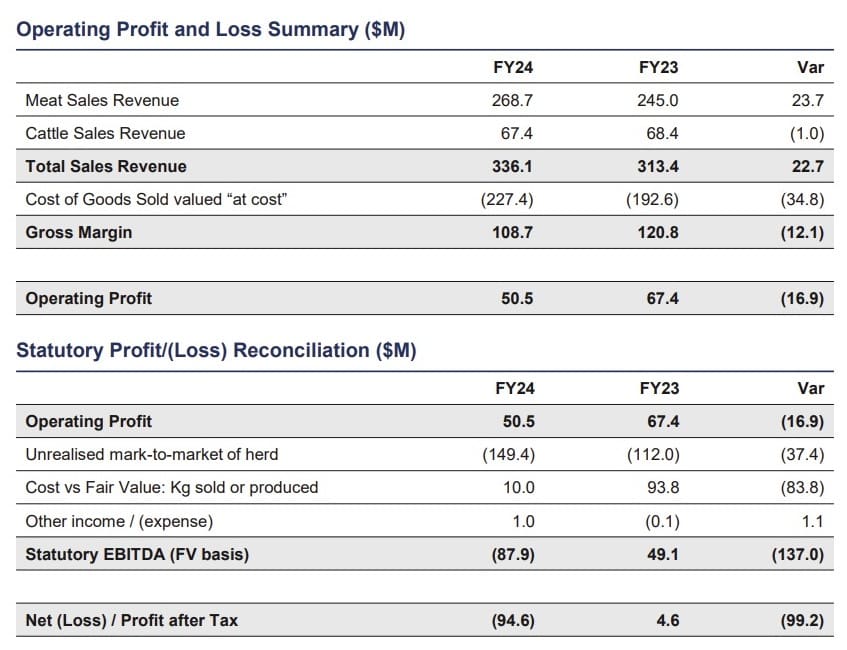

THE Australian Agricultural Co has delivered a $50.5 million operating profit for its full financial year ended 31 March.

While the result was 25 percent down on the prior year, it was still AA Co’s second largest operating profit, and the second consecutive result above $50 million, demonstrating the business’s ability to combat global market conditions.

However significant herd valuation downgrades impacted the statutory net profit after tax result, which showed a $94.9m loss, down almost $100m on the previous year.

However significant herd valuation downgrades impacted the statutory net profit after tax result, which showed a $94.9m loss, down almost $100m on the previous year.

Managing director David Harris told an investor and analyst briefing this morning that the company believed it was a strong result, in the context of difficult global conditions throughout the year, including increased global beef supply, and reduced live cattle market prices during 2023.

“While these difficult conditions had some impact on these results, the company’s brand strategy and unique distribution network helped deliver as strong outcome,” he said.

AA Co’s beef brands were still commanding price premiums in markets around the world, and considerable work was undertaken to capture more value through its beef programs.

“Our ability to increase sales volumes, while achieving price resilience shows the strength of our supply chain,” Mr Harris said.

In other key financial and performance metrics announced this morning for 2023-24:

- Operating cash flow of $9.3m was down $6.7m on the previous year, as the company “continues to align with strategic priorities,” including expansion at Goonoo feedlot discussed in more detail below.

- Sales revenue of $336m was up 7pc on the previous year, the third consecutive year of revenue growth

- The company spent $36.5m on business investments (principally, Goonoo, solar installations and upgraded plant and equipment), up $16m on the previous year

- The beef herd grew by 5pc to 455,000 head during the year

- The herd valuation was adjusted downwards by $149m to $611.3m, in line with general cattle price trends

- Net asset value was down marginally on the prior year to $1.517 billion, including a $78m increase in the value of pastoral properties and improvements value (more than offset by the decline in livestock value)

- Wagyu branded beef sales averaged A$19.85, up 10pc on the previous year.

Click on image for a larger view

As the company flagged earlier in interim results in November, Australian cattle prices hit four-year lows in the last financial year ended 31 March, which was the primary influence behind the weaker statutory NPAT performance.

The herd valuation was carried out at the end of the company’s financial year (March), Beef Central was told, and no doubt results would have looked worse if it was conducted at the end of last year.

“However the reduced cattle valuation is primarily realised by limited live cattle sales,” Mr Harris told analysts.

“While the significant reduction in cattle values impacts our balance sheet and statutory performance, it has a more limited impact on our operating performance, which remains positive,” Mr Harris said.

Growth in Wagyu sales, resurrection of 1824 brand

The company reported a 10pc increase in Wagyu meat sales revenue last year, some of which could be attributed to new product trials including Wagyu bacon, pre-formed burger patties and grassfed products introduced during the financial year.

![]() The resurrection of the company’s pioneering 1824 beef brand launched around 2003 was also announced during this morning’s briefing, although it will be a very different product than what was originally sold under the brand.

The resurrection of the company’s pioneering 1824 beef brand launched around 2003 was also announced during this morning’s briefing, although it will be a very different product than what was originally sold under the brand.

In its first iteration, 1824 was 130-days grainfed, supplied from the company’s composite flatback breeding program, with typical marbling scores of 1-2. It was successfully sold into middle to upper end food service across North America, Asia and Australia.

The new 1824 – marking the company’s two hundredth anniversary being celebrated this year – will be Wagyu product from the lower end of the marbling score range, typically marbling scores up to 4-5. The brand will sit below the company’s flagship Fullblood and crossbred Wagyu brand like Westholme and Wylarah, using new distribution channels targeting restaurants, steakhouses and pubs and clubs with a premium, yet more affordable Wagyu product, Beef Central was told.

Under the company’s sustainability initiative, the company reported $4.3 million worth of Australian Carbon Credit Unit accruals, from on-property carbon projects.

Goonoo project

The recently completed expansion project at AA Co’s Goonoo feedlot in Central Queensland has expanded both feedlot and cattle backgrounding capacity, this morning’s briefing was told.

The $12 million expenditure occupied a considerable chunk of last financial year’s $36m cap ex budget, along with projects like solar panel installation and plant and equipment upgrades. The company made no land purchases during the year to March 31.

Annual branded beef volume production through the Goonoo facility will rise 12pc, including an additional 5000 head yard capacity, but equally importantly, significantly larger backgrounding capacity.

Revenue performance a key achievement

Company chief financial officer Glen Steedman told the briefing that revenue performance ($336m, +7pc) was a key achievement for the year.

“We were able to leverage our existing supply chain, responding in an agile manner to the challenging price dynamics to increase supply and combat negative price impacts,” he said.

“The resilience of AA Co’s branded beef products limits the impact of price pressure, with volumes up 24pc, and average price down 11pc,” he said.

“The resilience of AA Co’s branded beef products limits the impact of price pressure, with volumes up 24pc, and average price down 11pc,” he said.

Cattle sales were subject to live cattle markets, which reached four-year lows during the year, having a direct impact on AA Co’s cattle sales margins.

“Again, we were able to increase volumes by 49pc, to combat these market conditions,” Mr Steedman said.

The significant decline in cattle market prices last year impacted AA Co’s statutory results, he said.

The reduction in statutory EBITDA of $137m was driven by unrealised mark-to-market loss on the herd value, as well as a lower value on animals sold or processed, in line with broader market conditions. Effectively, the herd valuation impact would only be realised, should those cattle be sold.

“Our strategy of selling premium beef into global markets helped us limit the impact on our results from reductions in live cattle prices,” he said. “This is why we focus primarily on operating performance, not statutory.”

Operating environment

AA Co’s David Harris

David Harris said most of the varying market dynamics highlighted above were outside the company’s control.

“Global meat sales conditions remain uncertain for the current trading year, however a key feature has been how we have purposefully positioned ourselves to both manage the current conditions as well as preparing for the opportunities that we anticipate will come,” he said.

“Managing the things within our control will keep the company in a strong and agile position. Consecutive favourable seasonal conditions across AA Co properties are contributing to strong pasture growth and increased productivity.

“Combined with a full year of benefit from the Goonoo expansion (described above), we anticipate healthier cattle and increased supply of our premium Wagyu,” he said.

“Analysts predict global over-supply of beef will ease in late FY25 (by January-March next year) which if realised should alleviate pricing pressures across our Wagyu boxed beef and live cattle sales,” Mr Harris said.

Questions

Unusually, there was only a solitary question from analysts at the end of the briefing.

David Harris was asked what impact the emerging US herd rebuilding phase and cattle shortage would have on AA Co Wagyu beef sales.

He said most analysts were predicting that general beef prices would improve in the back half of 2025.

“We are seeing that start in the commoditised lean beef area of production. The premium end of Australian beef will probably see a little of a lag on what the analysts think. We see it as a lot of opportunity, but probably the back half of next year for us,” he said.

- AA Co’s share price fell to $1.36 during early trading this morning, down 5c on yesterday.