A month ago, it might still have been excused as a short-term aberration, but it is becoming increasingly difficult to argue against latest retail data that clearly illustrates a growing market share for Woolworths, following its January adoption of Meat Standards Australia at retail.

A month ago, it might still have been excused as a short-term aberration, but it is becoming increasingly difficult to argue against latest retail data that clearly illustrates a growing market share for Woolworths, following its January adoption of Meat Standards Australia at retail.

Woolworths has again picked-up beef market value share at the expense of major rivals, Coles and independent butchers in the latest Neilsen Homescan monthly survey released yesterday.

For the rolling quarter ended April 14, Woolworths held a 32.7 percent share of overall Australian fresh beef sales, up from 32pc a month earlier, and a gradual 2pc rise since December 24, just prior to the high-profile, heavily-publicised launch of Woolies’ MSA adoption at retail on January 9.

Woolworths’ result for beef is its strongest since March last year, when it logged a 33.2pc share.

The company has recently upgraded its evaluation of the impact of MSA on beef sales, moving from ‘high single digit growth’ to ‘double digit growth’ in most recent media comments.

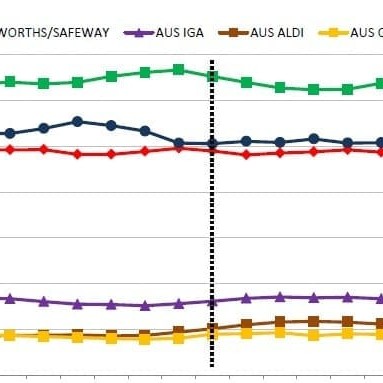

Among the ‘big three’ retailers responsible for more than 82pc of all retail beef sales nationally, Coles and independent butchers both lost ground in the latest April survey.

Independent butchers’ share for the rolling quarter ended April 14 eased a little from 25.5pc to 25.3pc, while Coles – which quite frequently inter-changes with independents in the ‘top three’ rankings throughout a yearly cycle – moved back to third place, moving from 25.2pc to 24.4pc, a significant 0.8pc drop. Coles has lost 1.8pc retail beef share over the past three months.

The monthly trends contrast a little with longer-term beef value performance however.

Woolies’ Moving Annual Total (MAT) to April 14 was 31.7pc, up 0.2pc on a month ago, but still 1pc behind where it sat this time last year. Coles MAT to April was 24.8pc (+1pc on a year ago) and butchers, 25.6pc (-1.2pc). Strong growth by Aldi (+1.3pc to 5.7pc share) and ‘other’ supermarkets appear to account for the deficit among the big three’s combined longer-term results for beef share.

Overall fresh meat sales

In the Neilsen survey’s assessment of overall fresh meat sales (including beef, veal, chicken, pork, lamb and minor proteins like seafood and turkey), Woolworths’ growth in beef is reflected in a similar trend, up 0.5pc to 34.8pc, up a little on this time last year.

In the Neilsen survey’s assessment of overall fresh meat sales (including beef, veal, chicken, pork, lamb and minor proteins like seafood and turkey), Woolworths’ growth in beef is reflected in a similar trend, up 0.5pc to 34.8pc, up a little on this time last year.

Coles and butchery outlets also recorded small losses in overall fresh meat sales over the past two monthly surveys, but Coles has increased share in its latest MAT compared with a year ago.

While it is way too early to pick up signals about shifts in lamb retail sales, following Woolworths' adoption earlier this month of MSA in its lamb offer, Beef Central will monitor future trends with interest.

The overall retail fresh meat category (not just beef) experienced negative value growth in April, mainly driven by decreasing prices, the Neilsen Homescan survey suggested. Beef, chicken and lamb all gained category share compared to the previous rolling quarter, however beef lost share compared to the same period a year ago, while lamb and chicken won share.

Overall, beef’s share of total meat protein sales by value rose 0.5pc to 37.2pc last month, while lower-priced chicken also grew strongly, rising 0.8 pc to 26.4pc. Lamb rose a little (13pc), while pork (9.6pc) and other species remained unchanged. The four week period did however show a small movement towards white meat and away from red meat compared with the annual proportions to the same date.

Prices for competing proteins

Prices remained largely stable compared to the previous rolling quarter figure. Lamb prices were unchanged averaging $12/kg, while beef ($10.20/kg) increased slightly.

Understanding MLA’s retail reporting system

Meat and Livestock Australia three months ago adopted a new monthly retail fresh meat market share analysis, provided by Neilsen Australia Homescan. It replaces the previous Roy Morgan single-source data that has been used for the past ten years.

While there are some variances between the two reporting systems, the relative positions of the three major retail competitors – Coles, independent butchers and Woolworths – remain much the same.

The previous Roy Morgan single-source data provided for the past decade was based on a door-to-door survey that estimated purchasing, based on respondents’ descriptions of how many serves they had bought in the previous seven days.

The new Nielsen Homescan data is extracted from 10,000 households nationwide, each using special bar-code scanning equipment to record all grocery purchases that enter their home.

The Homescan data represents actual purchases rather than stated serves. In MLA’s opinion, this delivers a better estimate of the actual trends in fresh meat expenditure.

As always, switching data providers means some differences in results. MLA has provided some briefing notes on what users might expect to see in contrasts between Roy Morgan to Nielsen reports:

Fresh Meat: The overall market share for each meat type is similar in each survey (+/-5pc)

Beef records a higher share in Nielsen than Roy Morgan (+5.7pc on average), while pork and chicken share decreases. This could be because of beef’s higher average price relative to the other two meat types.

Chicken (-1.7pc) and pork (-2.6pc) have lower value shares in Nielsen. The shares for veal (-0.5pc) and lamb (-0.9pc) are slightly lower in Nielsen.

National channel share, beef and veal: Nielsen data is more stable than Roy Morgan.

Specialty (butchers) is the only channel with a lower beef and veal share in Nielsen (-5.6pc on average). Specialty has a lower share for all meats except chicken. The nature of the specialty shop could result in a lower capture rate in Nielsen and a higher rate in Roy Morgan, MLA says. The exception (chicken) is caused by the fact that fresh chicken specialty shops are now included in the sample.

Coles (+3.2pc) and Woolworths (+1.1pc) have the biggest positive difference in channel share for beef and veal between the old and new systems. IGA (+0.6pc) and Aldi (+0.6pc) have very similar shares across the two data sources.

MLA concludes that overall, there is not a considerable difference in the data trends observed between Nielsen and Roy Morgan. Nielsen offers a more stable trend and the use of value instead of volume data, giving a more ‘realistic picture’ of the market, it says.

To read MLA’s full explanatory notes on the changes to the monthly retail survey, click here