Click to enlarge

A PROLONGED herd recovery from a 30 year low in Australian cattle numbers will underpin a sustained period of historically high cattle prices, Government forecaster ABARES predicts in its annual commodity outlook reports released today.

ABARES herd and production estimates released today. Click to enlarge

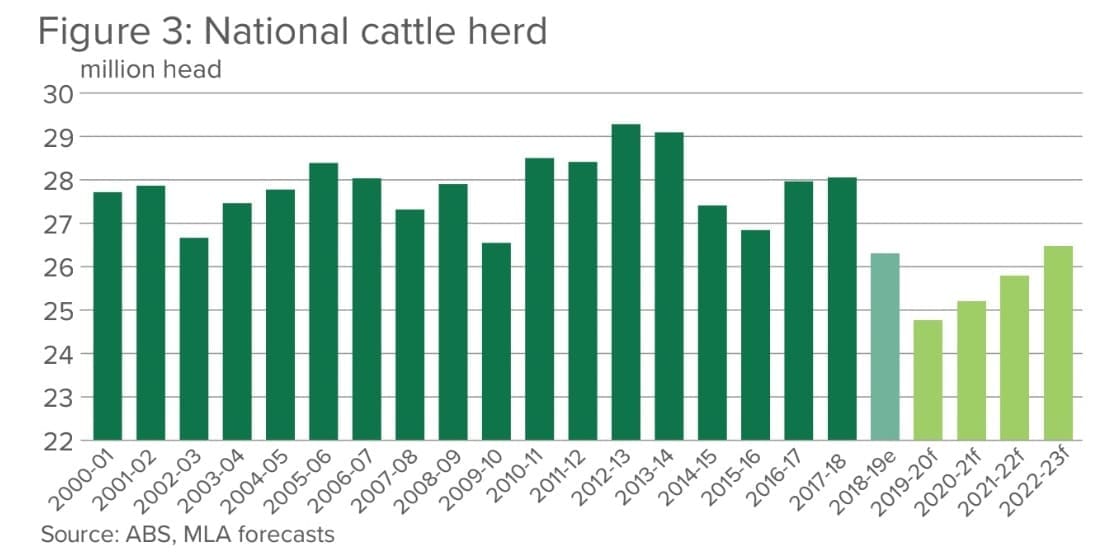

ABARES estimates Australia’s total cattle herd will stand at 23.5 million head at June 2020.

That total comprises 21.1 million beef cattle and 2.4 million dairy cattle.

ABARES’ herd size estimate is 1.2 million head less than the 24.7 million head figure put forward by Meat & Livestock Australia in its 2020 projections last month.

Why the large discrepancy between the ABARES and MLA estimates?

A major reason appears to be a change that was made by the Australian Bureau of Statistics to the way it gathers data for its yearly surveys.

MLA’s herd estimates released in February.

Traditionally ABS’ annual agricultural survey has included farms with an estimated value of agricultural operations (EVAO) of $5000 or more.

However, in 2017, the ABS raised the bar to only include enterprises with an estimated value of operations of $40,000 or more.

The change was reportedly made to save resources but meant many small-scale cattle enterprises around the country were no longer counted.

MLA told Beef Central it uses the most recent ABS Agricultural survey figures as a basis but then incorporates its own projection models to calculate all cattle, not just those from an enterprise with an EVAO of $40,000 or greater, to provide an accurate herd estimate.

ABARES also draws upon the ABS figures as a basis for its estimate but uses a different methodology to MLA to arrive at a final herd figure.

A spokesperson said ABARES uses herd demographic modelling combined with its assessments of price signals for producers and the prospects for pasture growth over the forecast periods to arrive at its herd estimate.

The result is a difference in official estimates of the size of the national cattle herd of more than one million cattle, or around 5 percent.

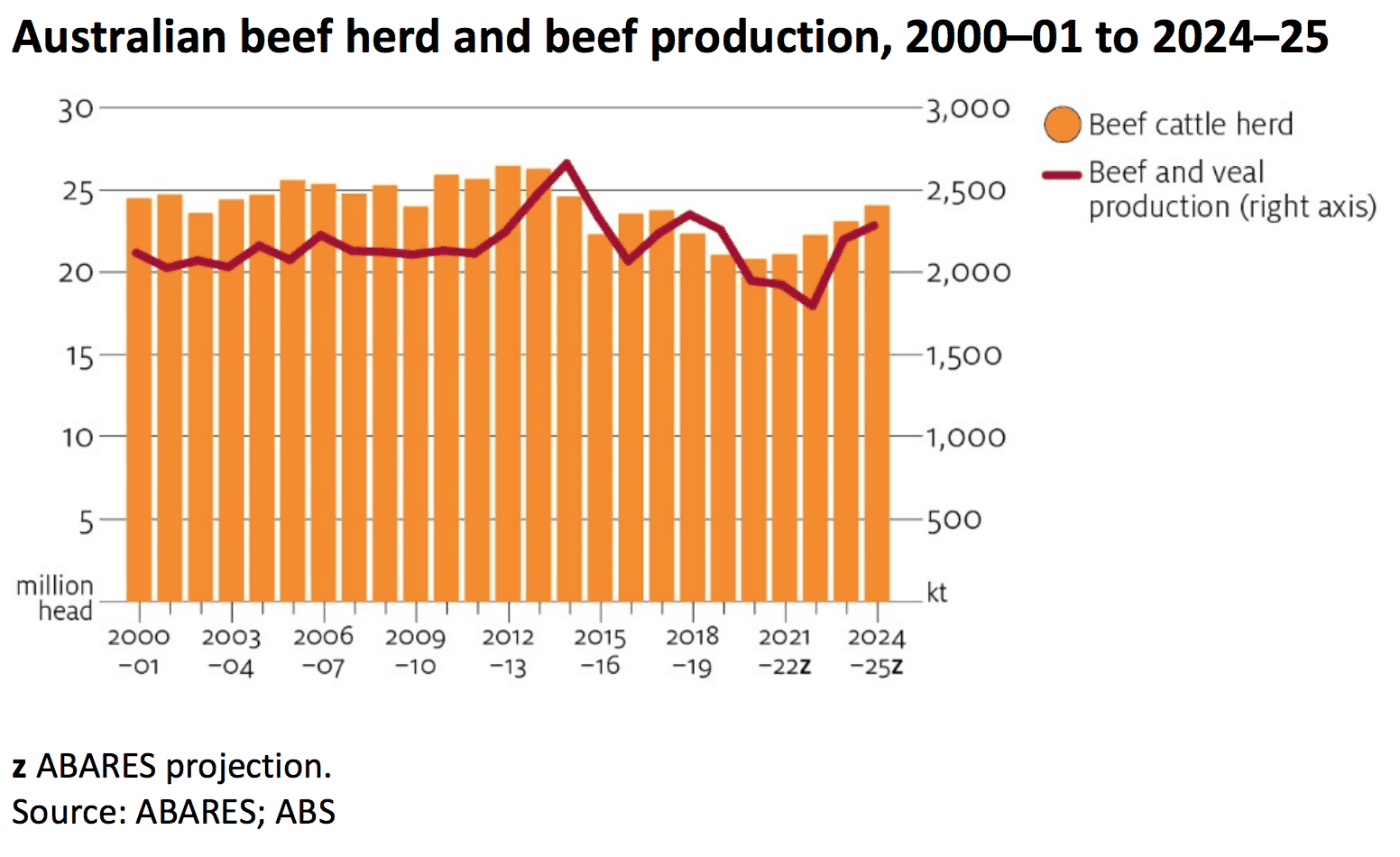

In today’s outlook report ABARES says it assumes a scenario that reflects climatic conditions similar to those experienced over the last 20 years to predict that the herd will increase by 4 percent per year on average to grow to 26.5 million head (24.1 million beef cattle, 2.4 million dairy cattle) in 2024-25.

Australian beef production is projected to reach 2.3 million tonnes in the same year, which is a level similar to the long-term average.

Key components of ABARES’ forecast for cattle and beef include:

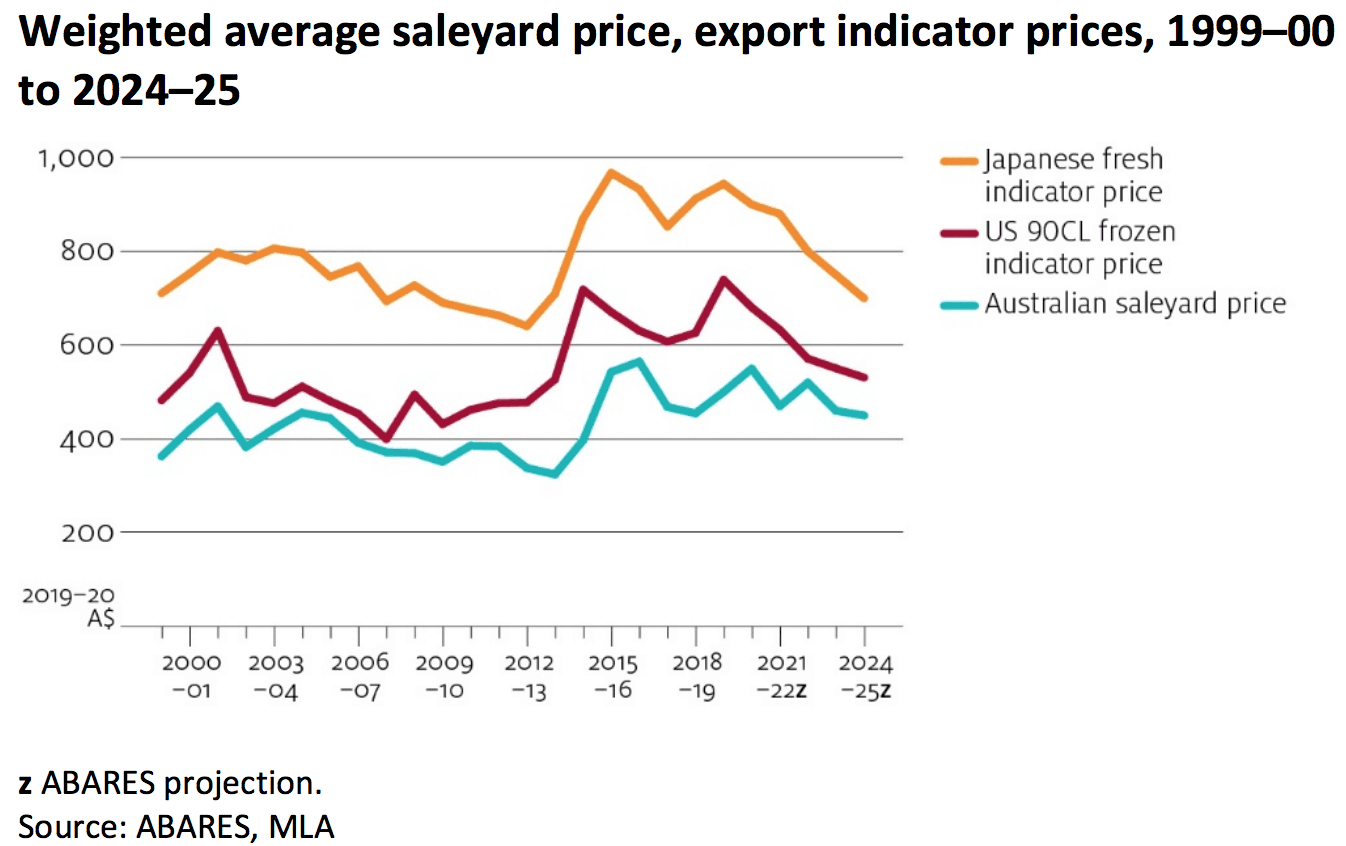

- The Australian weighted average saleyard price of cattle to rise by 7 percent to 538c/kg carcase weight in 2020-21.

- Average slaughter weights to increase as a result of improved pasture availability and a lower proportion of females in total slaughter

- Increased slaughter weights will only partially compensate for reduced turn-off, with beef production to decrease to 2.0 million tonnes in 2020–21.

- Australian beef exports to fall to $7.6 billion (0.9 million tonnes) in 2020–21, down from $9.8 billion in 2019–20 (1.2 million tonnes shipped weight).

- Export volumes to recover gradually, reaching 1.1 million tonnes in 2024–25.

- Australia will continue to experience increasing competition in key export markets.

- In particular the US will be more competitive in Japan and China following recent trade deals

- Australia beef in China will also face increasing competition from South American countries. In September 2019 China approved 25 new Brazilian facilities, bringing the total to 89.

- In October, China also approved 14 more Irish beef plants, bringing the total to 21.

- Impact of coronavirus (COVID-19) – Demand from restaurants is expected to remain weak as consumers avoid public dining until virus can be controlled, but beef sales in supermarkets are expected to remain relatively unaffected.

- Reaching pre-African Swine Fever levels of pork production to remain elusive meaning Chinese demand for beef will remain elevated in the short term.

- Demand in China to gradually ease to more normal levels towards the end of the outlook period, as a result of pork and poultry production increases either in China or in other major producing countries.

To view the full ABARES cattle and beef outlook 2020 report click here