Australia’s beef export industry is riding a tidal wave that has been called the ‘developing Asia era’. It’s the third distinct era in the modern history of beef exports, argues well known industry analyst and former MLA chief economist, Peter Weeks. But how did Australia position itself to catch that wave in the first place and how do we prepare for the next one?

Australia’s beef export industry is riding a tidal wave that has been called the ‘developing Asia era’. It’s the third distinct era in the modern history of beef exports, argues well known industry analyst and former MLA chief economist, Peter Weeks. But how did Australia position itself to catch that wave in the first place and how do we prepare for the next one?

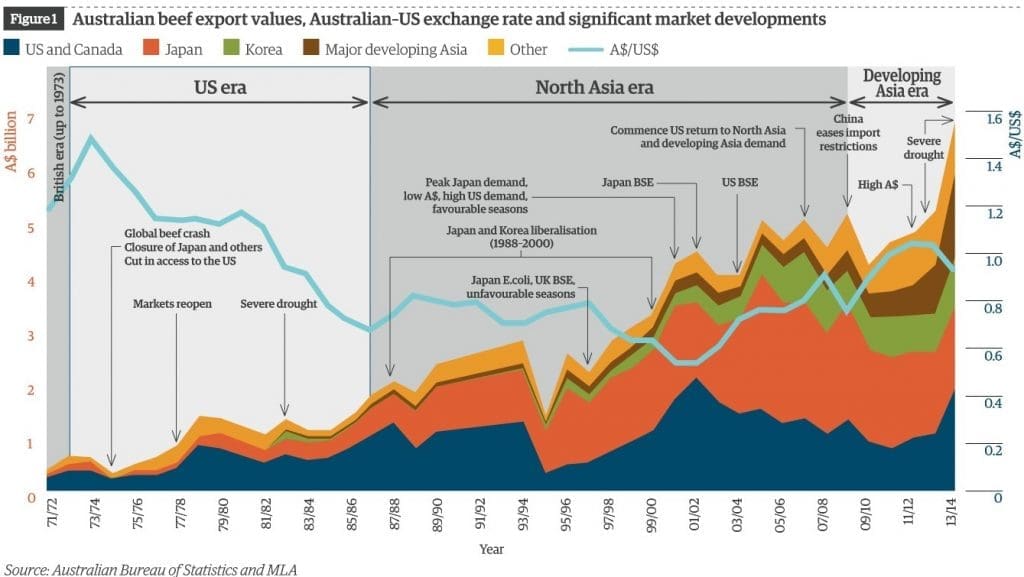

THE history of Australian chilled and frozen beef export industry over the past 50 years can be defined by three distinct eras.

The ‘US era’ saw the take-off of beef exports in the 1970s and 80s. From 1990 to 2010 it was the ‘North Asia era’, and the industry is now in the midst of the ‘Developing Asia era’.

“The beef industry has come a long way since its early days, driven principally by consumer demand growth in Asia, but assisted by trade liberalisation and greater sophistication and integrity throughout the Australian beef supply chain – especially on farm, in processing and in company and industry marketing, Peter Weeks argues.

While the US and Japan remain large and important markets, Australian exports now cover a full array of beef cuts to more than 100 markets – dominated by those in Asia.

The ‘US era’

In the ‘US era’ of the 1970s and 80s, beef exports were relatively simplistic. The majority was manufacturing grade beef for the US fast food sector, which dovetailed neatly with the high quality Australian retail and foodservice markets. Only small amounts of beef went to markets like Japan and Korea, which were governed by small quotas.

The ‘North Asia era’

It all changed quickly in the ‘North Asia era’ when Japan and Korean markets were transformed by trade negotiations and liberalisation.

By 2000, Japan and Korea accounted for almost 50 percent of the value of beef exports, and the US only 34pc. This peaked after US beef was banned in late 2003 during the BSE crisis, reaching 59pc of beef export volume in 2006 and 64pc of value in 2005, Mr Weeks said.

This trend also had an impact on-farm, with producers having to shift to fully grown steers and heifers, off both grass and grain, and to hit target weights faster to lift eating quality. Along came the lotfeeding sector to help meet those demands.

These changes also meant the market became more sophisticated and along with that came major challenges, Mr Weeks said, requiring improved marketing campaigns, grading and quality assurance systems, relationship building, the switch to chilled beef, finding destinations for the non-preferred cuts and overcoming trade disruptions.

This helped set up Australian beef exports to ride the next wave – direct from China and Indonesia – and survive the re-entry of US beef into the Japanese and Korean markets in 2007.

The ‘Developing Asia era’

The ‘Developing Asia era’ arrived more in the form of a tidal wave. Australian beef exports to China and Indonesia rose from 53,000 tonnes in 2006 to 297,000t in 2013, or from 6pc of total exports to 27pc.

It was principally the strength of underlying beef demand growth in these massive population centres, together with the easing of import access restrictions that drove this expansion, Mr Weeks said.

Australia is currently one of the few countries with official access to China and Indonesia and also has the added advantages of a strong image for clean and safe meat, a falling currency relative to these countries, the widest range of beef product on offer and well-resourced industry research, integrity and marketing programs to back it up.

Click on graph for a larger view

What’s in store in the next wave?

So what are some of the factors which may play out during this ongoing evolution of the Australian beef export industry?

Peter Weeks suggests the market features in future may include:

- A shift in beef trade-flows from well-developed North American and North Asian markets to China, South-East Asia and, perhaps, the Middle East

- Increasing positioning of brands in the quality mid-to-upper levels of modern retail and foodservice in these emerging markets

- Shifts in the composition of Australia’s beef trade towards quality lean beef – company-branded, well specified, natural, with quality, safety and integrity assured

- Focus on customers requiring reliability, safety, integrity, traceability and tight specifications (even for manufacturing beef)

- A growing short grain-finished beef export component, as a means of efficiently finishing pasture-grown cattle to specifications

- Domestic consumption will continue to fall, but consumers will be prepared to pay a high price and demand will focus on premium cuts, such as loins.

Peter Weeks’ article will appear in MLA’s June issue of feedback magazine, arriving in MLA members’ mailbags from this week.