GLOBAL economic prospects are weakening, with substantial barriers to trade, tighter financial conditions, diminishing confidence and heightened policy uncertainty projected to have adverse impacts on growth, according to OECD’s latest Economic Outlook.

The Organisation for Economic Co-operation and Development’s June Outlook projects global growth slowing from 3.3 percent in 2024 to 2.9pc in 2025 and again in 2026.

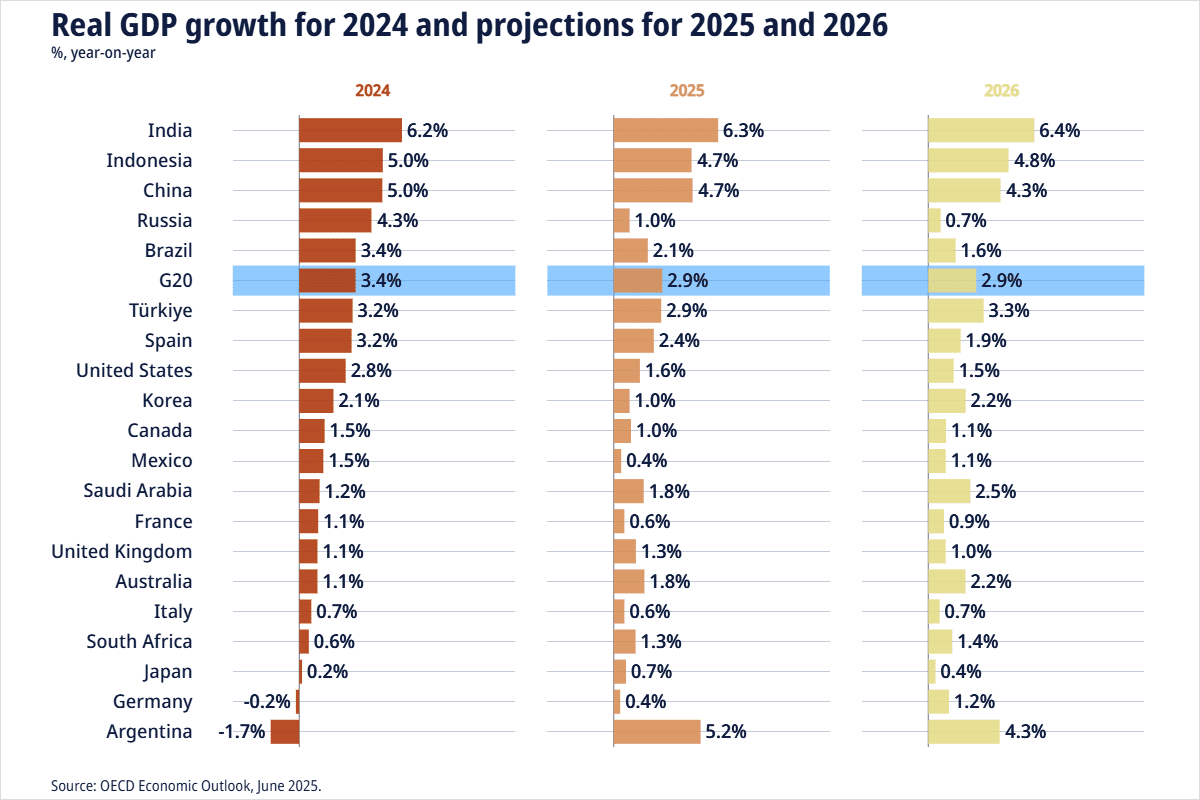

The slowdown is expected to be most concentrated in the United States, Canada, Mexico and China, with smaller downward adjustments in other economies (see graph below).

GDP growth in the United States is projected to decline from 2.8pc in 2024 to 1.6pc this year and 1.5pc next year. In the euro area, growth is projected to strengthen modestly from 0.8pc in 2024 to 1pc in 2025 and 1.2pc in 2026.

China’s growth is projected to moderate from 5pc last year to 4.7pc this year and 4.3pc in 2026.

Towards the bottom of the table, Australia is expected to rise from 1.1pc real GDP growth last year to 1.8pc this year, and slightly better at 2.2pc in 2026.

Click on image for a larger view

Tariffs, inflationary pressures

None of this is good news for beef sales, especially if discretionary spending comes under greater pressure.

Inflationary pressures have resurfaced in some economies, the OECD said in commentary.

Higher trade costs in countries raising tariffs are expected to push inflation up further, although the impact will be partially offset by weaker commodity prices. Annual headline inflation in the G20 economies is collectively expected to moderate from 6.2pc to 3.6pc this year and 3.2pc in 2026.

“The global economy has shifted from a period of resilient growth and declining inflation to a more uncertain path,” OECD secretary-general, Australia’s Mathias Cormann said.

“Our latest economic outlook shows that today’s policy uncertainty is weakening trade and investment, diminishing consumer and business confidence and curbing growth prospects,” Mr Cormann said.

“Governments need to engage with each other to address any issues in the global trading system positively and constructively through dialogue – keeping markets open and preserving the economic benefits of rules-based global trade for competition, innovation, productivity, efficiency and ultimately growth.”

The OECD’s June Outlook highlights a range of risks, starting with the concern that further trade fragmentation, including new tariff hikes and retaliatory actions, could intensify the growth slowdown and trigger significant disruptions in cross-border supply chains.

Inflation could be more persistent than anticipated, especially in economies facing substantially higher trade costs or with tight labour markets, prompting more restrictive monetary policy and weakening growth prospects.

Higher debt payments could increase fiscal pressure on governments worldwide, while tighter financial conditions will pose additional risks for low-income countries. Equity markets have recovered from a recent slump but remain volatile.

On the upside, a reversal of new trade barriers would boost global growth prospects and reduce inflation, the OECD said. A peaceful resolution to Russia’s war of aggression against Ukraine and of ongoing conflicts in the Middle East could also improve confidence and incentives to invest.

Central banks should remain vigilant, given heightened uncertainty and the potential for initial increases in trade costs to push up wage and price pressures more generally, the OECD warned.

“Provided inflation expectations remain well anchored, and trade tensions do not intensify further, policy rate reductions should continue in economies in which inflation is projected to moderate and aggregate demand growth is subdued,” it said.

Faced with multiple spending pressures, governments needed to ensure long-term debt sustainability and maintain the ability to react to future shocks.

“Stronger efforts to contain and reallocate spending and optimise revenues, set within credible medium-term country-specific adjustment paths, will be important for debt burdens to remain manageable and to conserve the fiscal space required to address longer-term spending challenges,” the body warned.

Significant pressures on trade, geopolitical uncertainty and modest growth prospects reinforced the need for ambitious structural policy reforms that strengthen living standards and promote economic competitiveness. A strong focus should be placed on policies to reinvigorate business investment, innovation and productivity.

“Investment has been in decline since the global financial crisis and that has been holding back growth,” OECD chief economist Álvaro Santos Pereira said.

“Greater investment in the digital and knowledge-based economy is a positive development, but public investment remains stagnant and housing investment is failing to keep up with demand. A bold policy reform agenda to boost investment can build a stronger global economy for the 21st century.”

Source: OECD

HAVE YOUR SAY