MLA’s Manager of Market Information Ben Thomas said once beef production slowly starts increasing again, there will be some downward pressure on prices in the Australian cattle market.

The Australian cattle herd is expected to increase in 2017 for the first time in three years, up three percent year-on-year to 26.9 million head, according to Meat & Livestock Australia’s (MLA) 2017 Cattle Industry projections released today.

MLA expects the first six months of the year to continue on the same track as 2016, with tight supplies, strong restocker demand and the subsequent likelihood of a strong young cattle market.

The herd increase is expected to kick in during the second half of 2017, and will start to impact the cattle market as the increase progresses.

“Once beef production slowly starts increasing again, there will be some downward pressure on prices in the Australian cattle market,”

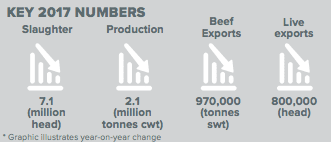

Expectations are for a further 3pc decline in Australian cattle slaughter in 2017, to 7.1 million head.

“While this is a significant fall, it’s not nearly to the same extent as what occurred over the past 12 months when there was an extremely rare 19pc drop,” Mr Thomas said.

“The primary reason for the lower slaughter is the expectation that many producers will be retaining as many cattle as possible to replenish depleted herds; even though the herd is larger than last year, it is still historically low.”

Mr Thomas said despite forecasts for slightly heavier cattle, Australian beef production is also forecast to fall, down 3% to 2.1 million tonnes carcase weight (cwt).

“Again, it’s the first half of the year that is likely to see supplies at their tightest, and production will probably start slowly rebuilding from there.”

Producers in southern Australia – New South Wales and Victoria in particular – are expected to rebuild their herds at a faster rate than their northern counterparts.

“Assuming average rainfall, the southern Australia herd could return to pre-drought levels by 2018,” Mr Thomas said.

“In contrast, the northern Australia herd is not only in a greater deficit, but the otherwise anticipated above-average branding rates in early 2017 will have been inhibited in some regions by the extremely hot conditions during November and December.

“Rebuilding in some regions could be delayed and it seems unlikely that the full Queensland herd will recover to pre-drought levels until 2021.”

Price trends

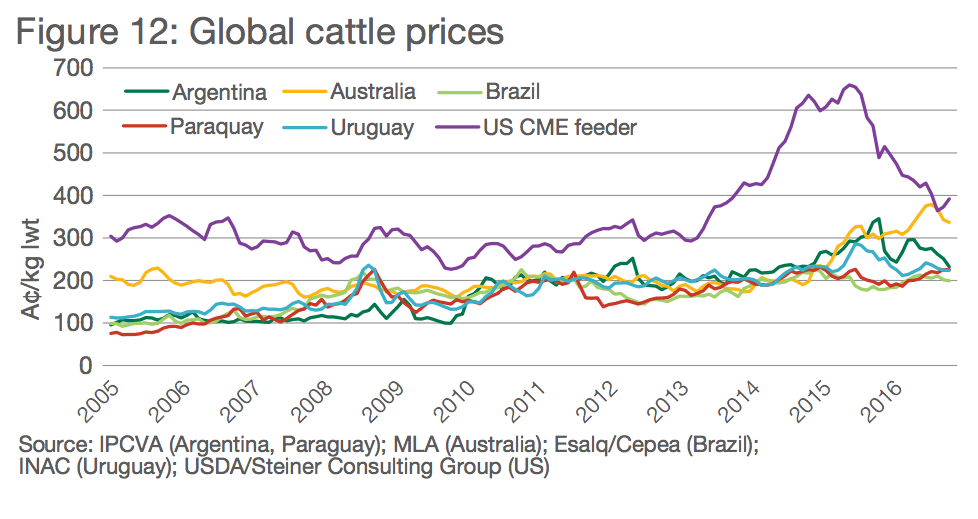

Looking a price trends, MLA says the Australian market is following a similar pattern to what occurred in America, although just 1-2 years behind.

“Once the US market broke through its long-term average trading range, it took just over two years to hit a high, before taking 15 months to lose much of the gains.

“Encouragingly though, the US has stabilised 38pc above the previous level, which potentially indicates a new floor.

“While Australian cattle prices also took two years to reach a peak, only the very early stages of a decline are imminent and a major price easing is likely to await a more balanced cattle market (probably from 2018), as production builds and restocking pressure recedes.

“Hypothetically, if Australia does follow the same pattern as what occurred in the US, and taking into account other factors, like global production and cattle/beef price forecasts, the Australian cattle market could see a 20-40pc decline from the peak, yet settle at a similar magnitude above the 10-year average.”

Projections for cattle on feed

Mr Thomas said the number of cattle on feed is forecast to remain constrained by the still very high feeder cattle prices.

“While entry cattle prices remain dear, solace comes from cheaper Australian feed grain prices and, under this scenario, forecasts are for cattle to stay on feed for 10% to 30% longer than what otherwise would have been the case,” Mr Thomas said.

“The overall outcome is the expectation for numbers on feed to range from 700,000 to 750,000 head per quarter, and turn off of just over 2.5 million head, which is 35% of total adult slaughter.”

69pc of beef production to be exported

Australian beef and veal exports are likely to correlate with the lower beef production and are estimated to ease a further 5% this year to 970,000 tonnes shipped weight (swt), meaning 69% of Australian production will be destined for international markets.

Mr Thomas said live exports would also continue to be challenged by the smaller pool of cattle, especially in the north, along with resistance from some markets at current price levels and continued uncertainty around import policies.

“For 2017, live exports are forecast to be 800,000 head, down a further 24% on top of the 21pc decline that occurred last year,” Mr Thomas said.

More details from Projections tomorrow

Click here to read the 2017 Cattle Industry Projections update.

Click on the video above this article which outlines MLA’s 2017 Cattle Industry projections.

Source: Meat & Livestock Australia

HAVE YOUR SAY