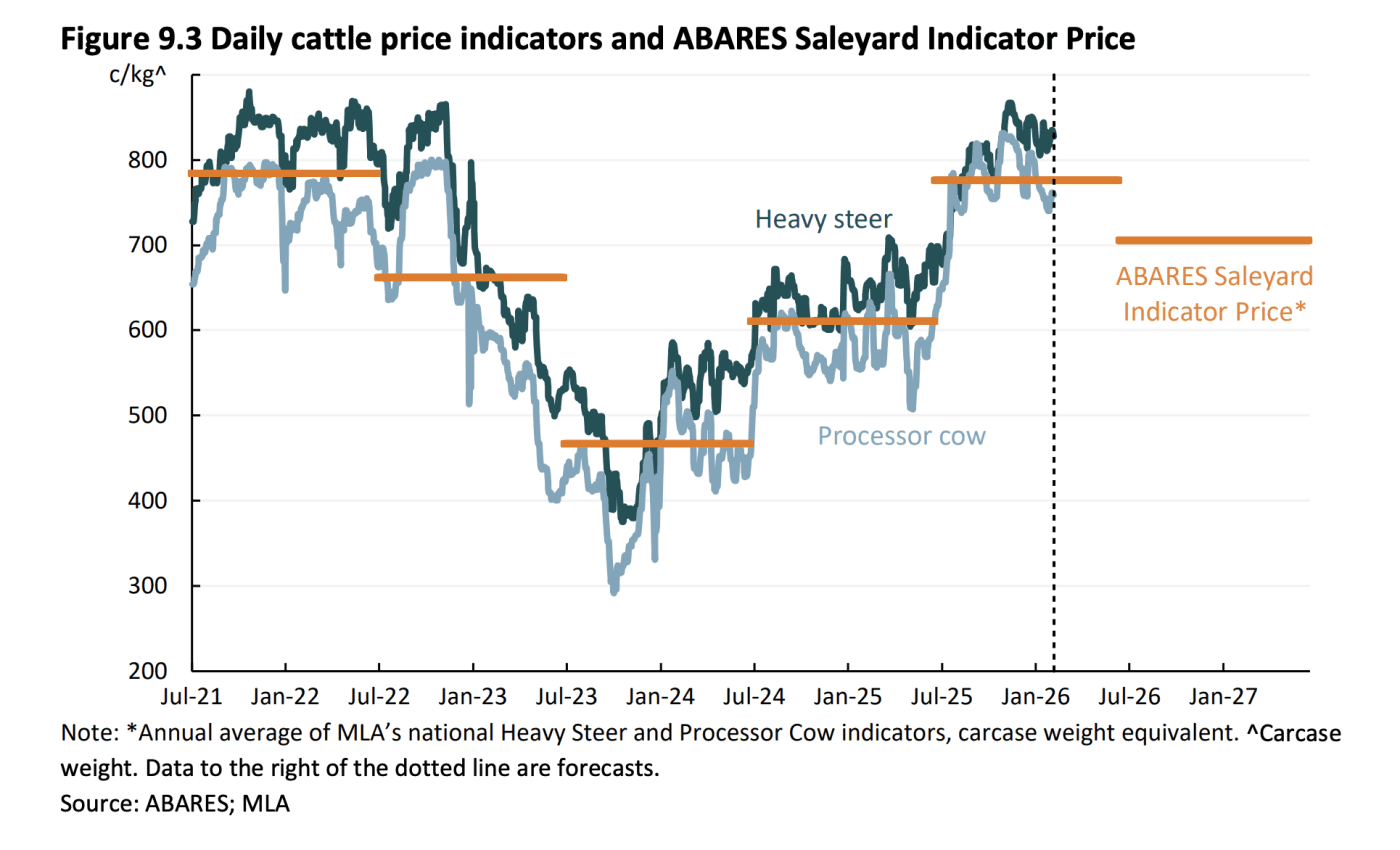

Australian saleyard cattle prices are forecast to fall by nine percent next financial year, but still remain slightly above the 10-year price average in real terms.

At its annual Outlook conference in Canberra today, the Federal Government’s chief commodity forecaster provided its assessment on how factors such as China’s new safeguard tariffs, production giant Brazil’s flexing export muscle and a below average climate forecast will shape market conditions for Australian producers in the next 12 months.

ABARES’ Saleyard Indicator Price is set to average 775c/kg this financial year (2025-26), before declining to 705c/kg in 2026-27.

Tight beef supply in the US remains the dominant influence on the forecast, ABARES says.

However, it also forecasts China’s WTO global beef safeguard measure to limit Australian beef exports and trigger lower prices in other global markets in the first half of 2026-27, in turn reducing Australian processor margins and demand for cattle.

However, it also forecasts China’s WTO global beef safeguard measure to limit Australian beef exports and trigger lower prices in other global markets in the first half of 2026-27, in turn reducing Australian processor margins and demand for cattle.

Continued dry conditions and an average to below average climate outlook is forecast to keep turn-off elevated, especially cows, in large areas of Southern Australia, and reduce competition among processors to secure cattle for slaughter, putting downward pressure on prices.

However, good pasture growth in large areas of Queensland is forecast to increase producer confidence to profitably convert lighter cattle into finished stock.

Beef production is forecast to fall by 6 percent to 2.6 million tonnes, as lower cattle slaughter outweighs a slightly higher average carcase weight.

ABARES believes the Australian beef herd will reduce by 3 percent this financial year (2025-26) due to elevated turn-off and a high female slaughter rate in Victoria and New South Wales in particular, which will lead to total lower calving in 2026-27.

However, this is forecast to be partially offset by favourable climate conditions in most regions of Queensland, which sees the herd forecast for 2026-7 remain relatively steady, down 1 percent to 27 million head.

Annual beef export volumes are forecast to fall by 8pc in 2026-27 to 1.5 million tonnes.

Australia is forecast to export 82 percent of its total beef production in the current financial year (2025–26).

Live exports of beef feeder, breeder and slaughter cattle are forecast to increase by 1 percent in 2026-27 to 784,000 head, aided by a build up of cattle across northern Australia in recent years.

Average prices for live feeder/slaughter cattle exports are forecast to decline 3pc to $1180 per head, driven by lower competition amongst Indonesian feedlots to secure stock with greater availability of Australian cattle and continued weakness in the Indonesia Rupiah tightening margins.

Global beef demand forecast

Globally, demand for beef is forecast to rise in 2026-27, driven by population growth and rising protein consumption in middle income and developing economies.

United States: Demand for Australian beef, particularly lean trimmings to complement US domestic production, is forecast to remain robust in 2026-27, but with increasing competition from Brazil and Argentina.

China: Beef imports to decline due to the introduction of the 55 percent out of tariff safeguard quota applied to all major suppliers. Australia’s quota allocation is 205,000 tonnes, significantly lower than the 318,000t exported last year. When the quota fills, Chinese importers are forecast to increase orders from other suppliers such as New Zealand, Argentina and Uruguay, which has larger quota relative to historical shipments compared to Australia and Brazil.

Japan and Korea: Demand for beef imports is forecast to increase in 2026-27 due to lower global beef export prices. Reduced market access into China to create a surplus of global beef exports, resulting in lower prices into other markets.

Global beef supply forecast

World beef supply in 2026-27 is forecast to fall slightly.

Brazil: Now the world’s largest beef producer, having overtaken the US in 2025, production is forecast to moderate in 2026-27 following elevated cattle turnoff in recent years. Beef production and exports have increased substantially in recent years reflecting productivity gains underpinned by increased feedlot utilisation, which has allowed producers to slaughter cattle at a younger age and maintain price competitiveness to Australia. Brazilian exports to China are forecast to fall due to the safeguard tariff-rate quota of 1.1 million tonnes, leading to greater shipments to the US, southeast Asia and the Middle East. Brazil has recently secured market access gains to Indonesia and Vietnam, but a greater risk to Australia’s beef export competitiveness over the medium term would be if Brazil gains access to Japan or Korea – access is currently restricted due to disease concerns, but in 2025 the Brazilian Government announced it had received certification from the World Organisation for Animal Health as a country free of foot-and-mouth disease.

US: With herd at a more than 70 year low, continued dry conditions across many areas of the Midwest and high prices are expected to keep turnoff elevated.

Argentina and Uruguay: Exports forecast to increase in 2026-27 due to increased import demand from China, with allocated quota much higher than 2025 export levels from both countries.

To view full ABARES 2026 ag commodity outlook click here.