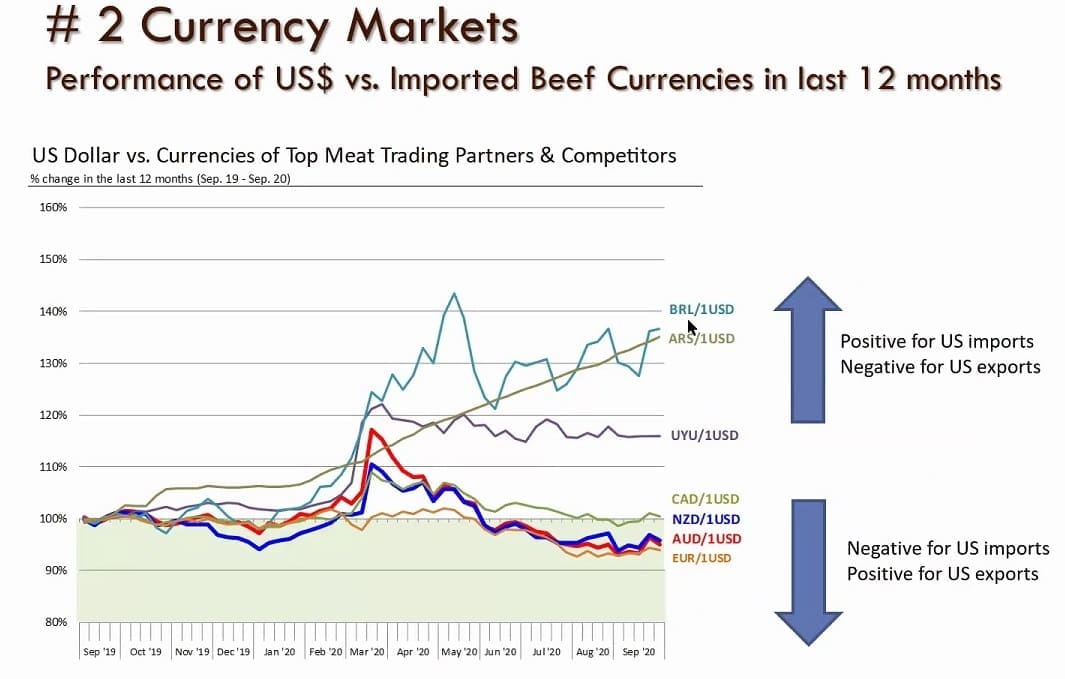

Currency shifts aid some exporters, hinder others

World beef trade currencies, as measured against the US$, had moved in two separate directions over the past 12 months, Mr Steiner told the webinar.

The Australian and NZ dollars had gotten stronger, which was damaging for US exporets, while the Brazilian Real and Argentinean and Uruguan currencies had gotten considerably weaker, adding to their export competitiveness into the US (see graph).

“Clearly South America is going to be anxious to shift product out of the region to get hard currency,” he said.

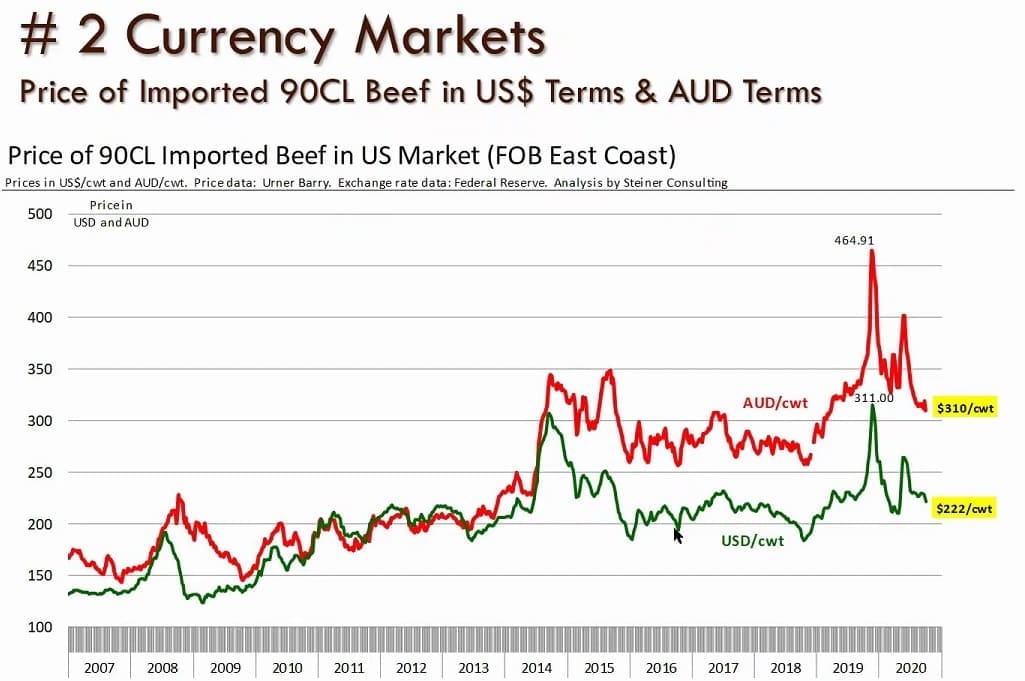

Comparing the price of imported Australian 90CL lean grinding beef with domestic US 90CL, Mr Steiner pointed out using the graph below how it had shifted over time.

“Around 2012, the A$ and US$ were around parity. That’s no longer the case, and certainly currency has shifted recently,” he said.

US corn crop:

Mr Steiner said the US was shaping up to produce its second biggest corn crop in history this year. The USDA supply/demand report issued a week ago suggested production this year would reach 14.7 billion bushels, only a little down from the largest crop in history of 15.14 billion bushels harvested in 2016-17.

The size of the corn crop was really a driver of a ‘lot of things’ in the US, including livestock production, he said. At the same time, exports of US corn were growing, with China entering the market recently, helping drive up the price of corn. China had previously been predominantly a domestic corn user.

December corn futures had recently gone up about US80c/bushel, having gone from around 300c in August to closer to 400c now. Despite that, corn remained reasonably priced, compared with where it had been in the past ten years.

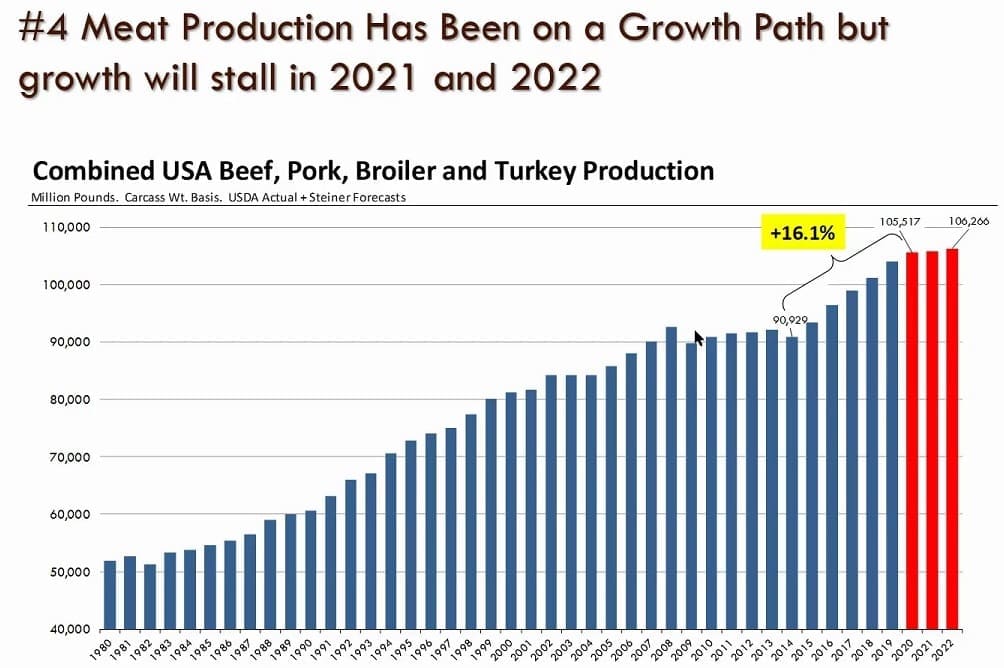

US meat production:

While US production of meat protein (beef, pork, chicken, turkey) had earlier flat-lined at around 91 billion pounds a year for seven years (see graph), production had since grown for the past five years, Mr Steiner said.

“But we see production flattening out now for the next few years,” he said. “We don’t necessarily see it going backwards, but growth is going to pause for a period. In the process, it is going to change per capita meat consumption in the US.”

Pig numbers was down, the beef calf crop had declined for two years in a row, and the chicken industry had its own problems, placing fewer eggs in incubators, as it moved to match supply with US demand.

Steiner Consulting anticipates that total cattle numbers in the US will be down, for the second consecutive year – moving down about 0.1pc to 94.3 million head in January next year. Beef cow numbers are expected to be down 0.8pc to 31 million head by January.

While the long-term trend in US steer weights was up, the trend line had flattened out recently, as suppliers were wary about being penalised for over-weight carcases.

Extreme low prices seen for slaughter cattle back in May, after closure of meat plants due to COVID caused a backlog in supply, were likely to be the lowest for some years, Mr Steiner said. Longer term, US cattle prices are expected to trend a little higher than today’s levels.

While US cow/calf operators had not enjoyed profitability over the past couple of years, Steiner’s forecast is that some profitability will return to the sector next year.

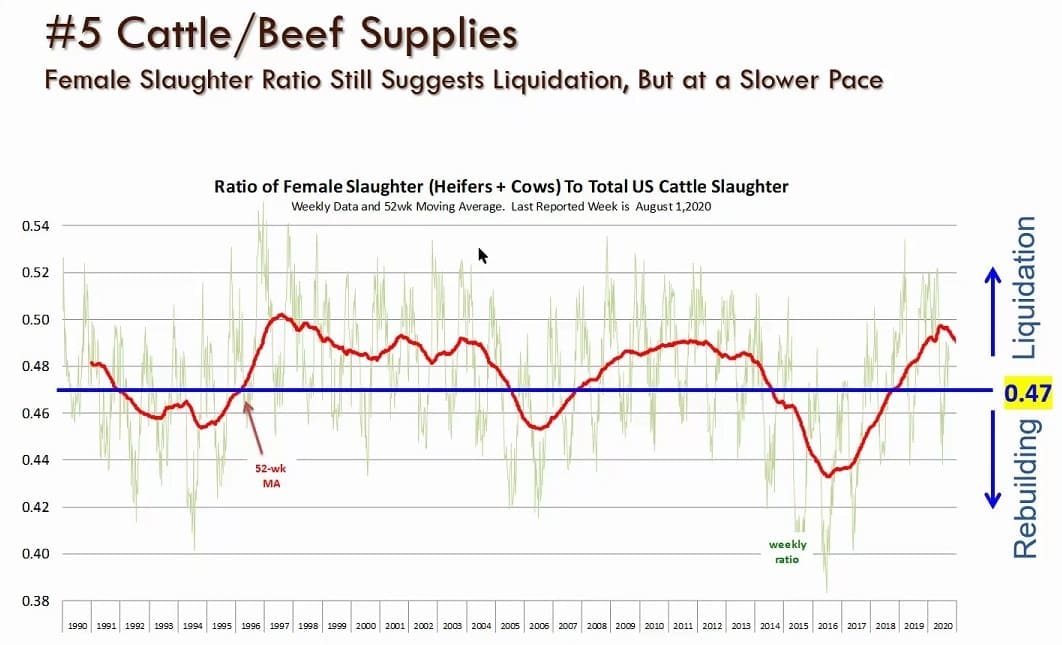

Using the slide below, Mr Steiner suggested that when females exceed 47pc of overall slaughter numbers (blue line), it represents herd liquidation. The ratio had been more than 47pc for the past couple of years, but was now in decline, with cow slaughter now 1.1pc less than a year ago, however drought in western states could impact the trend.

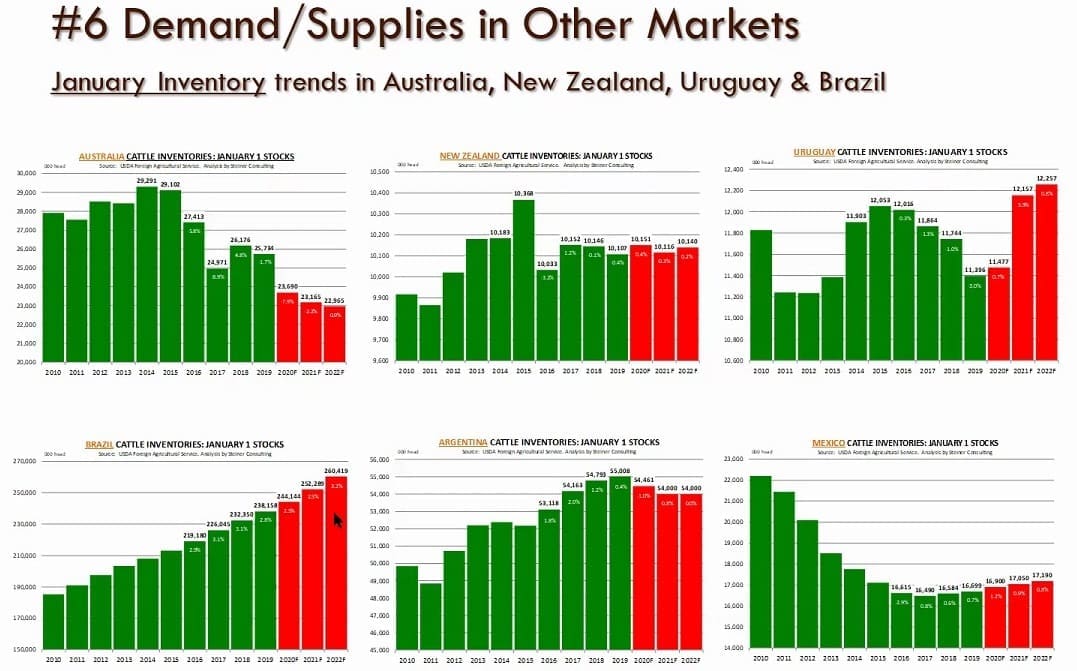

Mr Steiner used the graph below to compare herd inventories and trends among other major beef producing nations.

Australia was sharply down due to drought out to 2020, NZ was flat, Uruguay had grown a little, Brazil had shown non-stop growth, Argentina had come off a little, due to some liquidation because of money problems; and Mexico was growing a little.

“In general, the beef herd population worldwide is growing a little, while both the US and Australia are trending down,” he said.

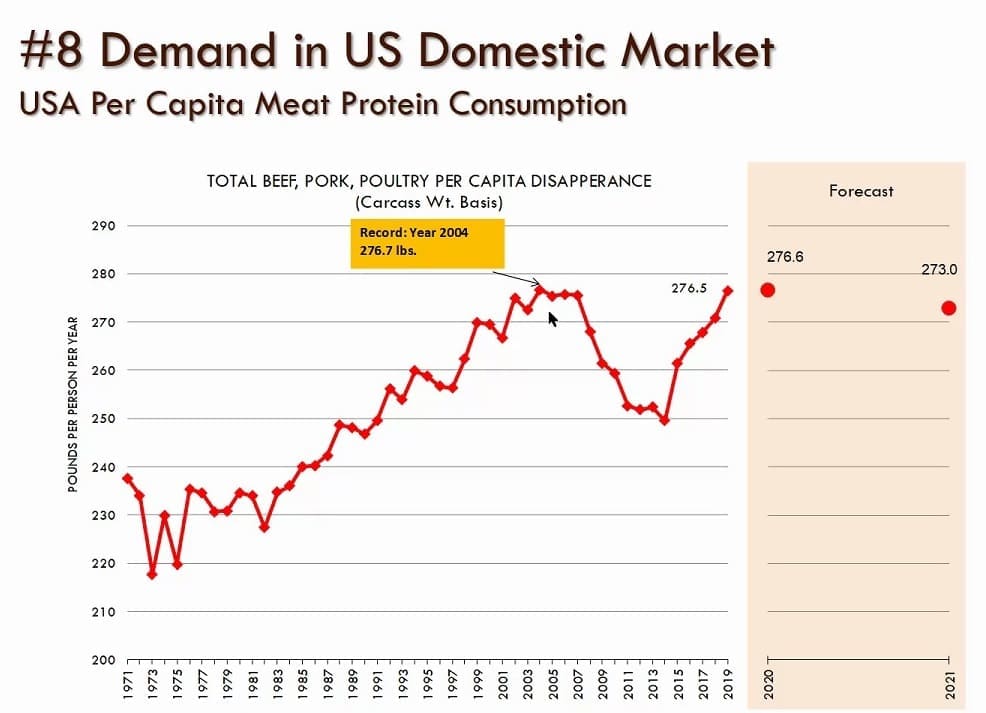

US demand for meat

Per capita US consumption of meat (beef, pork, poultry) hit an all-time record back in 2004 of 276.7 pounds, carcase weight basis (almost 126kg), but as the graph below shows, volume dropped away for some years after that, before recovering to near record levels last year, as production had grown.

“We will be at a similar number for 2020. But we think what the industry is running into now in the US is a ‘share of stomach issue’ between the various proteins,” Mr Steiner told the webinar.

“At some point, consumers are just ‘full’, and when that happens, they do not have a big incentive to go and buy additional meat products.

“Show up to a gathering of ten people around a table with nine generous plates of food, and you really find out who wants to eat. But come to the same event with 11 plates, and the fact the ten people have already had a full meal means the price of the eleventh plate could get pretty cheap,” he said.

“One of the problems with this is the inelasticity of demand for meat protein. Produce one percent less, or more, and price can give a response much bigger than 1pc. When you are trying to ‘force feed’ somebody who is already full, price has a negative effect, and the US chicken industry certainly has seen this, this year, with very low broiler prices, as they have been trying to force-feed the American public with more meat than they have room for,” he said.

“This is kind of where US meat production is at present. In order to get prices up, production is going to have to be pulled back. If that happens next year, per capita consumption may go down, and prices may come back a little.”

Mr Steiner said the same effect (reduced availability of meat for domestic consumers) could be achieved through increased US meat exports next year.

Price forecasts

Mr Steiner anticipates live steer prices in the US will rise a little next year, but suggested a better indicator was comparisons with the 2019 (pre-COVID) year, which suggested a fall next year.

For 90CL grinding beef, which rose dramatically during the second quarter this year due to panic buying, he anticipates prices next year to average 225c/lb, down a little on this year’s average of 234c/lb. However 90s prices next year were likely to be up a touch on 2019 prices.

“While cattle prices next year may be a little lower than 2019, we think the price of 90CL is going to be up,” he said.

Premium for Australian imported

The forecast spread next between US domestic 90s at 226c/lb and Australian imported 90s at about US233c/lb represented a premium of US7c/lb for Australian imports, Mr Steiner said, but the spread could vary from month to month.

Because of lower beef production in Australia and recovery in the Australian economy, there would be a premium next year on Australian meat in the US over domestic US 90s.

And there would be a premium for Australian over Brazilian or Argentinean imported grinding meat, during the same time period, he suggested.

During questiontime, a stakeholder asked about the outlook for increased South American exports into the US next year.

Mr Steiner said South American exporters were trying to ‘go wherever the money is,’ and the money currently was in the US market.

“We understand there continues to be some issues around getting enough product into the US because of testing requirements. Both Argentina and Brazil are coming back after periods of time where the US government would not allow them in, so they are doing more testing of product to make sure they are in compliance. That is slowing up some of the trade.”

Issues with quota also continued to put South American exporters at a slight disadvantage, he said.

Great article/analysis. Very pleased that only 20% of Australian beef exports go to China.