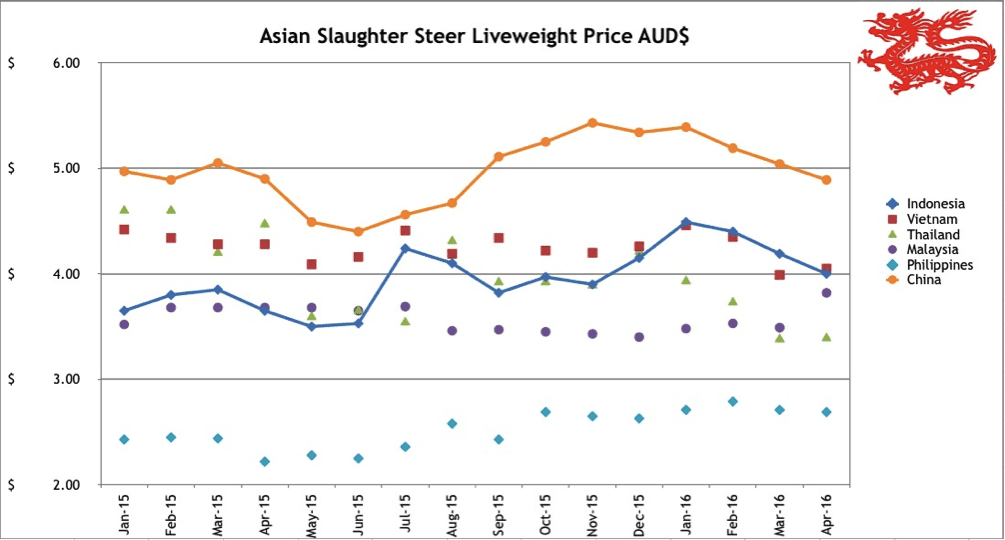

Indonesia: Slaughter Steers AUD $4.00/kg live weight (Rp10,000 = $1AUD)

There are plenty of very high cost fat cattle around at the moment and demand is soft so prices have eased a little since last month with even a bit of discounting for volume sales in the Jakarta area down to as low as Rp38,000 per kg live weight. This is not across the board so I am using Rp40,000 for the report figure this month. The Medan price remains at around Rp44,000 as supplies there are still very tight. The only good news for importers at the moment is that the price of Australian feeders is coming off quickly at up to 30 cents per kg less than January imports.

T2 Import permits of 250,000 head were allocated at the beginning of the month but the actual documentation is held up with bureaucratic problems so once again the exporters will be caught with ships ready to sail and no physical permit document in hand to allow the ship to depart. This absurd situation literally costs the industry millions of dollars as expensive vessels are anchored in the harbour waiting for permission to load. These additional costs are eventually passed onto the customer in one way or another so if the Indonesian government is interested in keeping prices low for its consumers it would be a good idea to fix this very, very simple problem.

There has been a lot of press recently about the Indonesian government fast tracking the importation of Indian buffalo beef to ensure that supplies are available in the market in time for the traditional high demand period of Ramadan and Lebaran. As the fasting month of Ramadan begins on 6th June with the major feasting and holiday week of Lebaran beginning on the 6th of July there doesn’t appear to be much time remaining to get this done. Given that the printing and delivery of an already agreed import permit can take nearly 2 weeks I don’t think that the chances of changing legislation and providing all the documentation etc for imports of large volumes of Indian product in less than 2 months is very likely. Not to mention the process of physical importation and distribution! And we haven’t seen the local farmers voicing their opposition yet so it seems to me that there is still a long way to go for this particular initiative.

The price fixing conviction saga for importers continues and could possibly drag on for a further four years as this is how long it might take for the appeals process to complete its journey through the Supreme Court.

Correction: In my opinion piece published in Beef Central a few weeks ago (Indonesian Beef Cartel Guilty of price fixing & market manipulation: Please Explain?) I stated that the importers were obliged to pay their fines up front in order to run their appeals. I am happy to correct this error (but not as happy as importers I expect), as the official advice is that importers don’t need to pay the fines until the appeals process has been concluded.

Some additional information has come to hand in the last week or so that further confuses the situation in respect to these convictions :-

- Some State Owned Enterprises are live cattle importers, feedlotters and trading companies but they were not subject to the KPPU court action even though they operate in the same market as the commercial importers. It would be an interesting comparison to follow their inventories and selling prices during the investigation period to see if and how they differed from those found guilty of market manipulation.

- I am advised that at least one “Importer” who has a new import license but has not actually imported any Australian cattle yet was also convicted and fined with the rest! This company does however operate a feedlot processing local cattle. Does this mean the local cattle traders will also be investigated or is this only the case if they intend to import Australian cattle?

Of the 32 commercial importers that were charged, all 32 were found guilty. While I know little about the details of the case, one thing I can confirm through interaction with many of these companies over many years is that most of them are fierce competitors who rarely communicate or cooperate in any way. It was therefore astonishing to me to discover that every single one of these aggressive commercial enemies have been found guilty of getting together with the rest and agreeing to fix the price. And at a time when supply was low and the price was already high and rising.

Another puzzling aspect of this government crackdown is the extremely doubtful effect that it is likely to have on the real consumer price. Of the 32 importers who fatten Australian feeder cattle, I do not know of any who actually retail their end product. In the vast majority of cases, fat cattle are sold “farm gate” to local butchers or traders. These butchers/traders then arrange for the slaughter of the cattle. During this process the cattle and their parts may be sold one or more times before the actual beef reaches the wet market. In a small number of cases, the wet market beef table is owned by the butcher but in most cases the wet market trader is just a retailer and/or wholesaler buying from the butcher. So in the course of every day, live cattle are sent from 32 importers to about 200+ (ESCAS approved) abattoirs with subsequent delivery of meat products to several thousand wet market stalls. At each point of sale along this processing and distribution end of the supply chain, the transaction is made on purely commercial grounds i.e. supply and demand. In the event that the importer should sell his cattle at less than the commercial rate to comply with the wishes of the government then this “low” price will simply be taken as a gift by the numerous traders operating between the feedlot loading ramp and the wet market seller. The wet market is without doubt a classic case of pure supply and demand as there are no regulations on them to sell at a price decided by the government or anyone else. There are probably tens of thousands of small operators selling product in the middle of the night and early morning all over Indonesia ensuring that it would be physically impossible for the government to have any hope of regulating their prices. The end result of course is that this wet market price will be a true reflection of the real demand and supply situation and if the supply is low the price will be high and vice versa. Therefore making rules for Importer pricing is completely futile if the aim is to maintain the retail price of beef within the government’s desired price parameters.

Last month I presented a Bloomberg graph showing how Indonesia’s GDP growth was continuing at a relatively steady 5% level. As further support for the reality of these figures see below a photo I took a few days ago of several construction sites immediately behind the MLA office in the western suburbs of Jakarta. When this office first opened about 6 years ago, their building was new and the area behind was a cow paddock. Today the entire suburb of BSD is a massive building site with another 10 high-rise cranes outside this picture able to be seen from the windows of the MLA office. All this is going on regardless of government policies and from my perspective reflects supply and demand for local business and residential activity in the greater Jakarta area. I am not an economist but this looks to me like incredibly potent domestic consumption driven activity. There is nothing in this area with significant links to commodity exports. The activity in this area and most of the parts of Indonesia that I visit is related to developments of residential and business properties, hotels, office blocks, malls, hospitals, schools and universities almost entirely driven by private enterprise. If China can transform its economy to one relying on the same domestic consumption then we don’t have a thing to worry about.

Building site behind the MLA office in outer Jakarta.

The government is still planning to import a large number of breeders but it appears that the numbers might be reduced as the magnitude of the task becomes clearer to the government agencies involved.

Vietnam: Slaughter Steers AUD $4.05/kg (VND16,800 to $1AUD)

Prices of slaughter cattle continue to be depressed primarily by oversupply. Prices in the north are reported to be in a range from Dong70,000 to 68,000 while those in the south have been as low as 67,000. For this month I will use Dong68,000 as the HCMC indicator price.

While there are some small pockets of Foot and Mouth Disease remaining, the worst of the outbreak is over. El Nino however is still exerting its affect across the whole region.

The practice of disguising buffalo beef and pork as cow beef continues to be frequently discovered by the authorities and reported in the local press.

Thailand: Slaughter Steers AUD $3.39/kg (Baht 26.5 to $1AUD)

Slaughter cattle prices have finally got some help with the reopening of the China market via the Mekong River Grey trade. Prices for cattle suitable for this trade (better quality slaughter steers, bulls and buffalo) are 100Baht per kg live weight at the feedlot gate. This is about 10 Baht higher than the local price for domestic slaughter cattle and 15 higher than the price for Burmese cattle at the Mae Sot border market. If this river trade continues to expand to where it was a year ago then the oversupply in Thailand that flows into Vietnam will slowly resolve providing support for producers and importers across the Greater Mekong Region.

Malaysia: Slaughter Steers AUD $3.82 per/kg (RM2.98 to $1 AUD)

Prices remain generally static in Malaysia this month with the apparent price rise on the graph above due mainly to a strengthening Malaysian Ringgit.

Philippines : Slaughter Cattle AUD $2.69/kg (Peso 35.3 to AUD$1)

The season remains dry across most of the Philippines with the big news being the forthcoming Presidential elections in about 3 weeks time. While outgoing President Benigno Aquino has performed well, presiding over a much-improved economy, the country is still way behind the rest of the region in almost every economic and social measurement. This includes beef production, prices and consumption.

China: Slaughter Cattle AUD $4.89/kg (RMB 4.90 = AUD$1)

In Shanghai where the abattoir monitored for our report is for cull dairy cows, some cattle were rejected at any price. Those accepted for slaughter had their price reduced to Y16.8. In Beijing the slaughter price has eased back to Y24 per kg live. The AUD price for the graph above relates to the Beijing price.

Well-known branded product in the supermarkets is easily achieving 30% margins for the same unbranded cuts.

One of my agents advised that local press reports suggested that smuggled beef accounted for about 10% of all beef consumed in China with the greatest shortages experienced in the high-end restaurant sector.

Cambodia: Siem Reap, the city near the famous temple of Angkor Wat

I was lucky enough to visit Siem Reap recently and visited the main local Psaler wet market in the centre of the city early one morning. Beef prices were AUD$12 per kg with broiler chickens $4 and local chickens $8 per kg. Pork was $4.33. The Cambodian population is largely of the Buddhist faith but the beef section of the wet market is run solely by Muslims, mostly ladies. These prices are relatively high for Cambodia as Siem Reap is a huge tourist destination for not only Angkor Wat but also the many other temples surrounding the town. This location is one of the premier tourist destinations in all of Asia and in my personal opinion in the entire world.

Muslim ladies run the beef section of the Psaler wet market in Siem Reap city.

These local chickens look more like small emus but must taste pretty good to sell for $8/kg.

There have been many third hand reports that the two new western abattoirs and feedlots in Cambodia are almost ready to commence imports with some suggesting that their first shipments might be as early as this month (May). Regardless, they are both close to opening operations and delivering a new market for Australian cattle, further good news for northern producers to have another new destination for their stock albeit a low volume one.

Venice, Italy

My daughter Zealie was married in Venice last week and I visited the famous “wet” fish market on the Grand Canal (and adjoining modern butcher shops) in between the many wedding celebrations. Venetians obviously like their fish because it costs about the same as the beef – see the photos below. The prices are in Euro with 1 Euro equivalent to about AUD 65 cents.

Thanks to Flavia Garzia for this photo of Zealie and Stefano Tognon.

Dr Ross Ainsworth’s monthly South East Asian reports are first published exclusively on Beef Central. To view more of Dr Ainsworth’s previous Beef Central articles click here. To visit his personal South East Asia report blog site, click here.

Market price table for April 2016

(All prices converted to AUD)

These figures are converted to AUD$ from their respective currencies which are changing every day so the actual prices here are corrupted slightly by constant foreign exchange fluctuations. The AUD$ figures presented below should be regarded as reliable trends rather than exact individual prices. Where possible the meat cut used for pricing in the wet and supermarket is Knuckle / Round.

| Location | Date | Wet Market

AUD$/kg |

Super market

$/kg |

Broiler chicken

$/kg |

Live Steer

Slaughter Wt AUD$/kg |

| Jakarta | Nov 15 | 13.00 | 19.00 | 3.00 | 3.90 |

| Dec 15 | 13.00 | 19.00 | 3.50 | 4.15 | |

| Jan 2016 | 13.26 | 16.32 | 3.26 | 4.49 | |

| Feb 2016 | 12.95 | 19.69 | 2.90 | 4.40 | |

| March 16 | 12.83 | 18.18 | 2.93 | 4.19 | |

| April 16 | 13.00 | 18.20 | 2.90 | 4.00 | |

| Medan | Nov 15 | 10.50 | 11.00 | 3.30 | 3.70 |

| Dec 15 | 10.00 | 11.00 | 2.20 | 4.10 | |

| Jan 2016 | 12.24 | 10.61 | 2.45 | 4.29 | |

| Feb 2016 | 11.92 | 10.36 | 2.54 | 4.14 | |

| March 16 | 11.11 | 10.50 | 2.12 | 4.49 | |

| April 16 | 12.00 | 10.40 | 1.70 | 4.40 | |

| Philippines | Nov 15 | 6.47 | 6.88 | 3.61 | 2.65 |

| Dec 15 | 6.90 | 7.02 | 3.65 | 2.63 | |

| Jan 2016 | 7.53 | 7.23 | 3.70 | 2.71 | |

| Feb 2016 | 8.24 | 7.50 | 3.82 | 2.76 | |

| March 16 | 8.00 | 7.28 | 3.57 | 2.71 | |

| April 16 | 7.93 | 7.50 | 3.39 | 2.69 | |

| Thailand | Nov 15 | 9.34 | 10.89 | 2.72 | 3.89 |

| Dec 15 | 9.19 | 10.73 | 2.68 | 4.21 | |

| Jan 2016 | 9.84 | 11.02 | 2.76 | 3.93 | |

| Feb 2016 | 9.02 | 10.98 | 2.75 | 3.73 | |

| March 16 | 9.39 | 10.52 | 2.63 | 3.38 | |

| April 16 | 9.06 | 10.57 | 2.64 | 3.39 | |

| Malaysia | Nov 15 | 9.06 Buffalo | 11.33 | 1.78 | 3.43 |

| Dec 15 | 9.00 5.62 | 11.25 | 1.99 | 3.40 | |

| Jan 2016 | 9.18 5.83 | 11.47 | 2.13 | 3.48 | |

| Feb 2016 | 10.00 5.74 | 11.67 | 2.17 | 3.53 | |

| March 16 | 9.90 5.78 | 11.55 | 1.91 | 3.49 | |

| April 16 | 10.06 5.87 | 11.74 | 1.85 | 3.82 | |

| Vietnam | Nov 15 | 15.43 | 17.28 | 7.41 | 4.20 |

| HCM City | Dec 15 | 15.43 | 17.28 | 7.40 | 4.26 |

| Jan 2016 | 15.82 | 17.72 | 8.86 | 4.46 | |

| Feb 2016 | 15.52 | 17.39 | 8.07 | 4.34 | |

| March 16 | 14.88 | 16.66 | 7.74 | 3.99 | |

| April 16 | 14.88 | 16.67 | 7.74 | 4.05 | |

| China | Nov 15 | 15.22 | 21.65 | 4.34 | 5.43 |

| Beijing | Dec 15 | 15.38 | 19.57 | 4.27 | 5.34 |

| Jan 2016 | 15.86 | 19.91 | 4.35 | 5.39 | |

| Feb 2016 | 15.11 | 19.49 | 4.26 | 5.19 | |

| March 16 | 14.23 | 18.61 | 4.07 | 5.04 | |

| April 16 | 14.28 | 18.69 | 4.08 | 4.89 | |

| Shanghai | Nov 15 | 19.56 | 20.87 | 5.65 | 3.80 |

| Dec 15 | 18.37 | 20.94 | 5.98 | 3.84 | |

| Jan 2016 | 19.56 | 21.73 | 6.09 | 3.91 | |

| Feb 2016 | 17.87 | 21.70 | 5.96 | 3.72 | |

| March 16 | 14.63 | 18.21 | 5.69 | 3.45 | |

| April 16 | 13.88 | 16.33 | 5.70 | 3.43 |