Flat domestic US consumer demand and larger export offerings out of New Zealand saw imported grinding beef business continue at a slow pace in the US last week.

Flat domestic US consumer demand and larger export offerings out of New Zealand saw imported grinding beef business continue at a slow pace in the US last week.

Market participants indicated only luke-warm end-user interest for imported beef. Some noted that end-users were pushing imported deliveries out, given the discount of domestic product to delivered imported beef.

Part of the reason was recent high New Zealand cattle slaughter, which for the week ending February 16, reached 71,000 head, 26 percent higher than a year ago.

In its weekly imported beef market report on Friday, Steiner Consulting said lean beef values were about US2c/lb (A4.6c/kg) lower than the previous week, although there were bids from some US importers that were as much as US5c/lb (A11.5c/kg) below those quotes.

“Those bids were passed, but New Zealand packers were seen as quite keen to put more beef on the books for March and April delivery,” the Steiner report said.

Australian manufacturing beef was also modestly lower compared to the levels established the previous week.

“On average, Australian prices are higher than what NZ is willing to take at this time but some market participants think it is only a matter of time before Australian processors start booking product at lower price points,” Steiner said.

Those that have a more bullish view of the market, however, indicated that as weather improves in the US, there should be increased interest and higher prices for imported beef. Late last year there was talk of record highs for grinding beef in the early stages of 2013.

The normal decline in US domestic lean beef supplies coupled with improving seasonal demand should underpin both domestic and imported lean beef values in March and April, they argue.

Is it supply or demand?

Last week’s Steiner report suggested the hot topic of conversation in the US market currently is whether the perceived softness in grinding beef values is due to weak demand, or as a result of supply pressures.

“First off, it’s important to define concepts properly. Demand generally refers to a set of prices and quantities. For a given price, the consumers or end-users are willing to purchase a given quantity.”

“Therefore, simply because prices decline or move up, this does not mean demand has changed. Rather, the consumer/end user is willing to purchase more/less given the change in price or quantity,” the report said.

“A decline in demand would imply that the entire schedule of prices and quantities has shifted. But a change in preferences can also impact demand. For instance if you don't like chicken as much as you used to, you would probably need to see lower prices for chicken to get you to buy the same amount as before. That is a change in demand.”

“For example, the recent issues with horse meat co-mingled with beef in Europe would certainly impact on demand in Europe. Also, lower disposable incomes and lower prices for competing products will tend to shift the entire demand curve.”

Demand weakness evident in US

There appeared to be some demand weakness for the US beef complex at this time, Steiner said on Friday.

Disposable incomes in the US had been negatively impacted. Social security taxes, which were temporarily lowered to 4.2pc in 2011 and 2012, are now back to 6.2pc. Gasoline prices have trended higher, eating away at disposable incomes.

“Fuel demand tends to be somewhat inelastic, because people still have to go to work,” Steiner said.

Lower prices for pork had also impacted beef demand.

“In the case of grinding beef, we’ve seen supplies of both domestic and imported product trend lower recently, but despite that, grinding beef prices are now well below year-ago levels as well -largely due to less expensive fat beef trimmings,” the report said.

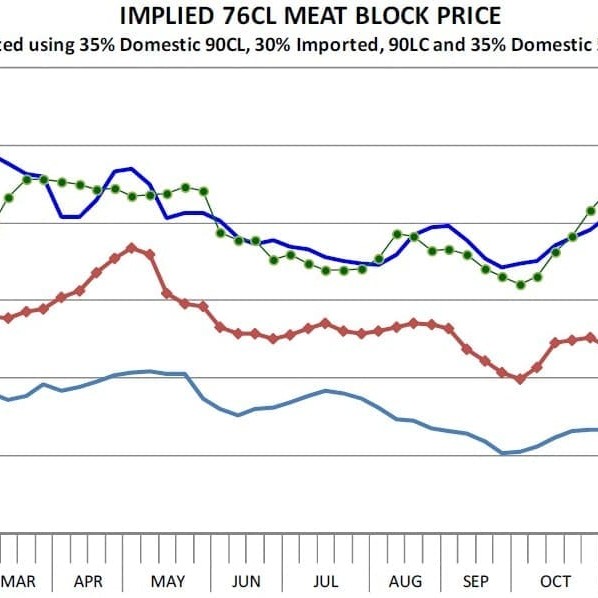

Steiner illustrated this with a typical US beef burger pattie formulation – a 76CL meat block comprising 35pc Domestic 90CL beef, 30pc Imported 90CL, and 35pc Domestic 50CL Fresh.

The calculated cost of that 76CL meat block currently stood at US$1.63/cwt, 7.5pc lower than the same week a year ago (see graph below).

The decline is almost entirely due to the decline in the price of domestic 50CL beef trimmings, which are down 34pc from last year. The price of domestic 90CL lean beef is down 1.5pc but US cow meat supplies are up 2pc while imported beef prices are about steady – even as Australia is shipping significantly less beef in February and also March than it did last year.

DAFF figures for exports to the US so far in February this year suggest total exports are not likely to exceed 15,000t, compared with February last year when exports hit 23,300t, before peaking at almost 27,000t in March.

“The bottom line is that the US market is not struggling with excessive grinding meat supplies at present, rather demand is more of an issue,” the Steiner report said.