AUSTRALIAN cattle prices could double over the next two years, but specialised segments like Wagyu feeders could take up to two years longer, delegates at the Australian Wagyu Association annual conference in Cairns were told this week.

Simon Quilty addresses this week’s AWA conference

Analyst Simon Quilty told an audience of 650 delegates from across Australia, New Zealand and other countries that global supply and demand circumstances, and especially those in the United States, would work strongly in the Australian beef industry’s favour in coming years.

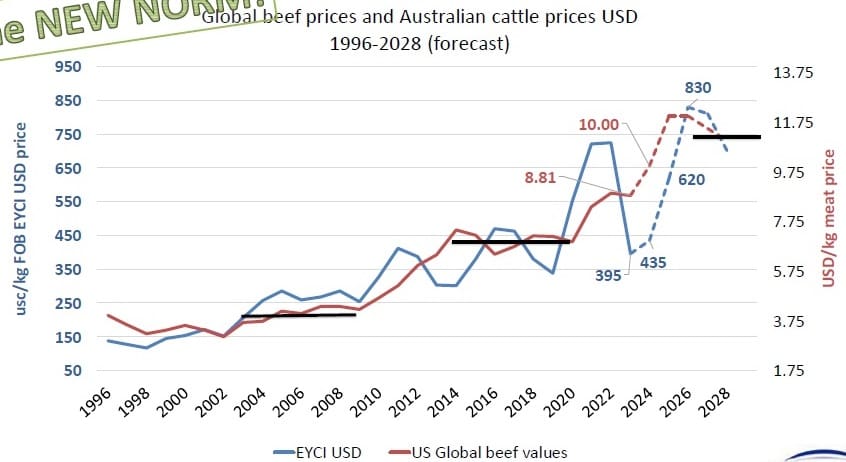

He said globally, prices today for cattle (and beef) were dramatically under-valued.

In what could only be termed an enthusiastically bullish address, he said the industry had been sitting in a ‘holding pattern’, as prices stated to improve this year.

“Just recently, we’ve had a nice rebound in cattle prices, but there’s a lot more work to be done yet,” he said.

“It’ next year, in 2025, that things really start to gather momentum, as tight beef supply meets global demand, that starts to pick up dramatically.”

He termed this phase “The new norm.”

“It’s in 2026 and 2027 where I believe we will see a sustained increase and value of livestock until at least 2030, if not later,” he said.

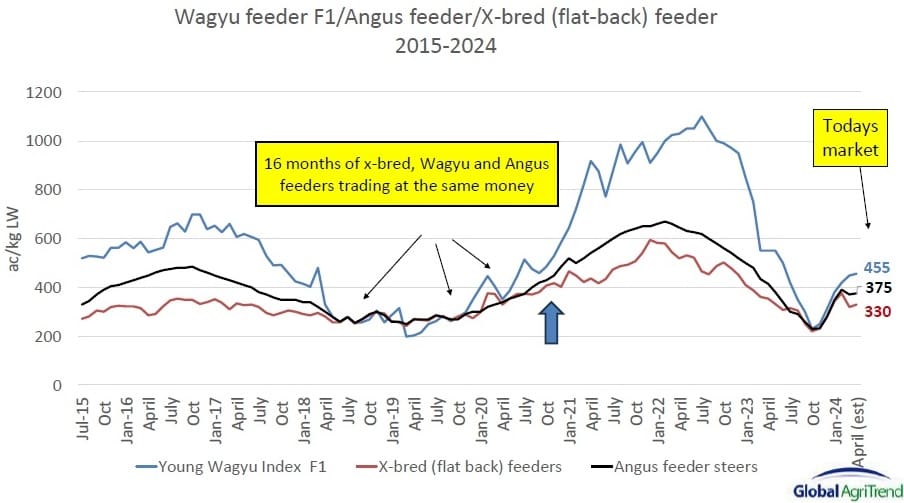

In the graph published here, plotting Wagyu, Angus and Queensland flatback feeder steers, the period 2015-17, pries were good. Then there was the enormous collapse in which Wagyu actually traded below the value of flatbacks for a period. Then the market picked itself back up, and in 2022, a remarkable peak was seen at close to $11/kg liveweight, for F1 feeders, and Angus close to $7/kg.

“It begs the question: Where are we heading today?” Mr Quilty asked.

“Why is it that we have rebounded off the bottom today, whereas last time there was a collapse, prices wallowed for almost 18 months?”

“This time, we spent only around four weeks at the bottom of the market.”

Mr Quilty said one of the key reasons was that the Australian herd genetics today were so much better.

“Genetics improved out of sight – that’s made us less vulnerable to certain parts of the market,” he said.

“Secondly, there was less panic. This time, people held their nerve. Wagyu numbers on feed fell from an estimate around 230,000 head down to only 208,000 head, whereas last time there was a collapse, Wagyu numbers on feed fell down to just 165,000 head, as people exited the market, and swamped the market.”

“Also today, we have a much stronger international customer base – more diverse, and with deeper pockets.”

“As an industry, the Wagyu sector has become more diversified, more mature, and its ability to manage these downturns is critical – and the industry has shown it can do it,” he said.

Looking at the nominal value of cattle, every ten years or so, prices reached a new peak, Mr Quilty said.

“We saw this in the 1970s, followed by a stable period. Go forward another ten years, and there’s another stable period. By the end of next year, we’ll be at the end of the next upwards cycle.”

“After this, I believe from late 2025 to around 2032, stability will be back in the market – at much higher prices than today.”

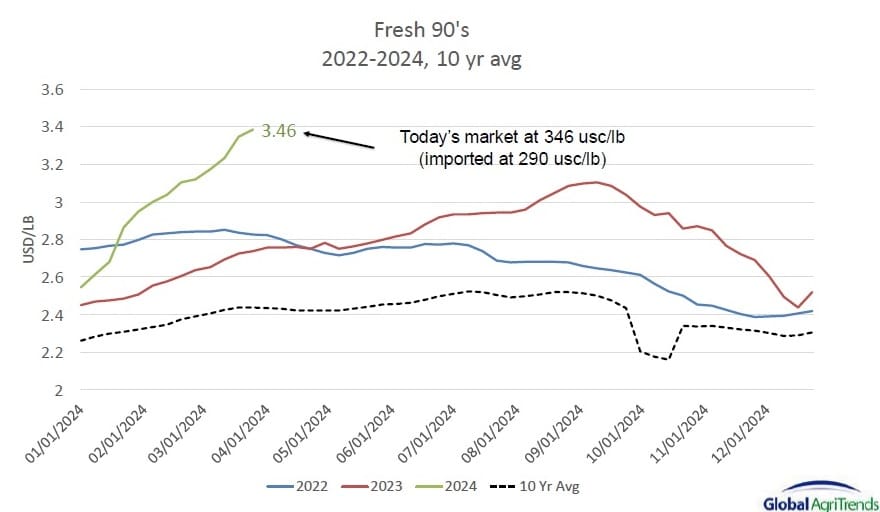

He said grinding meat prices in the US had this week hit new record levels, with US fresh 90CL beef hitting US346c/lb.

“But when grinding meat prices lift like this, it takes everything else with it – the round cuts, tenderloins, you name it. That’s because if it doesn’t sell on its own, it gets directed into the grinder. Trimmings at these prices will lift the value of carcases, and cattle in general, and global meat prices.”

And he stressed that these record US prices are being seen at the start of the Northern Hemisphere summer demand season – not at the end. The expectation among some is that the US market for fresh 90s may go to US380c/lb this year.

“In 2026, and 2027, I’m of the opinion we’ll see fresh US 90s at US410c/lb, which will lift global beef prices significantly,” Mr Quilty said.

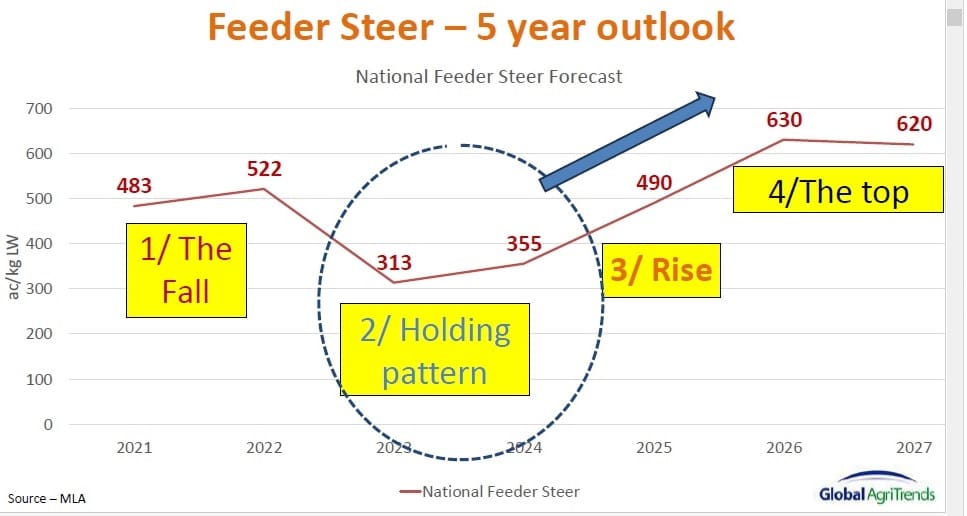

For the next five years, he forecasts that flatback Australian feeder steers will average 520c/kg. That follows a ‘slight move sideways’ this year (355c/kg), followed by a 470c average next year, and 630c/kg the year after that.

“Welcome to the new norm,” Mr Quilty said.

Weather a factor

Weather would obviously play a part in future trends, he said, and weather experts that his company, Global Agritrends relies on suggest a breakdown of El Nino in Australia, moving into another La Nina phase in June, producing a wet period for the back end of this year.

“With that, rain is starting to fall in North America, as we speak,” he said, “and the US is such an important part of the global equation when it comes to markets.

“But as Australia enters a forecast wet period later this year, the US is expected to go dry again. It has been a troublesome three and a half years for North America – rain finally comes, but the belief is, it will be only short-lived.”

Turning to Australia’s supply situation, Mr Quilty said last year, the number of states in herd liquidation (female slaughter above 47pc) gradually increased as last year progressed, with the fourth quarter showing Victoria, NSW, South Australia and Western Australia all reducing herds due to weather pressure.

Last quarter, ended 31 March, those states got worst, while the ‘rebuild’ states of Queensland and Tasmania got better.

“It’s quite unusual that states are moving in opposite directions, but its all about whether rain is falling,” he said.

The net effect was that NSW and Victoria have had an unusually high liquidation period, and in Queensland, a fairly strong rebuild.

“The tightness in cattle supply will be critical as a part of that elevation in cattle prices over the next five years,” he said. “The more we liquidate now and over the past year, the higher prices will potentially go.”

Mr Quilty suggested the national herd (currently around 25.6 million) is it comes through this liquidation process, and if the forecast for weather into next year proves reliable, it will grow to around 26.4m next year, and 27.7m the year after that.

“We’re pointing to heifer retention, because that’s what’s required to get the rebuild going. That tightness in the market also lends itself to higher prices.”

In terms of rates of slaughter, his forecast is for a national kill this year around 6.8 million head, but to fall dramatically next year to 5.8 million, as the southern rebuild gets going in earnest, and 5.7m in 2026.

He said the rise in cattle numbers on feed to record numbers last year was not driven by global demand, but weather.

“Last year was truly a challenging year for meat sales,” he said. “But I see numbers of cattle on feed going to new record highs over the next few months, which will also be price-supportive for the feedlot sector.”

Tough year for beef exporters

While Australia’s beef export volume lifted last year because of the dry conditions and liquidation in some areas, prices were lower in most markets. In the US, for example, our imported beef prices fell 21pc on the previous year, down 11pc in Japan, 18pc in Korea and China, and globally, down 18pc.

Mr Quilty said it was important for producers to understand how challenging 2023 was for Australian meat exporters – but he also thinks the worst is behind us.

“Interestingly, the US is key to all this. If we look at Korea, Australia has picked up 18pc in terms of volume, as US supply has fallen – even though it all occurred at lower prices. In China, Australian export volumes are up 30pc year-on-year, while US volume is down 20pc.

“That’s because when it comes to export production, globally, Australia and the US compete with each other in all these key markets. In Japan, Australia and the US ‘own’ 90pc of the imported beef market.

“So if America drops in volume, as they are, we step up to fill the void.”

Globally, Australia has stepped up producing in other markets an additional 49pc of volume, while the US is down 6pc.

“When it comes to the tightness of supply in the US and the liquidation, we are truly the one nation in the world that can step-up and fill the void,” he said.

Wagyu price trends suggest green shoots

Green shoots were starting to appear, globally, Mr Quilty said.

Presenting the slide below showing global Wagyu prices since 2020, using Japanese data, it showed Japan ships around 8500t of Wagyu around the world each year.

“It’s a really good windsock to show us what’s coming. In comparison, Australia exports about 70,000t of Wagyu beef each year. Since 2021, prices for Japanese Wagyu to all markets around the world fell 35pc, with the bottom of the market around October last year. That was much the same time as when the Australian Wagyu market bottomed, also.

“So it wasn’t just the Australian Wagyu industry feeling the pain – Japan felt it just as much, and they provided a window as to why that happened.”

China remained a challenging market for all imported beef – with the local freezers full of product – mostly South American in origin.

“Consumer confidence in that market has fallen off a cliff, and trade has been challenging. Freezers in Japan were also full with beef inventory, but thankfully in the last six months those stocks had started to fall.”

US green shoots

So while international markets are improving, progress is gradual.

In the US, since around May last year, as seen in the graph above, domestic beef production volume has started to fall.

“They simply don’t have the volume as their herd rebuild phase starts,” Mr Quilty said.

In the above graph, Australian grassfed is displayed in green, which represents one of the Wagyu industry’s competitors in the China marketplace.

“The consumer in China is looking for quality, and value for money – and that is what the grassfed trend is all about. They are looking for the taste of a beef item with quality, but at the right price.

“That is going to be the challenge for Wagyu over the next five years – being ‘affordable’.”

US hold the key to price recovery

Despite the developments in other export markets, the key to recovery and improvement in prices for Australian beef over the next three to seven years lay with the United States, where the national beef herd last year hit a 73-year low, Mr Quilty said.

“As a result of that, we are just starting to see price signals in the market. The live cattle Futures market in the US is predicting that prices will increase by 9pc by April next year.

“To me, this is truly under-valued. They have prices going to US$194/cwt, whereas in my mind, they have to be talking at least $210-230/cwt.

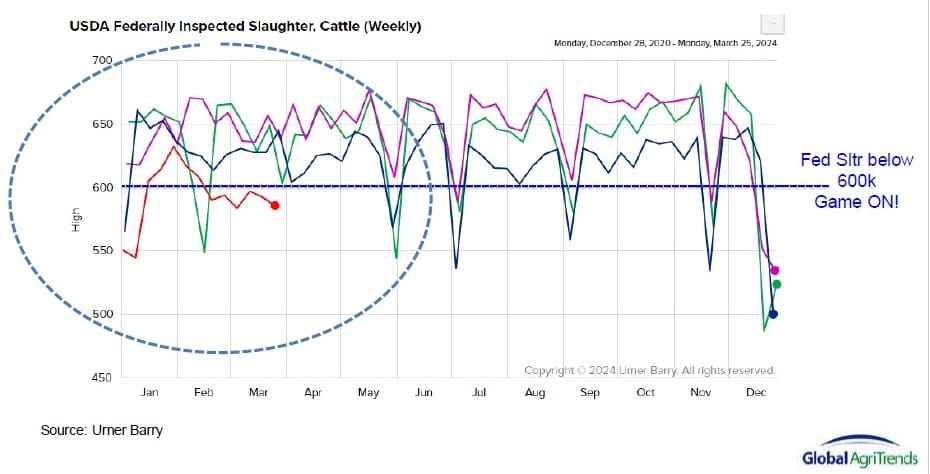

The key that drove this was weekly US production, and the US female kill for the past 28 months had sat at 51pc, he said.

“The normal rate for breakeven is 48pc, so female slaughter has been way above what it should have for more than two years, reducing the US herd to the point where now meat supply is holding up dramatically.

The key today for US kills is 600,000 head per week, and in this graph, it can be seen that it has just gone below that critical number. Once US slaughter starts to drift below 600,000, automatically prices start to improve, and that follows into all other markets, Mr Quilty said.

The expectation is that the US will see a 9.5pc fall in beef production between last year and what’s expected in 2025. That would translate into a 26pc fall in US global exports.

“As a result of this, the Japanese and Korean markets which Australia shares with the US, will see a big decline in US supply, meaning Australia is the one to step up. It points to strong demand for Australian beef in North Asia, simply due to the lack of US supply,” Mr Quilty said.

But even though there are strong headwinds in the US in terms of high cost of living, latest consumption figures show that beef continues to be the main player in the US protein space, with US$36 billion worth of retail sales last year. The next largest contributor, poultry, accounted for $18 billion.

Aussie Wagyu position in the US

In the graph below, it is evident that USDA Prime Grade beef (red line), the highest quality category, is almost a safety net for Australian Wagyu, Mr Quilty said.

Whenever Australian BMS 4-5 Wagyu (green line – one of the Wagyu sector’s lowest grades, but still a step above USDA Prime) falls slightly below it, it does not take long for Australian Wagyu beef to be back above it again.

“It is out-competing the best of USDA Prime, in terms of price.”

(graph US prime graph)

US sophisticated market

(graph)

Mr Quilty said in his opinion, the US was “truly a sophisticated beef market.”

“All the different grades of marbling score are truly recognised and appreciated, whether it be 8-9s, 6-7s, or 3-5s,” he said.

“You can see when the market was at its peak in August 2022, just how much of a significant premium the quality end of the market did for Australian beef in the US.

“As an industry, our challenge is to see the same level of sophistication and education in other regions – it does not exist in Asia, for example. In Asia, it’s all about brand.”

“To me, where we want to go globally is in true recognition of marbling scores, by segment.”

(slide – US prime)

Looking forward through 2024, Mr Quilty pointed to the extraordinary relationship with US Prime, versus the nine year average.

“It looks to me like we are going to get a peak in the US market around June, before moving sideways, with a fairly flat line later this year, due to lack of domestic supply.

“For Australian Wagyu beef into the US, USDA Prime is the safety net – as Prime lifts, so too does the market for Australian Wagyu.

“I think the signs are encouraging, and I think we will see them sooner, rather than later in the North American market.”

Wagyu trim critical

As prices for beef go higher and consumers are really challenged, Wagyu trimmings (used for burgers and other manufacturing beef items) was critical in the overall mix to deliver profitability in the Wagyu sector, Mr Quilty said.

“We saw in the US over the past year, due to the high cost of living, that beef trim pricing was up 4.2pc, as demand rose due to people trading down from steak cuts.

“The key is, we want the consumer who elects to eat a burger over a steak, on price, that they choose a Wagyu burger – that the eating experience doesn’t disappear, or drift into another species.”

Looking at Wagyu 65CL trimmings prices over the past three years, China had been the key (China plotted in red).

“China became the common denominator – if you couldn’t sell it anywhere else, you go to China. What happened in the period in the graph when the two came into line, was that McDonald’s Australia ran a Wagyu promotion which sucked-up every carton of 65CL trim, and even drove grassfed 65s higher.”