119th Edition: December 2023

Key points:

- Election in Indonesia in February, Ramadan in March, and delegation to Australia.

- Vietnam Tet in February, and graduation ceremony for abattoir workers trained in Vietnam.

- All countries in the region are showing slow growth and rebound from cost-of-living crisis.

Regional Trends and Overview

Dr Michael Patching

As we close another year, it’s becoming clearer that the South East Asian markets have undergone a change that lays a foundation for the next 5-10 years in the beef and cattle trade to the region.

Global economic shifts have affected manufacturing and tourism-dependent nations more than others, contributing to reduced consumption of various products and a visible cost of living crisis in many regional countries. Particularly noteworthy is the disappearance of the “growing middle class” in China, once a cornerstone of regional and global trade. Fortunately, we are now seeing the start of recovery which will be gradual and may take several years.

The main shift for the cattle and beef sector is the growing acceptance, and sometimes preference, for frozen beef over traditional “fresh” (locally slaughtered) meat. The trend of frozen meat integrating into traditional distribution channels presents new challenges for the live export industry but opportunities for the boxed trade. The live export challenges go beyond the usual factors of price, livestock availability, and the occasional market access risk. I would caution Australian producers from overinterpreting the recent increase in imports into Vietnam and Indonesia as both nations are preparing for high volume periods of Tet and Ramadan respectively. I believe that the future of the live export industry will increasingly be reliant on the investment in downstream capabilities, especially abattoirs, by Australian and international supply chain partners.

And this becomes the significant opportunity for Australian exported beef, strengthening its position in Asian supply chains. In countries with options for cheaper beef/buffalo products, Australian beef exporters are racing to the bottom if we are only competing only on price and we cant trade enough volume if we rely on high value products. To grow a product or brand in any country we need consistency. The brands and products that are now succeeding in specific countries have a reputation for consistent quality product that meets the market price, these are not the cheapest or the highest ‘quality’ product.

There has been little change in the movement of livestock in the region in the last month. Laos Government continues to look for opportunities to export both live cattle and beef into China and have recently started investing in a large abattoir in Vientiane with Chinese support. It is not in a GACC China approved zone and I question its ability for it to export products irrespective of where the investment is coming from. We have seen this too many times before in Asia.

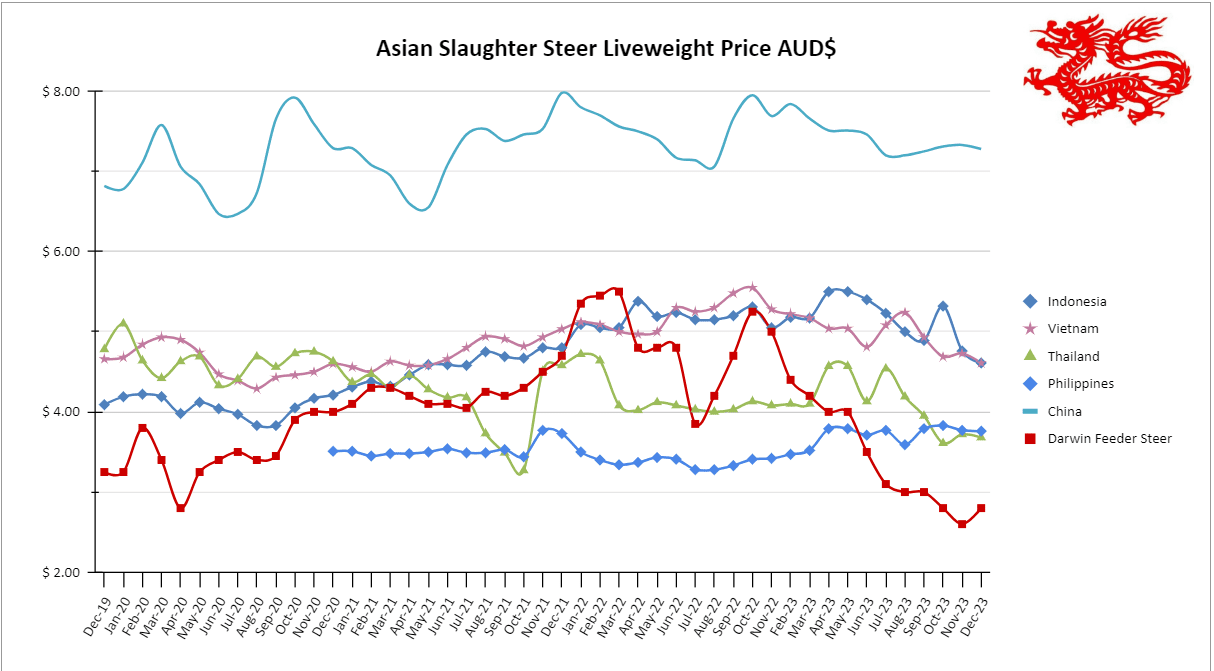

Indonesia: Steers AUD $4.61 / kg live weight (IDR 10,247.99 = 1 AUD)

The price of beef cattle remains stable in the wet markets (135,500 IDR on average) and in supermarkets (164,700 IDR on average). We expect a slight increase in the buying trend for beef, especially over weekends during December, mainly as a lead up to the Christmas and New Year’s holidays. The carcass price is between 91,500-94,500 IDR. Ramadan in Indonesia starts on the 10 March 2024 and preparations for that period should be underway.

The commencement of Indonesia’s 2024 election campaign period marks a crucial time in the nation’s political landscape. Running from November 28th to February 10th and elections to be held on the 14th of February (how romantic). The Indonesian government has pledged to maintain effective governance, despite ministers’ engagement in campaign activities. The election is significant for Indonesia and everything that is happening in the country should be examined within its lens.

The beef sector in East Java has announced self-sufficiency in meat production. This achievement has largely been attributed to a successful artificial insemination program, and is being promoted as a testament to the effectiveness of local initiatives. East Java is a significant contributor to Indonesia’s cattle population and domestic supply. There is a risk that this may further destabilise the relationship between Indonesia and Australian live cattle trade, as it demonstrates lack of dependence in a politically important period. Artificial Insemination (AI) bodies that produce bull semen in Indonesia are the Singosari Center for Artificial Insemination in Malang, East Java, and the Lembang Center for Artificial Insemination in West Java.

However it should be noted that despite strides in local production, Indonesia continues to rely heavily on imports to fulfil its demands. Recent data from the National Food Resilience Agency (Bapanas) underscores this dependence. Beef availability in 2023 has been projected to reach 787,103 tons, with only 510,659 tons being produced domestically. the remainder are imports. And it is estimated that there will be an end-of-December 2023 stock of 87,084 tons remaining in storage.

FMD and LSD remain a concern for local farmers. There have been no important new reports made, however farmers continue to privately report issues with stock losses and sporadic outbreaks. Cattle insurance continues to play a pivotal role in providing financial support to livestock farmers during unexpected events like sudden cattle deaths or health-related issues and is a key determinant for declarations of disease events. If the insurance level is not high enough there is little incentive for reporting disease. For farmers in Tabalong, Kalimantan the claim amount has been worth IDR 10,000,000 (AUD $980) and reportedly has served as a safety net, mitigating the financial impact of livestock losses in instances where cattle have died unexpectedly or faced complications such as FMD outbreaks.

Unofficially, the Indonesian delegation to Australia expressed satisfaction during their recent visit to look for evidence of LSD, this included the testing processes they observed. Notably, they were intrigued by the absence of any positive LSD results during their visit and were certain they would find evidence. The delegation had the opportunity to witness testing firsthand, even on cattle with spotty appearances, and were also shown laboratory facilities to underscore the reliability of the testing systems.

This visit marked a significant step forward in the ongoing efforts following the early September agreement to reopen trade. A key component of this agreement is the commitment to a joint investigation. The next phase involves technical discussions at the officials’ level, building on the insights gained from the visit. The Australian industry is supportive of Indonesia’s approach to addressing their concerns, emphasizing patience and understanding. It has been made clear that there will be no compromises regarding our stringent disease-status standards or the health protocols that define the conditions for trade. This stance reinforces Australia’s commitment to maintaining the highest standards of health and safety in trade practices.

Vietnam : Steers AUD $4.63/ kg live weight (VND15,996.80 = 1AUD)

The pricing landscape for Australian cattle delivered to Vietnamese abattoirs continues to display competitiveness, offering a cost advantage over local cattle and imports from neighbouring Thailand and Laos. Steer prices have seen an uptick, reaching VND 74,000 per kg liveweight, while bull prices are marginally higher at VND 75,000 per kg. In wet markets, the wholesale price for hot beef has recently decreased, now standing at VND 189,000 (approximately AUD $11.81) per kg.

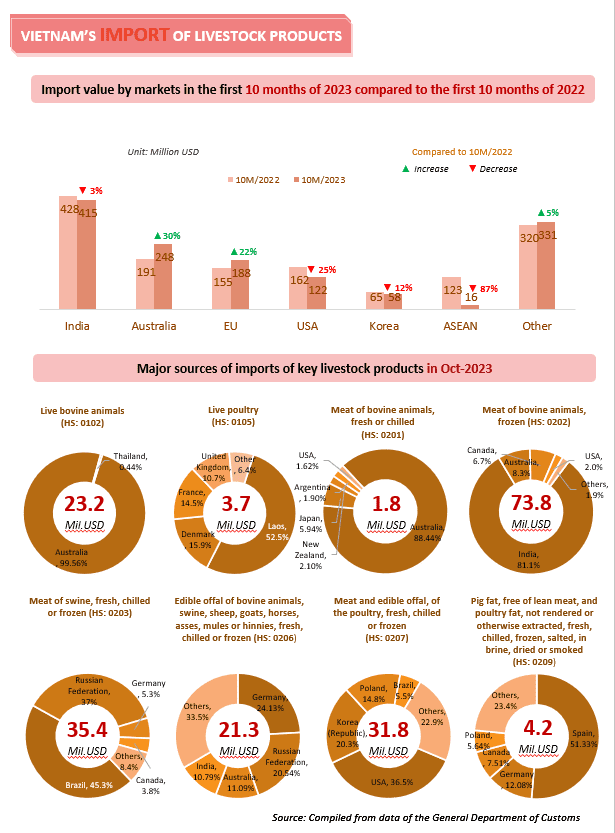

Printed Source: Asia Beef Network

The data printed above from the Asia Beef Network tells a few important stories. Australian imports into Vietnam continue to rebound well with a 30% increase in value of all products (live and boxed) in the first 10 months of the year, with reports that this growth is continuing in the build up to Tet (Vietnamese New Year) in early February 2024. But it also shows the position of Indian buffalo in the country, where it holds a large share of the import value but has not shown any growth. The country is basically saturated for the Indian product and we will continue to see value increases coming from other countries such as Australia, US, and Canada when they have competitive product to sell.

Regarding live exports, the recent increase in live export numbers into Vietnam still needs to be headed with some caution. Recent visits to Vietnam did not convince me that there has been any significant shift in the consumption of beef from Australian live cattle and what we may be seeing is an opportunistic reaction to the price of cattle in Northern Australia, and instability in Indonesia, rather than a genuine shift in market demands. The numbers of cattle remaining in the feedlots in the coming months and over Tet will be the indicators for 2024 performance of the trade.

Training for Mutual Benefit

The establishment of a first-class skilled meat worker training program in Vietnam is another milestone in addressing the shortage of skilled workers in Australia’s meat processing industry. This initiative is the result of a joint venture with shared equity between Katherine Pastoral Company of Australia and Mr T Beef, a subsidiary of the Vietnamese industrial conglomerate Quang Phat Group. The abattoir and Quang Phat Group have been involved in the import and slaughter of Australian cattle since 2014, but now processes a mix of Australian, Thai, and domestic beef for the Vietnamese market. The purpose-built boning room in Long An, South Vietnam meets Australian standards and is integral to the intensive training courses modelled after Australian certification modules. The program has made a commitment to practical experience and is managed by an onsite Australian manager and MINTRAC assessor, Adrian Prior. Adrian is a unique trainer who was able to really connect with his Vietnamese students and a great ambassador for Australia. This operation recently celebrated its first round of graduates, with graduates securing employment with EC Throsby in Singleton and Young NSW. Donna Throsby from Throsby’s made the journey to interview each of the graduates and their families personally.

This is the second of two initiatives being run in Vietnam to build new models to address workplace shortages in Australia. The significance of this collaboration is that it not only addresses workforce shortages but also fosters economic ties and cultural exchange between Australia and Vietnam. And it provides alternative income for meat companies so that they can invest in further industry developments.

Very proud Cert III Graduates with the company reps and trainers.

Philippines: Slaughter Steers AUD $3.76 / kg liveweight (P. 36.54 = 1AUD)

In the Philippines, the beef market has maintained its status quo over the last month, with prices remaining stable. In wet markets and supermarkets alike, beef knuckle has been trading at P. 560/kg and P. 600/kg, respectively. Local cattle prices in Mindanao are still pegged between P. 130-145/kg liveweight, and the hot carcass meat price is approximately P. 260/kg. It is important to note that these figures pertain to cattle bred and traded within Mindanao, not Australian imports.

Thailand Steers AUD $3.68 (THB 23.22 = 1 AUD)

Thai live cattle prices decreased slightly to Tb 85.43/kg ($3.68 AUD). The common problem of high feed input costs continues to impact the local industry.

Feeder Steers Darwin $2.80 Townsville $2.60

The northern export feeder steer price has finally turned the corner and has trended up over the last few weeks. This follows a general rise in cattle pricing across Australia, with other domestic cattle indicators also rebounding from what producers hope was the bottom of the market. This is largely a result of rainfall events across the east and northern cattle producing areas and the annual seasonal start of the wet season in Australia’s North which has restricted supply of cattle on the market.

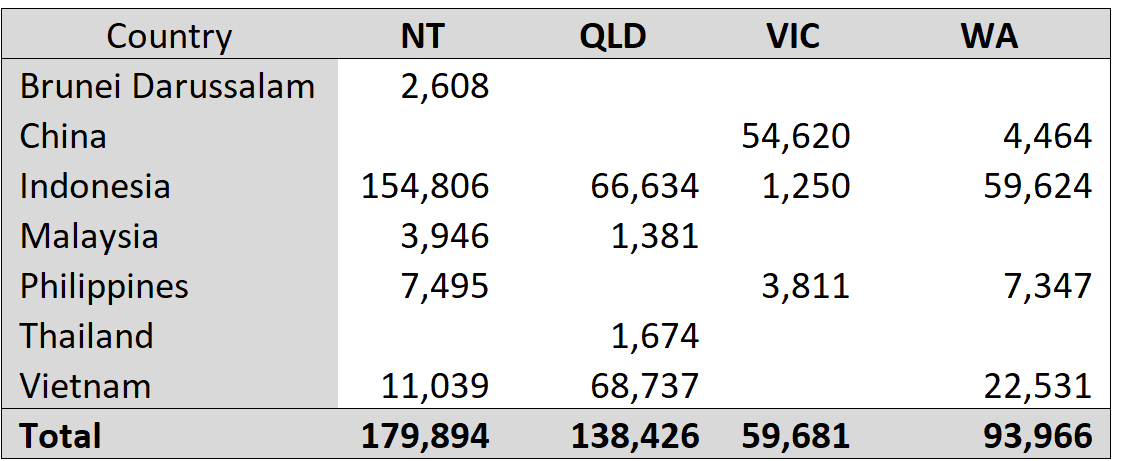

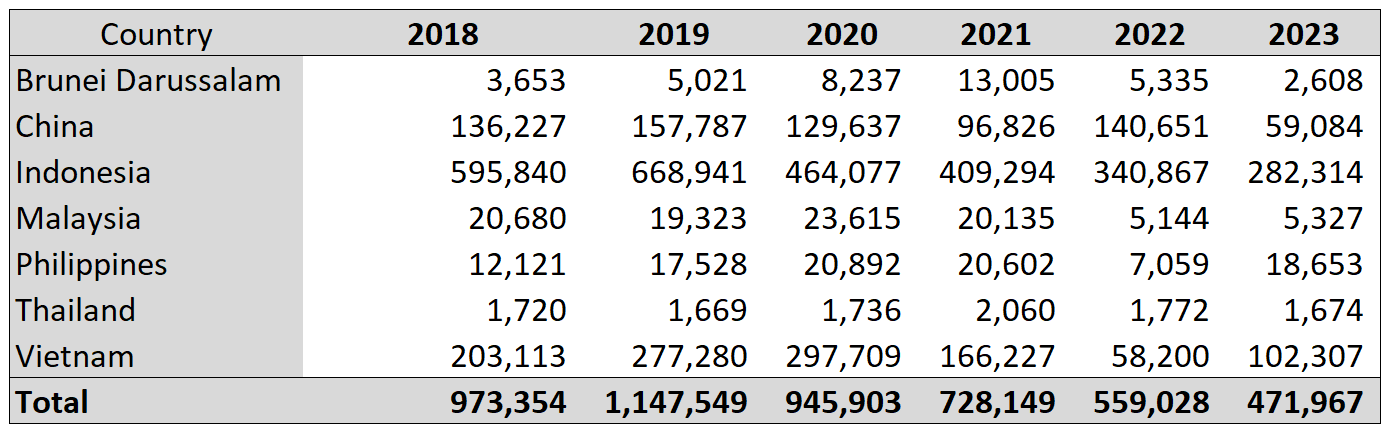

2023 Year to October figures for cattle sea freight across Asia for our different ports from the DAFF website.

Year to October for cattle sea freight comparison across Asian markets from DAFF figures.

Michael, I wouldn’t read much into anything coming out of a Pollies mouth in this country, especially in the next 12 months …

A good case of “Foot in Mouth” as there are droves of Aust’n cattle from West Java and Lampung in the Surabaya market and downward pressure on prices accordingly..

I reckon there are 2 things saving the Aussie fdr cattle market here.. 1 is the enormous margins being enjoyed by the Govn on the Indian buffalo meat trade which indirectly established a putting a high floor price of beef here and, 2.. local farmers will scream their guts out if the price of their cattle goes too low..