145th Edition: March 2026

Key Points:

- Brazil and Canada are expanding market access in Southeast Asia as regional buyers diversify beef supply.

- Indonesia continues enforcing Ramadan beef price caps as cattle prices hold around IDR 55,000/kg liveweight.

- Tight cattle supply and wet season conditions are limiting availability into Darwin despite strong export demand.

Regional Trends and Overview

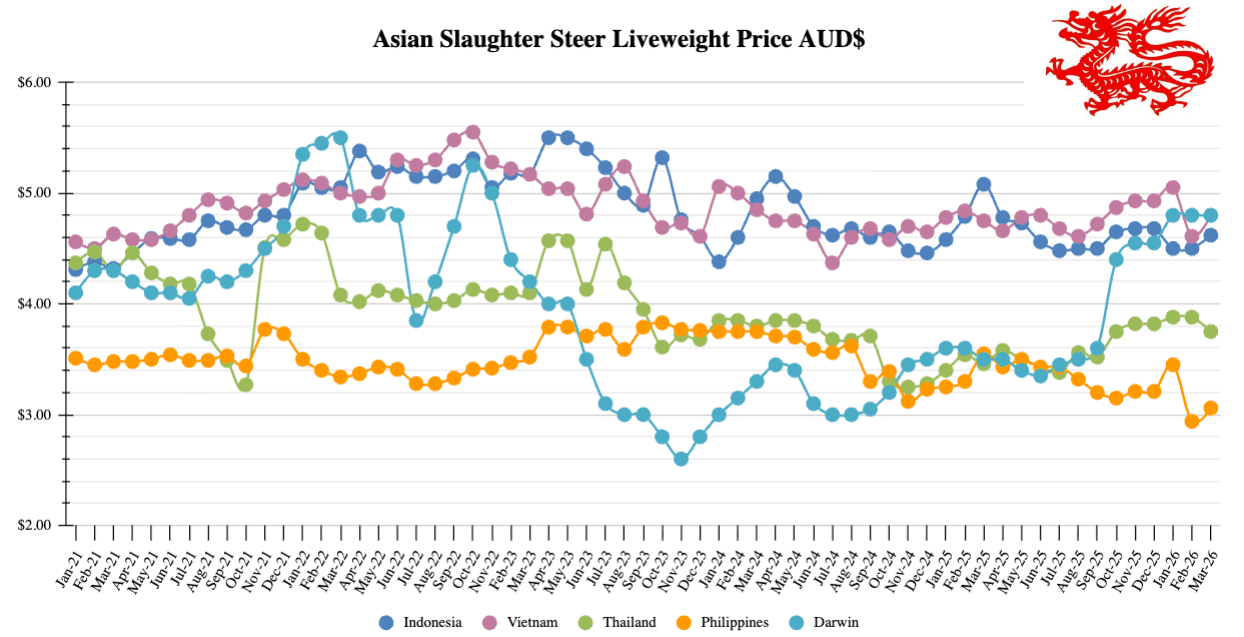

Regional Price Graph

Indonesia: Slaughter Steers $4.62 AUD per kg live weight (IDR 11,942 = $1 AUD)

Prices

Dr Michael Patching

Indonesian cattle prices have continued to strengthen since the previous report, with bull and steer prices now around IDR 55,000 per kg (AUD 4.62 per kg), extending the gradual upward trend seen earlier in Lampung and Java.

The increase reflects the ongoing pass-through of higher import costs and firm demand across the supply chain.

At the retail level, beef prices remain elevated, with wet market beef knuckle averaging about IDR 130,000 per kg (AUD 10.98 per kg) and supermarket beef knuckle reaching around IDR 157,000 per kg (AUD 13.18 per kg).

Meanwhile, chicken continues to offer a significantly cheaper protein alternative, with non-branded broiler chicken in supermarkets priced at approximately IDR 36,900 per kg (AUD 3.10 per kg).

The substantial price gap between beef and chicken continues to shape consumer purchasing behaviour across Indonesia’s retail protein market.

Photos: Local beef sales at an Indonesian wet market

Price caps enforced as Ramadan demand lifts

Indonesia’s government continues to enforce the beef price controls already in place for the Ramadan and Eid al-Fitr period, with authorities closely monitoring markets as seasonal demand lifts. We are now more than halfway through Ramadan, and recent messaging from Jakarta suggests officials are actively reminding traders and processors to keep prices within the established caps.

The official feedlot reference price remains around IDR 55,000 per kilogram live weight (AUD 4.61 per kg), with operators expected to align selling prices accordingly. At retail level, benchmark prices sit around IDR 130,000 per kilogram for forequarter beef (AUD 10.89 per kg) and IDR 140,000 (AUD 11.72 per kg) for hindquarter cuts. Frozen forequarter beef is around IDR 105,000 (AUD 8.79 per kg), while frozen buffalo meat remains the lowest priced option at about IDR 80,000 per kilogram (AUD 6.70 per kg).

Reported market prices during Ramadan have been hovering close to those levels, suggesting the policy is at least containing the usual seasonal spike. That said, keeping live cattle at IDR 55,000/kg while retail beef sits around the mid-IDR 130,000 range does not leave a lot of room through the chain, which is likely why the government appears to be leaning quite heavily on enforcement this year.

Indonesia looks to diversify food supply partners

Canada has recently secured expanded access for beef and pork into Indonesia under the Canada–Indonesia Comprehensive Economic Partnership Agreement, opening the door for products such as over-thirty-month bone-in beef. For Canadian exporters the opportunity will likely sit in Indonesia’s higher value imported beef segment, competing more directly with Australian chilled and frozen beef in modern retail and food service channels as the middle class protein market continues to grow.

To me this looks like part of a broader strategy from Jakarta to diversify its protein supply base. We saw Indonesia approve a number of additional Brazilian beef plants last year, and Brazil has also been allocated a larger import quota for 2026. When you add potential Canadian product into the mix, it is fairly clear the government is trying to ensure it has multiple supply options rather than relying too heavily on any single exporter. From an Australian perspective it is probably not an immediate threat, but it is a reminder that competition in Indonesia’s imported beef segment is only going to increase over time.

Vietnam: Slaughter Steers $4.80 AUD per kg live weight (VND 18,525 = $1 AUD)

Brazil continues expanding regional market access

Vietnam has also approved four additional Brazilian beef plants for export, further expanding Brazil’s access to the market. While the volumes involved are unlikely to shift the market overnight, it does reinforce a broader trend I have been watching across the region. Brazil has been steadily increasing its footprint in Southeast Asia, first through expanded access and larger quotas into Indonesia, and now through incremental approvals into markets like Vietnam. From my perspective this reflects Brazil’s long term strategy of building presence across multiple ASEAN markets, particularly in the frozen beef segment where price competitiveness tends to matter most. For Australia it is another reminder that competition in Southeast Asia is gradually intensifying as South American exporters continue to push into the region.

Vietnam election signals next phase of economic policy

Vietnam’s 2026 National Assembly elections are an important political milestone for the country, setting the composition of the legislature for the 2026–2031 term and signalling the policy direction for the next five years. While Vietnam operates as a one party state, these elections still matter because they effectively confirm the leadership priorities coming out of the Communist Party Congress and translate them into legislative and economic policy.

From my perspective, the vote is likely to reinforce the government’s focus on economic growth, industrial development and food security. That matters for the region because Vietnam is steadily becoming one of Southeast Asia’s more important importers of livestock and agricultural products, including Australian beef and cattle, and the policy direction set over the next five years will influence how that demand continues to develop.

Hog Prices Rebound as Sector Stabilises After Difficult 2025

After a year marked by African Swine Fever outbreaks, flooding and uneven market conditions, Vietnam’s livestock sector is entering 2026 on a steadier footing. Authorities report that overall production remained stable through the disruptions, with food supply secured ahead of Tet.

The most notable shift has been in live hog prices. Values lifted sharply from around VND 50,000 per kilogram late last year to approximately VND 80,000 at the end of January, before easing slightly to around VND 77,000. Strong seasonal demand ahead of Lunar New Year combined with herd losses in affected regions tightened supply more than earlier forecasts had anticipated.

While pork remains the dominant protein, the volatility highlights how sensitive the market remains to disease events and weather disruption. Company results through 2025 reflected that uneven environment, with several larger operators reporting improved earnings as prices strengthened into year-end.

The broader direction is one of recovery rather than expansion. Production has stabilised, pricing has improved, and confidence appears firmer heading into 2026, but underlying risks around feed costs and disease management remain part of the operating landscape.

Photos: Pork products on display in a Vietnamese supermarket

Philippines: Slaughter Steers $3.06 AUD per kg Live weight (₱41 = $1 AUD)

Prices

Livestock prices in the Philippines continue to show a largely stable trend, with only mild movements observed across key categories. Wet market beef knuckle has inched higher to ₱360 per kilogram ($8.80 AUD), while supermarket beef knuckle remains steady at ₱415 per kilogram ($10.15 AUD). Slaughter steer prices have posted a modest gain, rising to around ₱125 per kilogram (about $3.06 AUD). Meanwhile, pork carcass values are holding firm at ₱240 per kilogram ($5.87 AUD).

In poultry, supermarket broiler prices are unchanged at ₱170 per kilogram ($4.16 AUD), while branded products such as Magnolia continue to trade near ₱247 per kilogram ($6.04 AUD). Overall, market conditions remain balanced, with price movements suggesting stability rather than any decisive shift in direction.

Photos: Local meat and livestock sales in Mindanao

Swine and Poultry Rebound While Cattle Numbers Continue to Edge Lower

Recent data out of the Philippines suggests pork and poultry are slowly recovering, but the cattle sector continues to drift in the opposite direction. The national swine herd edged up about 0.5 percent year on year to 8.79 million head in the fourth quarter, with hog production lifting 1.6 percent. Poultry performed more strongly, with chicken inventories up 5.2 percent to 217 million birds and production rising more than 9 percent.

What stands out to me is that the structure of the industry has not really changed. Around 78 percent of pigs and more than 86 percent of cattle are still held by smallholder farms. That fragmentation makes it difficult to scale production quickly or improve productivity in any meaningful way.

Cattle numbers continue to trend down. The national herd slipped another 1.3 percent to around 2.5 million head, with beef output also falling slightly. From my perspective this reinforces the longer term pattern we have been seeing in the Philippines and neighbouring countries. Pork and poultry are gradually filling more of the protein demand, while the cattle sector remains constrained by small scale production and limited investment. For exporters, that probably means the Philippines will continue to rely on imported beef rather than building a significantly larger domestic herd anytime soon.

Australia: Feeder Steers Darwin $4.80

In Darwin the past month has felt fairly steady, largely because feeder prices have remained at historically strong levels. With values sitting around the $4.80/kg liveweight range, exporters appear comfortable continuing to ship cattle when they can source them.

The bigger challenge at the moment is availability. Wet season conditions across much of the Top End are limiting road and yard access, so several exporters have been forced to look further south to assemble consignments. Demand from Indonesia remains solid, which is why prices have held up despite the logistical constraints.

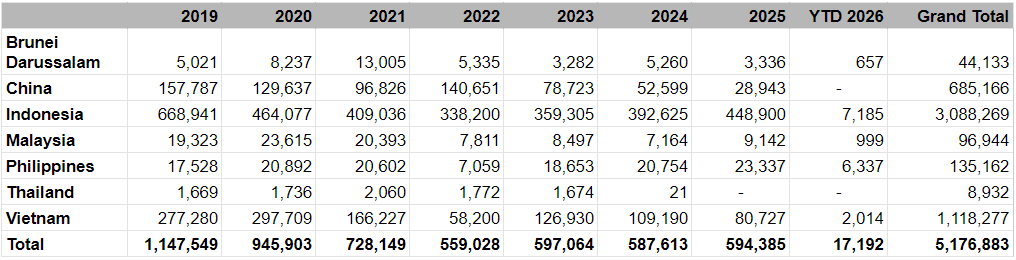

Year 2026 cattle exports – comparison across SE Asian markets

Source: DAFF website