111th Edition: April 2023

Key Points:

- Ramadan kicks off around the Islamic world

- Despite reduced cattle prices in Australia reduced demand still seen across SE Asia

Hear from an impressive Thai cattle farmer: This month we have started a new section to the SE Asia report which is a podcast/audio series called “Meat the Market Asia”. We will talk with local farmers, traders, real people in SE Asia so you can understand what is going on directly from them rather than secondhand from me. Contact me if you have a story you want to share.

In the first episode I talk with Pui from Loong Chow Farms in Thailand. A third generation cattle farmer who trades local cattle, has his own breeder operation, imports live cattle from Australia, and has partnerships with high value beef restaurants and distribution. Thank you to Simon Hopwood from SEALS for the reintroduction to Pui. Further information on some of the interview content can be found in the Thailand section below.

Meat the Market Asia – Podcast Link (Spotify)

Pui from Loong Chow Farms Thailand

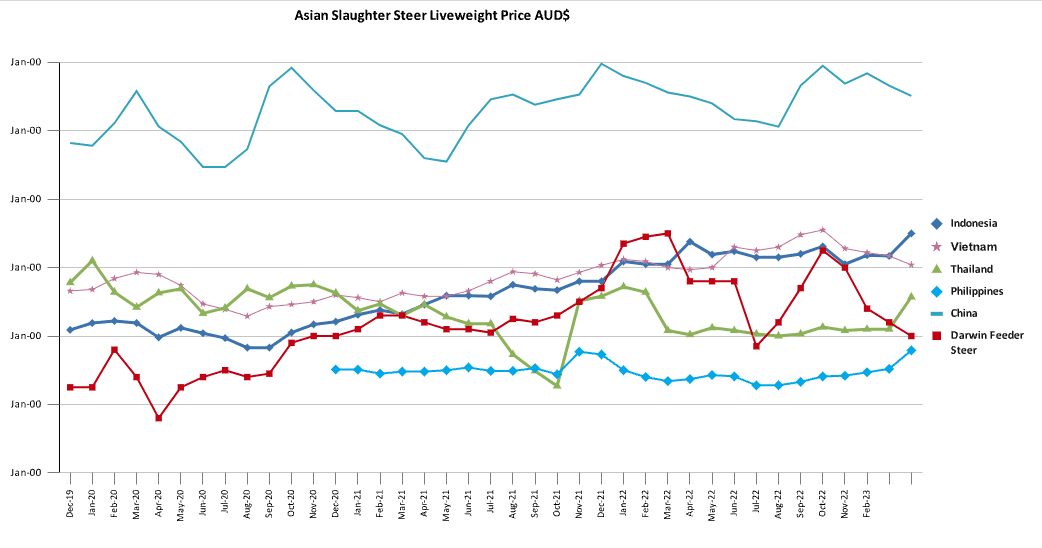

Indonesia : Steers AUD $5.50 / kg live weight (Rp10,080 = 1AUD)

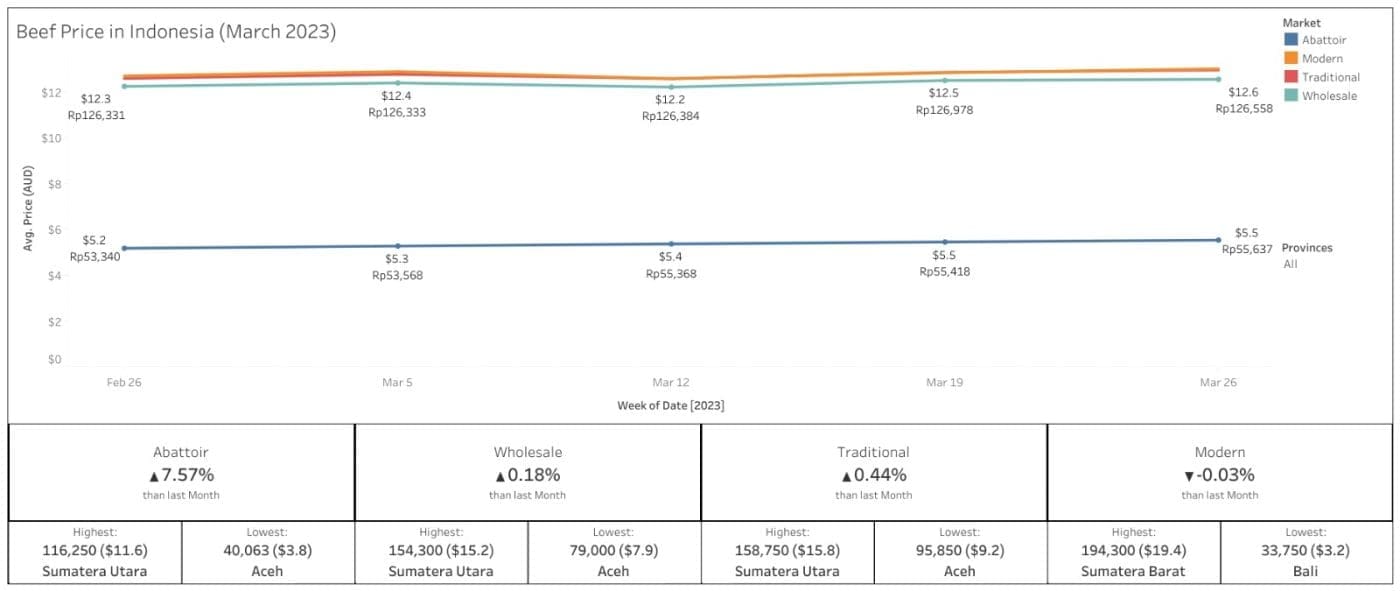

Prices of cattle and beef in Indonesia during the month of March 2023. Source: Adapted by Alta from Simponi Ternak

Ramadan has kicked off across the Islamic world and will run from March 22nd to April 20th. Ramadan is an important religious event for Muslims globally. During this holy month, Muslims fast from sunrise to sunset, abstaining from food, drink, and other physical needs. As Indonesia is the world’s largest Muslim-majority country, the fasting month of Ramadan is widely observed throughout the country.

Ironically the period of fasting is also generally a period of increased consumption, especially beef. During this month, Muslims usually have two main meals: one before dawn, called sahur, and another after sunset, called iftar. The pre-dawn meal is intended to provide sustenance for the long day ahead, while the iftar is a time for breaking the fast and sharing food with family and friends.

Ramadan is a time of spiritual discipline, of deep contemplation of one’s relationship with God, extra prayer, increased charity and generosity, and intense study of the Quran. Ramadan is also about fasting and sharing food.

Beef consumption peaks just before the start of Ramadan and during Lebaran (Eid al-Fitr, Hari Raya Idul Fitri) which is the end of the fasting month (22 April). Many Indonesians view beef as a luxury item and save up to buy it during this time. The demand for beef usually increases significantly during this period but we are yet to see the spike. Imported frozen beef including IBM is a strong contributor. Prices are still expected to increase in the last week.

The reports are that in the few days leading up to Ramadan the slaughter rate increased four times in Jakarta and two times across the rest of the country. This is positive but the total slaughter volume is down considerably from previous years due to the impact of cost of living concerns and the impact frozen beef is having on consumption trends.

With 123 million people returning home to their villages to celebrate with their families for Lebaran there will be an increase in beef consumed in rural villages and less in Jakarta. Cattle prices into abattoirs increased over the last month on average, but as the new dataset shows there is a huge range across different islands. Feedlot capacity for Australian cattle is reported to be around 70 percent.

Indian Buffalo Meat: The newspaper Kompas has continued to print media reports about the impact of frozen beef imports including Indian buffalo meat (IBM). The articles continue to claim that the purpose of the frozen meat imports was to decrease the price and therefore accessibility for average Indonesians, especially for processed products like bukso balls. But this hasn’t happened and beef continues to be an expensive product. Similar articles stress the lack of consultation with local farmers on the frozen beef quotas and the impact imported beef has had on local breeding businesses. With the added impact of LSD and FMD many local farmers are feeling significant pressures in Indonesia at the moment.

We will discuss Eid Adha (Qurban) in more detail in the coming months (not until the 29 June), but for Indonesia there is already speculation about what will happen with local cattle prices and availability, especially as suitable slaughter stock numbers have been depleted due to FMD and LSD impacts. Australian cattle are generally too large (expensive) for ritual slaughter in Indonesia and Malaysia as participants are paying for the animal rather than salable meat yield. It is possible that there will be an increase in sheep and goat slaughter in Indonesia, but don’t put in your trade enquiries yet, Australia does not have slaughter protocols signed for sheep and goat.

It seems that Indonesia may have stopped reporting new cases of FMD in Indonesia with no change since last month and the reporting site is now under maintenance https://crisiscenterpmk.ditjenpkh.pertanian.go.id/?l=en The reports of large FMD outbreaks has reduced, but there will be ongoing economic impacts.

For consultants in the audience, keep your eye out for Katalis IA-CEPA projects that are being reviewed and will be going out to tender in the next few weeks/months. These will mostly be feasibility studies and market entry analysis for new products or opportunities across a range of opportunities including beef and cattle.

Vietnam: Steers AUD $5.04 / kg live weight (AND15,658 = 1AUD)

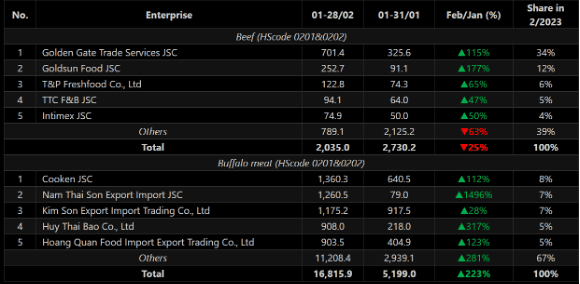

I remain quite bearish on the Vietnam market for live exports, but the opportunities for boxed beef exports remain exciting albeit difficult due to the fragmented market with lots of small importers. Below is a breakdown of the top importers in Vietnam from the first couple of months of 2023 extracted from Vietnamese customs data. Lots of small importers and relatively large volumes of IBM.

We will need a longer dataset, but the growth in IBM imports in February (+223%) is something to continue to monitor and could either be due to high purchase volumes for Tet, or driven due to the cost of living crisis just hitting Vietnam. Note that now that transshipment to China has essentially stopped it can be assumed that all the IBM is remaining in Vietnam.

Data on Top 5 buffalo and meat importing enterprises of Vietnam in February 2023, month on month (mt). Source: Adapted by Agromonitor from Vietnam customs data

For the live export market. Some breeder cattle imports were reported in March, but there remains a limited demand for slaughter or feeder cattle exports to Vietnam. The price is reported to be back to under US$3.00/kg CIF (landed in Vietnam) and there are reports that there are several shipments planned for April and May. Feedlots are relatively empty, with only around 20,000 head currently on feed, however the slaughter rates are also very low with only a maximum of 3,500 head of Australian cattle being slaughtered every month. This contrasts to 2019 where one importer was processing 9,000 head in some months. The abattoir price remains stable for steers at VND 82,000 in the North and VND 79,000 in the South. And bulls are about VND 85,000.

Higher quality hot meat supply abattoir in Southern Vietnam. Was previously slaughtering high numbers of Australian cattle, now is only processing local cattle.

To make matters worse, the summer months are traditionally a period of decreased beef demand. Hot pot season ends in Hanoi in the north, and people move to cooler meats like chicken.

For Vietnam, China has recently announced that all illegal cross border trade will end by 2025. As previously reported, the volume of cattle moving over the border to the north is already negligible, but the announcement combined with ongoing restrictions at the Vietnam-Laos border due to salbutamol is worth observing. The outcomes of all this could be a more regulated regional trade and this presents a myriad of potential scenarios and outcomes which could equal more or less demand for Australian livestock in the region. My opinion is that it will likely result in less Austrlian exports as regional cattle in the region will just move into Vietnam (but it is a lot more complex than that).

As discussed by Pui in the podcast, Vietnam is maintaining the closure of the border for movements of cattle out of Thailand due to ongoing scrutiny over the use of salbutamol. Vietnam continues to test and penalise salbutamol use, but it is still being detected in pig farms in Vietnam and so also likely in the cattle industry. In an Asian Agribiz article one farmer reported that “He (the pork buyer) said if I don’t, he will not buy the pigs because the meat colour and lean percentage are not good enough”. Beta agonist use is widespread in the region and while awareness is the key to stopping its use, the livestock (pig and cattle) are currently unprofitable without it.

In more positive news, Chinese tourists have returned to Vietnam under a restricted group tour arrangement. The restrictive nature of the tour group setup will do little to immediately increase spending in the country, but it is at least a positive step for tourism and economic growth.

A second round of the Australia Vietnam Economic Grant (AVEG) is now being tendered for. Applications close on 14 April.

Darwin (AUD $4.00)

As reported last week prices for Australian cattle have been dropping and there are more available cattle for the live export trade in both Darwin and Townsville.

As noted previously and in other sections, there is a significant shift in the demand from importers in feeder and slaughter markets and this looks to be the main limitation going forward and is something that Australian producers will need to consider in the coming months. Even as cattle become available it is unlikely that it will be met with the same enthusiasm that we have seen in other cycles. And with the change in the market dynamics and penetration of frozen products it is not likely to ever return to pre-COVID levels even with a significant price decline.

Thailand Steers AUD $4.57 (Tb 22.90 = 1 AUD)

As discussed above, the Thai trade to Vietnam through Laos remains closed due to Salbutamol restrictions on the Vietnamese side of the border. The Vietnamese Government has met with the Thailand Government equivalents but at this stage there is still no information on when or how the border trade will reopen. This has resulted in a higher price for local cattle.

There are reports of the border trade between Laos and China reopening including cattle on the ferry ride from Thailand up the Mekong River to China. China has a closer relationship to Laos than Vietnam and has built quarantine yards at the Laos – China border with the intent of starting an official trade. China is going to have to enforce stricter movement restrictions on unofficial cattle movements from Laos if they want this to be profitable and sustainable.

As confirmed by Pui, it is risky and costly for companies to rely on any trading cattle between countries. Many trader businesses have lost a lot of money in the last few years due to COVID and Vietnam border closures. Loong Chow Farms previously had a specific part of their business dedicated to breeding and trading cattle for the China and Vietnam markets, but they are now moving out of this trade altogether as it is now too unpredictable. Local cattle are trading at a higher 105 Tb/kg while Loong Chow Farm cattle are attracting a premium above 115 Tb/kg depending on breed.

Loong Chow Farm in Thailand. The sheds in the back are the feedlot and breeding pens

Loong Chow Farms imports most of the 20,000 Australian cattle annually (Approx one shipment every 2 months) all of which go into domestic processing and consumption. This has grown quickly from the 1-2 annual shipments in 2017. The cause of this growth is attributed to their focus on value adding down the supply chain and partnership with Company B. They are now processing and producing high value products suitable for the Thai market from Australian cattle. This steady growth has not been easy as they have had to constantly find new markets for their products, and new ways to create value from their beef. The Beef Master restaurant is definitely the showpiece store for Company B with their quality beef products, and I strongly advise anyone passing through Bangkok to try it for yourself. You can contact Loong Chow Farms through their Facebook page.

Cabinet for Beef Master Restaurant and Retail in Thailand. Source: Simon Hopwood SEALS

Philippines: Slaughter Steers AUD $3.79 / kg liveweight (P. 36.9 = 1AUD)

The Philippines remains under pressure from the cost of living crisis and average Filippinos continue to struggle. But the Philippines more than most other countries in the region has a large wealth gap. There are growing opportunities in the Philippines to export higher value cuts to specific areas, especially the southern islands including Mindanao which has been generally underserviced, likely due to travel warnings about the region and terrorism risks. There are large parts of Mindanao that are now safe for travel.

For live export, they have imported 3,726 head so far in 2023 and there are plans in place to import more in the coming months. The reduced price of Australian cattle will no doubt help with trade into a market that is very price sensitive.

In a future podcast we will talk with Raymond Hernandez from RSRH Livestock in the Philippines who will tell a very similar story to Pui from Thailand with their cattle importing and beef processing business and the desire to import higher quality cattle to service their niche customer base.

In Mindanao the wet market beef knuckle price remains at about P.560.00/kilo and supermarket beef knuckle at P.600.00/kilo. Beef price for hot carcass local cattle is P.260.00 Kilo. Slaughter steer price has increased to between P.130.00 up to 140.00/kilo liveweight.

China: Local Slaughter AUD 7.51 / kg liveweight (RMB 4.66 = 1 AUD)

In Beijing the beef price in wet markets has dropped from 96 to 88 RMB over the last month. With some products being sold for 78 RMB. A similar trend is being seen in supermarkets which have dropped from 126 to 100 RMB over the last month. Live cattle prices have not changed since last month and remain about 35 RMB / kg liveweight.

The Chinese trade with Brazil has reopened and this temporary ban has had minimal impact across the rest of South East Asia. There has been a delay in Indonesia’s receival of the Brazilian quota, but this is not directly related to the BSE case from Brazil.

Very detailed and well explained analysis of live export destination markets in SE Asia Mike.

Your research is a great sounding board for validation of “on the ground” price trends in several markets in which we have an interest.

Neil