GRINDING beef end-users in the US remain very uncertain about price direction in the next three months.

While the market for imported lean manufacturing beef was steady to modestly higher last week, on the strength of limited offerings from Australia, the overall trend in price this year remains little changed.

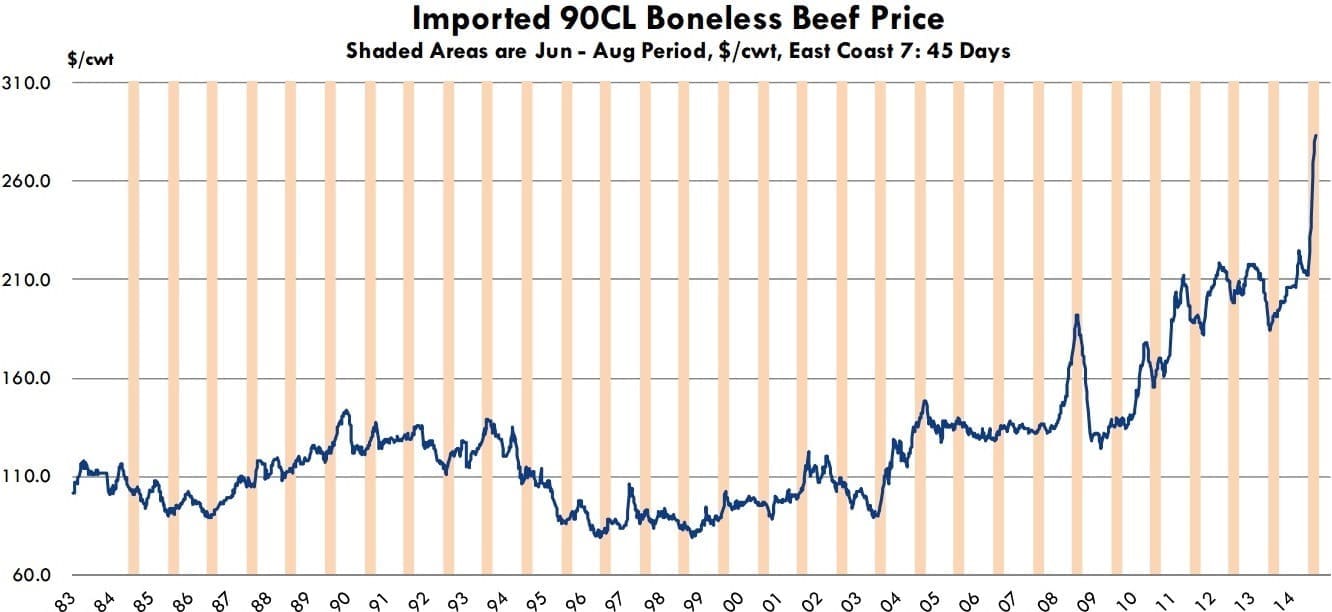

Imported manufacturing beef prices have rocketed higher in the last seven weeks (see chart) and as of late last week, were pegged at around US$2.83/lb on an FOB US East Coast basis, a new all-time record high, the weekly Steiner imported beef report said.

Source: Steiner Consulting. Click on image for a larger view.

Prices have jumped more than US70c/lb since the end of May, a 33pc increase.

While in absolute terms that is the biggest three-month jump on record, it is similar in percentage terms to what was seen in 2008 – although the recent increase has been much faster.

As this graph shows, prices in 2008 started the year at around US$1.35/lb and hit a peak of US$1.92/lb at the end of July, a 40pc premium.

“However, that was a year that saw just as dramatic a deflation of the price bubble, aided by the financial crisis and dramatic shifts in currency values, a general credit squeeze and slumping demand,” Steiner pointed out.

“Some end-users still remember those days well, and some are opting to sit on the sidelines and try to buy product on an as-needed basis, rather than take significant out-front positions. As a result, there are a number of buyers that remain short, and this continues to contribute to the very tight market conditions and high prices,” Steiner said.

Larger buyers that simply could not afford to stay without a position were likely to continue to buy in this market, but Steiner pointed out it did not have visibility regarding those purchases.

“There is a lot more imported beef that is bought direct these days than in years past. As a result, the spot market is relatively limited and with so many short-bought buyers, we think this has contributed to the high prices we are currently observing.”

US fed cattle prices declined sharply last week, in part because the cutbacks in US slaughter during July have started to back-up some cattle in feedlots.

The October fed cattle contract closed last Thursday at $146.55/cwt, down almost $15/cwt compared to the contract high in late July.

“This is a cautionary signal for many end-users, that taking high-priced positions in this market is a risky game,” Steiner said. “Keep in mind that these are fed cattle futures prices, the price of lean grinding beef in the US market continues to hover near all-time record levels, and we have yet to see any weakness start to develop.”

Indeed, prices for many lean beef cuts are currently near or at all-time record highs, a sign that lean beef remains a precious commodity in the current market.

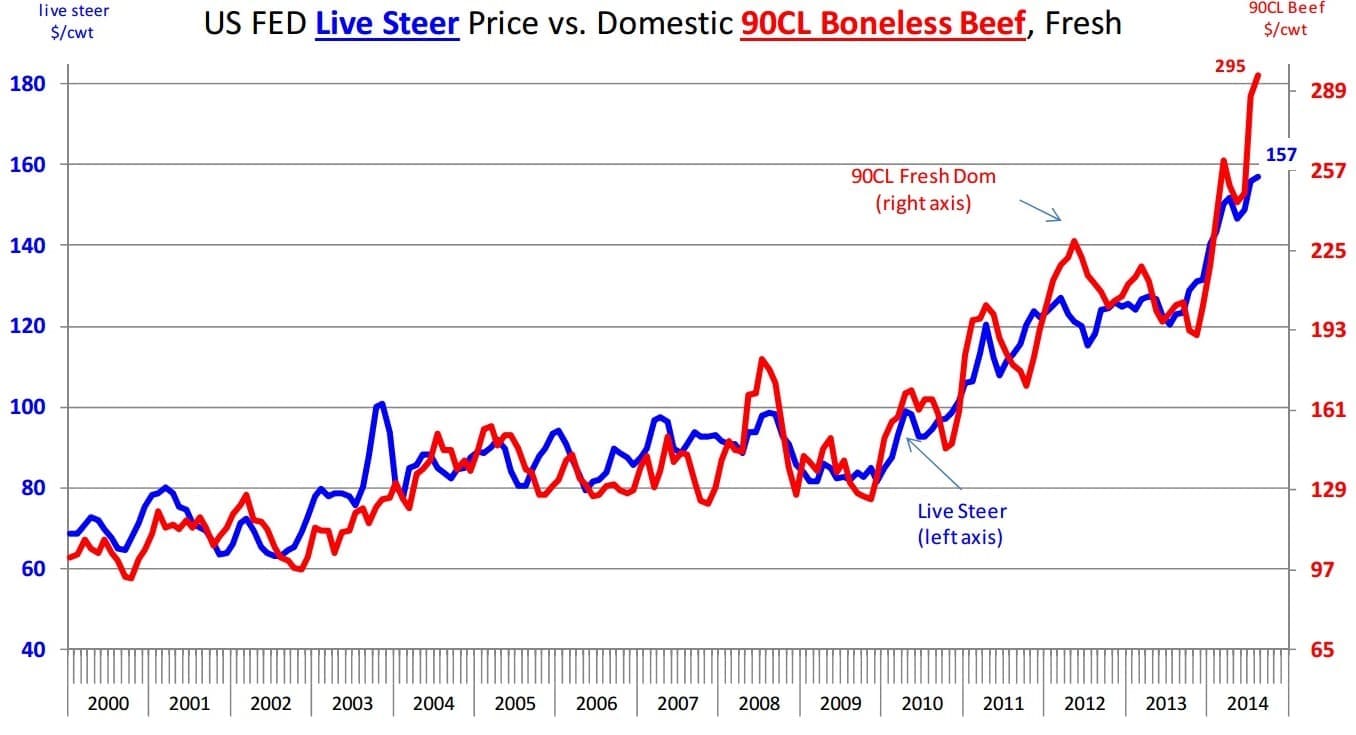

A strong correlation exists between US fed cattle prices and the price of 90CL boneless beef, hence the extreme uncertainty among market participants.

“In recent months, lean beef prices have outpaced the increase in the price of cattle and that continues,” Steiner said.

Source: Steiner Consulting. Click on image for a larger view.

As illustrated in this graph, the gap between lean grinding beef and US fed cattle prices is historically large and history shows this kind of situation does not persist for too long.

“It also remains to be seen whether the recent drop in fed cattle signals a shift in market trend, or if it simply is a correction in what otherwise remains a bull market,” Steiner said.

“We think the latter is more the case as many of the fundamentals in the cattle market remain unchanged. Fed cattle supplies remain limited and we expect the calf crop next year to be steady to slightly below estimated numbers or 2014 – and this year will have the smallest calf crop in about 60 years.”

“Heifer retention has yet to start and it will be a slow process. This means heifer supplies coming to market will be limited for the next 18-24 months as producers slowly add females in the herd. Cow slaughter also is down sharply, with the latest numbers showing cow and bull slaughter running 14pc below year-ago levels.”

Fed cattle slaughter also is down about 7pc on last year.

“All this means these are very uncertain times in the US beef market, and the drop in cattle futures has many end-users hoping for a similar correction in the market for lean and extra lean beef,” Steiner said.

“So far, however, demand continues to outpace available supplies and current prices reflect a very strong market that is significantly under-supplied. This could change in the northern hemisphere autumn, when more cull cows become available and also if fed slaughter picks up.”

“But, with a record low calf crop and herd rebuilding picking up steam, any such increases in supplies will likely prove to be short lived,” Steiner said.