SHAREHOLDERS have savaged the Australian Agricultural Co’s stock value in the wake of Wednesday’s announcements to the market about operational reviews of the company’s poorly-performed Livingstone Beef processing plant near Darwin and some branded beef programs.

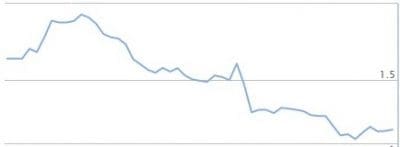

The share price suffered an 8pc discount immediately after the announcement, falling from $1.22 to as low as $1.08, before recovering later in the day to $1.12 at close of trading on Wednesday.

Yesterday the share price recovered a cent, closing at $1.13 – still close to its lowest point since hitting $1.62 back in November.

AA Co’s weekly average price trend over the past 12 months (Note: graph does not capture the slide in value seen over the past two days)

AA Co has experienced a dramatic fall in its share price over the past year, from $1.92 last June, arousing recent speculation over a potential buy-out by largest shareholder, UK billionaire Joe Lewis’s Tavistock Investments, which Bloomberg suggests has gradually crept up to a 42.48pc stake in the world’s largest beef business.

The mood evident during Wednesday’s analysts’ telephone briefing suggested onlookers were taken by surprise by the financial disclosures – particularly those surrounding the performance of the Livingstone Beef asset, which up to now has been obscured by being reported within the company’s broader northern beef operations.

Livingstone Beef processing facility, near Darwin

The newest and most modern beef processing plant in Australia, the Livingstone asset cost AA Co $100 million to build only three years ago, amid great fanfare. Local reports in Darwin suggest the plant has been operating for only two days a week in recent times.

Any reservations about the project’s chances of success, including comments from experienced processing industry sources published by Beef Central when the project was first floated, were quickly hosed-down by AA Co management and the board, as ‘lacking vision.’

In disclosures covered in greater detail in this article we published on Wednesday, AA Co forecast a likely loss before tax of $30-$40 million for its trading year to March 31 – a massive turnaround from profit of $133 million a year earlier.

The company announced a strategic review of its Livingstone Beef processing operations, “to assess all available options and determine the optimal path to deliver shareholder value from the facility.”

AA Co reported significant losses related to the Livingstone Beef business in the range of $60-$65 million, reflecting an impairment charge against the carrying value of the business and ‘onerous contract provisions’ including the provision of gas supply to the plant.

Wednesday’s briefing was told the company’s performance in the second half of last financial year, ended March 31, had been affected by external challenges including increased competitive dynamics in certain markets, a higher Australian dollar, higher input prices and an elevated cattle price environment for the Livingstone Beef plant, resulting in higher cattle procurement costs.

In a significant departure from previous briefings where individual performance of the Livingstone Beef business was shrouded within broader company results, AA Co has now chosen to directly report on the asset’s performance. It said Livingstone was expected to contribute an FY18 operating pre-tax loss of $18-22 million for the full year. That compared with an FY17 operating loss of $12.5 million – the first time that figure has been publicly disclosed, in Beef Central’s understanding.

In order to provide greater transparency to the market, AA Co said it intends to include ‘segment disclosure’ for Livingstone Beef in its full FY18 audited results, due for release on May 23.

AA Co provided a written response after Wednesday’s briefing on whether the Livingstone facility could now be put on the market:

“The review will provide an understanding of the broad range of potential alternatives and at this stage we have not ruled anything out. We will provide a detailed update on the review at the time of our 2018 financial year results, to be announced on May 23. While this strategic review is underway, management will continue to focus on the controllable aspects of the production process, including further improving the operational efficiency of the plant.”

Speculation has circulated since Wednesday’s disclosures, and consequent share price drop, that Joe Lewis’s Tavistock may soon mount a takeover, to privatise AA Co.

Last year, AA Co embarked on an overhaul of its executive team, purportedly on the back of greater control being exerted by Tavistock.

Chief executive Jason Strong left suddenly in August, preceded by the company’s chief financial officer, senior marketing personnel and other key staff. The CEO’s temporary replacement, Scott Prebble, is leaving the company for other employment, AA Co told the market recently.

At times, brutal questions

At times brutal questions levelled by analysts and investors during Wednesday’s phone briefing focused on share price performance, profitability, strategic direction and the prospect of asset sales.

One analyst from Bennelong Asset Management asked whether the company would consider selling its properties and returning the cash to shareholders, given that the company’s share price was trading at such a discount.

“That’s not within the scope of the review,” CEO Hugh Killen said. “Our properties form part of our unique supply chain, and the cattle are obviously key to what we do, in being a branded beef business. We are focussing on improving performance in the business, and that is the core part of the review. We believe the decisions we are making here today, in terms of how we approach our supply chains, will increase our underlying profitability, and therefore the share price.”

“What happens if you don’t succeed?” the Bennelong analyst asked.

“We will succeed,” Mr Killen said.

AA Co’s Dane Fitzgibbon would not speculate on an assessment by another analyst that the company’s full net profit after tax, based on the full balance sheet, might reach $60 million this year, saying this would be disclosed in May.

“Today’s information is a pre-release, using ranges from the unaudited numbers,” he said. “We tried to deliver what we could reasonably provide, early, to give the market transparency, but there is a layer of detail that will follow in May,” he said.

“The Livingstone review will come back with a fulsome report at the release of the full-year results in May.”

Another analyst said over the past ten years, there had been brief ‘glimmers’ of returns on assets approaching 10pc, and he wanted to know what the board’s target for ROA was, and how it proposed to get there.

“What we’re doing, as part of the review, is focusing on the performance of the business, and getting to the position where the business is performing up to its opportunity. But we have not set a target at this point for return on capital,” Mr Killen said.

“You’re a listed company on the stock exchange,” the analyst said. “You have peers around you that have set 10-15pc return on asset targets.”

“We assess investments on a case-by-case basis, for their contribution towards executing our strategy,” Mr Killen said. “But we’re not disclosing benchmarks for the entire company.”

AA Co’s cost structure also came under close investor scrutiny.

“Looking at the cost base of some of AA Co’s unlisted peers (other large privately held pastoral companies), are you happy with the cost base – the multiple layers between senior management and the people on the ground?” an analyst asked.

“There is a strong view, which will come into focus as part of the review process, that we can reduce some of our cost base,” Mr Killen said. “The decision around the 1824 brand program (100-day grainfed beef – now to revert to cattle sales instead of retained ownership through the supply chain) was the first part of reducing that cost base that exists in our business, and we’d expect to be able to eliminate further costs going forward,” he said.

“The strategic blunders have just been one-after-another, with chopping and changing, and a laundry list of excuses accompanying each set of sub-standard results”

Aaron Edwards from Alta Investment Management, asked when the AA Co board, and in particular the chairman, would be held accountable for the “extremely sub-standard performance” of the business over an extended period.

“Mr McGeochie has been chairman for the past seven years, and we have been a shareholder for most of that, unfortunately. The strategic blunders have just been one-after-another, with chopping and changing, and a laundry list of excuses accompanying each set of sub-standard results,” Mr Edwards said.

He sympathised with Mr Killen, having been CEO for only a short time, but he said it had been ‘going on’ for a long time, and obviously most of the high-level initiatives (ie Livingstone Beef) had been signed-off on, and presumably extensively investigated, by the board. His question was, “when is there going to be some accountability at that level?”

Mr Killen said he would take the comments on board, and feed them back through to the chairman.

“I would say that while the current AA Co management team is new, it is not asking for a free-ride out of that. But we are focussed on improving the business going forward, and it is important that everybody understands that we are making decisive decisions around the business, giving higher levels of disclosure, and are committed to improving the business performance, going forward.”

Chairman Don McGeochie did not participate in Wednesday’s investor briefing.

- No date has yet been set for this year’s annual general meeting, but AA Co said it was likely to be in Brisbane in July.

I concur with comments made by Alan Schmidt.

A classic example of a company that has lost focus on what they do best.

Seeking vertical integration via “killing” and “branding” has come at an enormous cost. Both killing and branding require considerable experience in each discipline, of which AACo had none.

It’s hard enough to run an abattoir anywhere and history shows running one in the NT has been fraught with danger and starting from scratch could only have been a high risk venture.

A very top heavy head office only exacerbates the problem and winning awards doesn’t create profits.

Imagine if the Livingstone capital had invested in a couple more major breeding operations as an alternative. Might have even made a profit in one of best bull runs the industry has seen for many years!

One feels for the institutions who have finally become interested in Australian agriculture but have unfortunately backed the wrong horse.

Rob Backus, Peter Vincent and Ian McKenzie are correct regards their comments on the current Chairman. He should do the honourable thing and resign.

The AA co began to lose it’s focus when Chris Walker saw them coming and sold them his Wagyu herd (good luck to Chris!).

The Company used to be probably the lowest cost producer of live beef protein in the world at the Farm gate. Any analyst in any primary or commodity sector would say that that is a reasonable place to start. AA co forgot about this and began searching for ‘added value’ without understanding that they were blindly walking into totally different businesses.

It requires a very able MD with a depth of experience in the sector and an experienced team of senior mangers that are empowered. This has not been the case for over a quarter of century in this particular business.

Time the company got back to the knitting!

We have to be realistic.Don McGauchie has stepped from one disaster to another in terms of his lack of skills as Chairman of business that he must now know are outside of his skills. When the chips are down he seems to be always missing and letting others stand alone in explaining what the Company is trying to structure towards a successful integrated business plan and a business that has unlimited potential. Please Mr McGauchie step aside and let someone with talent have a go!!.

The numbers didn’t add up when the first sod was turned to build the Livingstone plant and they don’t now. AA engaged in a very expensive exercise attempting to remodel itself as a producer of meals controlling the chain from go to whoa and now ponders returning to its historical core business. The oft-quoted “critical mass” does not mean there’s safety in numbers in any commercial sphere and particularly so when producing animal protein whilst relying on stable production and market environments. Don McGauchie was out of his depth at Telstra when acting as Trujillo’s “yes” man to drive a wedge between the company and it’s largest shareholder. He’s not the person to steer the board of AACo.

Aaron Edwards’ insight and comments are spot on. Time for changes at the top.

Market Analysts, and all stakeholder need to understand, if not remembered, that a pastoral grazing zone beef producer is similar to a factory, in there is a ‘production-line’ of Beef (on-the-hoof): yet totally unlike a widget factory. The risks are huge, and cumulative, in this type of business: especially the variability of seasons over a 10-year period, and the volatility of farm-gate prices for a similar period in the Pastoral grazing zone commodity space can be huge.

This current price of $1.18, is roughly the same price the company has been fluctuating around for a long time: look back and see …

Whatever the reason for the waxing and waning of the share-price, my considered Valuation opinion still remains sitting at an underlying intrinsic value of around $1.65 per share (fully diluted) … with Livingstone Plant yet to come into its own …

Funds Managers who are complaining obviously do not understand the nature of risk in this space, and the need for quiet and patient capital … it’s all about Great Expectations on their behalf.

Beef as part of Food and Fibre, is a Long Game … so buy well (as in now), and sit back for a long ride. It’s like mustering: a quiet ride out, a bit of a trot-along, a bit of cantering as necessary, an occasional gallop, and then swallowing dust behind the mob on the steady walk on the way home … ?? Everyone needs a cold shower, a cup of tea and a Bex, and a good lie-down …