The live cattle trade between northern Australia and Indonesia has been an amazingly successful international trade phenomenon for most of the last 30 years.

The resilience of the business model has been demonstrated on two separate occasions when the trade suddenly halted.

The first was the Asian financial collapse in 1997/98, followed by the Australian government’s closure of the trade on welfare grounds in 2011.

In both cases the trade recovered quickly as a result

of the rock-solid commercial logic driven by all the critical elements of the business case listed below:

- Domestic cattle supply shortfall with no chance of recovery

- Extremely strong social preference for fresh beef from the wet market network.

- Sustained economic development resulting in rising standards of living

- Beef is the premier meat protein with pork excluded as an option

- Cheap feeder cattle from northern Australia

- Cheap agricultural bi-products for fattening rations allowing for low cost value adding

As of today, the first four factors still strongly support the model.

Unfortunately, the critical contributions from five and six are declining at an alarming rate:

- The domestic cattle supply has made no significant gains in 30 years. The recent introduction of Foot and Mouth (FMD) and Lumpy Skin diseases (LSD) have ensured that the national beef herd will enter a new phase of accelerated decline.

- Preference for fresh beef has not changed significantly despite the introduction of much greater volumes of refrigerated beef in modern retail outlets.

- National economic performance remains impressive with current and forecast GDP growth in the 5% zone. This growth appears to be sustainable with robust domestic demand, a rapid post-covid recovery in tourism and a commodity export boom.

- Pork consumption will never be significant with an 87% Muslim population.

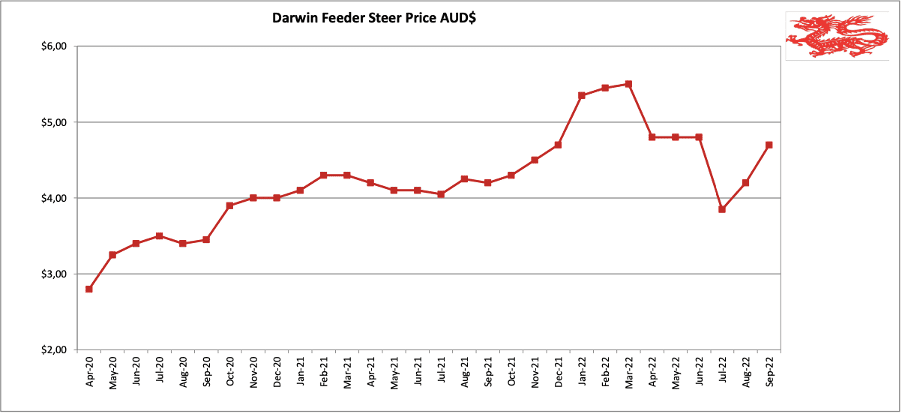

- Northern Australian feeder cattle prices appear to have entered a new range of much higher rates as a result of a number of factors including strong world-wide beef demand leading to increasing demand for northern feeders from the eastern states of Australia and the very slow herd rebuilding after the last drought. Importers cannot survive the 2 to 4 year wait until prices cycle down once again.

- The reduced availability and high cost of agricultural biproducts for feedlot rations is also unlikely to reverse as technology advances in the processing sector will probably lead to reduced availability and even greater upward pressure on prices.

In the early years of the trade, when input prices rose, importers were able to increase the price of slaughter cattle to maintain profitability. During the last decade, the Indonesian government food security policy has imposed extremely strict fixed price limits on slaughter cattle sales effectively preventing importers from adjusting their margins to meet new cost pressures.

Without a consistent supply of low-cost feeder cattle and cheap feed ingredients or the ability to raise output prices substantially, profitable lot feeding is almost impossible despite the extremely efficient value adding operations of well managed Indonesian feedlots.

The likelihood of future feeder prices falling back to AUD$4 or below are very slim. The 2022 May-June drop was related to the FMD outbreak.

One possible solution is to reconsider the concept of grazing Australian feeder cattle on grass under oil palms for the majority of their weight gain then returning them to the existing feedlots for a short final finishing and distribution.

Feeders grazing under palms are able to gain at least 300 grams per head per day (value Rp15,000 @ Rp50,000 per kg live weight) at a cost of less than Rp10,000 per day. This represents AUD 50 cents net profit per head per day. A 300kg feeder growing at 300 grams per day will take about two years to reach 500kg. And the plantation owner gets a significant cash bonus in the form of reduced herbicide costs as the cattle act as biological lawn mowers.

If the net profit is Rp5,000 per head per day then the annual profit per head is Rp1,825,000 or AUD $182.50 @ Rp10,000 = AUD$1. Profit for the two-year grazing period is about AUD$365 per head.

With the average plantation size at about 5,000 hectares, and a conservative stocking rate of one steer to 5 hectares, this means that an average plantation might be able to graze up to four groups of 250 head with an annual net return of close to AUD$180,000.

For a rough comparison, total cost per head per day in a feedlot is around Rp50,000 for a gain of say 1.4 kg per day, an increase in value of Rp70,000 per head per day. But this margin does not take into account that the steer is imported for CIF Rp59,000+ per kg and sold for a lower figure of Rp52,000 per kg (today’s rates). This means that the last 200kg of weight gain in the feedlot has to be so profitable that it compensates for the initial loss of buying a feeder at 300kg for Rp59k then selling the finished animal for Rp52k per kg.

The total area planted to palm oil plantations in Indonesia is estimated at 14.6 million hectares with 70% of this area in the island of Sumatra (10 million ha.) and 30% in Kalimantan.

If live cattle had access to 20% of the plantation area in Sumatra this would represent an area of two million hectares.

Using a stocking density of 1 animal to 5 hectares this would imply that Sumatra could comfortably support 400,000 feeders.

Photo: Cell grazing of feeders under oil palm trees. This mixed group of male and female yearling progeny from imported Australian cows are growing at 600 grams per head per day with a modest level of daily supplement. Cattle spend one day in each cell. Management of feeders with electric fencing is extremely simple compared to breeders.

Photo: This is yesterday’s cell after a single day of grazing. Woody weeds will be spot sprayed in the next few days. These trees are about five years old. The cattle will cycle back to this cell in about 70-90 days time.

Existing feedlot supply chains would be needed to provide for importation, arrival quarantine, veterinary protocols including vaccinations for LSD and FMD and electric fence training before stock can be trucked to plantations. Once the grazing period has concluded the animals could be returned to feedlots where they can undergo a final freshening up process ready to re-join the well-established supply chains to the vast number of domestic abattoirs spread throughout Sumatra and West Java.

While large scale grazing under palms is an option in both Sumatra and Kalimantan, Sumatra is the simplest way to begin as the entry ports and feedlots are already established while returning to the supply chain can be achieved by trucking while the Kalimantan option will require the use of shipping. ESCAS issues can be managed just as they are in feedlots.

There are a range of combinations in which this new mix of grazing and lot feeding business could be structured with potential for Australian exporters and producers to provide the skills required for large scale grazing operations to combine with importers to manage a highly flexible system of supply from both direct imports and oil palm grazing. This Australian cooperation could be as a service provider or as a business partner.

While this modified operational structure obviously represents a major change to the overall business model, it might allow for survival in the short term and possibly lead to an even more productive and profitable business in the medium to long term.

We are producing roughage feed for both dairy and beef cattle derived from corn silage

Hi Ross,

Great article, I worked for NBPOL in PNG managing the cattle under oil palm in West New Britain. Great system. Opportunities for Australia to send live breeders, genetics etc.

I think an aspect often overlooked is that cattle provide risk management for plantations – especially smallholders. If the palms get diseased, impacted by weather or go through the replant cycle the cattle can provide income and make use of waste vegetation -including palms fronds etc.

We used to use PKE in the feedlot diet heavily (definitely too much by any nutritionists standards) but it was cheap and readily available.

Lots of others would know more than me, but I am passionate about the role of livestock in tree crops/plantations.