Richard Koch, Elders

Elders analyst Richard Koch provides this regional cattle market summary following an Elders regional livestock managers’ hook-up each Monday…

THE sharp rise in fuel costs will have far reaching implications for Australian livestock markets through increased freight costs (for both livestock & beef) and the broader impact on beef demand and grain prices.

Freight costs have risen around 20 percent since the conflict started late last month. How long they will remain elevated remains uncertain but at this stage likely at least until after Easter.

The implications for cattle markets are likely to be:

- Southern processors may not be able to pay as much for northern cattle to freight south this autumn/winter, increasing the seasonal north/south cattle price divergence over the next few months (refer to comments in yesterday’s weekly kill report)

- Downward pressure on restocker demand with the cost of freighting cattle to get them home more expensive than a fortnight ago

- An increase in the cost of exporting beef, increasing imported beef costs

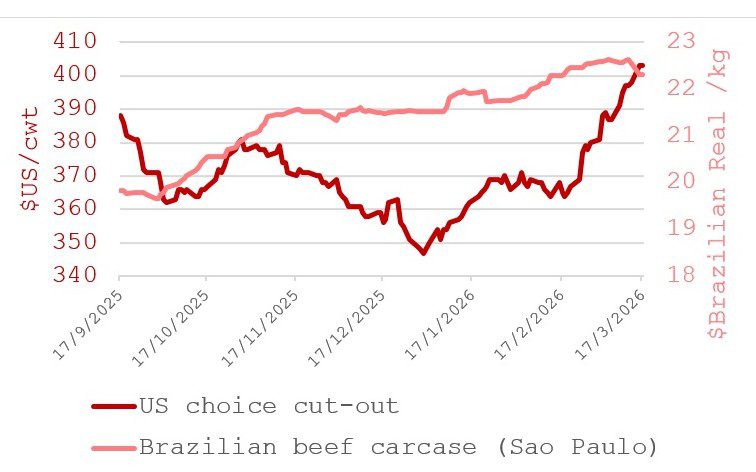

- Increasing consumer expenditure on fuel and reducing the amount of money that consumers have to spend on beef. So far there are no signs of a pullback in global beef prices with US wholesale prices moving significantly higher in recent weeks (see chart).

- Higher grain prices. Wheat is up from $345/t to $365/t Downs over the past fortnight with further rises likely. This will tighten feedlot margins and reduce demand for feeder steers.

This chart shows US and Brazilian wholesale beef prices. Source:LSEG workstation

Cattle markets show no sign of fuel impact – yet

So far, the impact of higher fuel costs has not been felt in local cattle or international beef markets, which continued to hum along fully firm this week, with local markets influenced by limited supplies out of large parts of Queensland.

Our Longreach agent reports that excellent early rain has brought on a better variety of grasses than last year with pastures having more bulk. It’s very wet north of Muttaburra and it may take three to four months to get stock out from high rainfall northern areas.

There won’t be a rush to sell cattle given the feed situation with dry cows and feeders held over from last year the first to go when it dries out to generate some cash flow. Some local producers are likely to hold cattle to utilise the feed and sell them at heavier weights around August-September. There are still some areas south of Longreach needing more rain and some runoff to fill on farm storages.

Further south and west in Central Queensland, cattle are stuck in paddocks putting on weight with sales at Gracemere cancelled last week and Charters Towers not selling over the past fortnight.

There is green feed “up to the third and fourth barb” in CQ cattle country, one local agent said. Most of Queensland has now had rain, if not too much, with only a patch from Goondiwindi out to Cunnamulla and north to St George needing more rain.

The Darling Downs feeder market is hard to quote at present, but firming towards 500-520c/kg (all liveweight, unless stated), with quotes hard to get as yards work through cattle contracted earlier at 500-510c/kg Downs.

The fat job is still holding around 450c/kg lw bullocks and $3.80/kg cows. Little restocker cattle are making plenty of money $5.50/kg with heifers still lagging, but catching up gradually.

Some cattle are just starting to move again in CQ, although there are a lot of internal roads not operational, making it difficult to shift cattle from yards to the bitumen. Weather pending, there will be a run of slaughter or heavy feeder cattle when the first frosts hit and prior to the end of June, which may pressure prices and test processor and feedlot capacity.

NSW

The NSW market is completely different and very dry compared to the rest of the east coast with massive yardings at all northern NSW sale centres again this week and plenty of store stock available. The strength of the market is contributing to the heavy, early turnoff.

Weaner calf sales at Carcoar this week will provide a firm test of the market, with a quality yarding of 8000 predominantly Angus blue ribbon calves at an Elders-only sale this Friday.

There are likely to be more black calves sold this week in NSW than for a long while. At Carcoar most of the yarding will be around 300kg and judging by the offering at Yass weaner sale last week where most were 220-280kg, heavier weight weaners are the exception rather than the norm.

Restockers chasing weight should be shopping at Carcoar this Friday.

Tasmania

In Tasmania last week, the north of the state received another 10-30mm of rain which was very timely for the first of the Elders feature annual weaner sales at Powranna, where 2800 mostly Angus calves were sold in challenging conditions.

The top end 440-450kg sold from $2300/head or 480-500c/kg, with mediums around 550c/kg and lighter weights around 200kg 580-620c. Heifers sold from 440-450c/kg with lighter types 460-470c.

In the Tasmanian fat cattle market, which is primarily grassfed program yearlings and dairy/cull cows, prices for program yearlings were 860-870c/kg dressed.

Local prices are going to be affected by higher fuel costs with a large proportion of Tasmanian cattle having to be shipped across the straight and slaughtered on the mainland.

Slaughter cows were a little softer this week with weight of numbers as the annual cull ramps up as winter approaches with values sitting at 750-800c/kg dw equivalent in the yards.

Processor margins are tightening, however, the desire to retain overseas staff that the industry has invested in, to train and house after COVID, should keep processing rates strong, helping and to underpin slaughter cattle demand.

South Australia

It was also raining in south-eastern South Australia earlier this week where the season is up and going. Stubbles are amazing due to bumper crops with plenty of seed blown out the back of the header, crops have self-sown.

With diesel and chemical costs rising, putting stock on is a good way to keep costs down and retain some sub soil moisture for winter, finding stock will be the main issue.

More rain in SA pastoral areas this week has set our clients up for the year and they are looking to rebuild numbers. Elders Broken Hill bought three loads of cattle out of Tamworth last week, but getting a reasonable freight quote was difficult with diesel up about $1/litre. The freight situation is going to make restocking less enticing than it was a few weeks ago.

Elsewhere in SA, across the Eyre Peninsula there is some stock coming off lentil stubbles that got knocked around by the rain. There is also plenty of restocker interest from the inside country, with discussions taking place with agents in WA about moving stock across the Nullarbor.

Western Australia

In contrast to the east coast, West Australian prices have been stable for a couple of months with local feeder steers 420-500c/kg and heifers 350-430c.

Prices are likely to firm into autumn/winter with supply of quality cattle in southern WA starting to drop off with graziers likely to get rewarded on their third and fourth drafts. Cows have strengthened 690-715c/kg dw at the works and 320-350c/kg lw in the yards.

Kimberley/Pilbara

As WA cattle numbers taper off in the south, attention turns to northern cattle supply with Kimberley stations holding livestock supply tenders in the next week where they invite southern processors to submit bids.

While Kimberley supplies should be excellent, the season in other WA pastoral regions has almost been non-existent with conditions poor from the Pilbara to the Gascoyne and down through the mid-west out towards Kalgoorlie with some areas not having rain going on 2-3 years.

There is going to be a lot of light store type cattle coming out of these areas at 150-250kg steers and heifers and light cows which will be the lowest priced cattle $per head in Australia by some distance.

HAVE YOUR SAY