Source: Steiner Consulting

A CHASM of Grand Canyon-like proportions has opened up in recent months in comparative pricing between imported Australian 90CL frozen beef and equivalent domestic US chilled beef supply.

In Australian dollar terms, the price differential between Aussie imported grinding beef and equivalent local US supply has never been greater, calculated on Friday in A$ terms at a massive A$2/kg in the wholesale market.

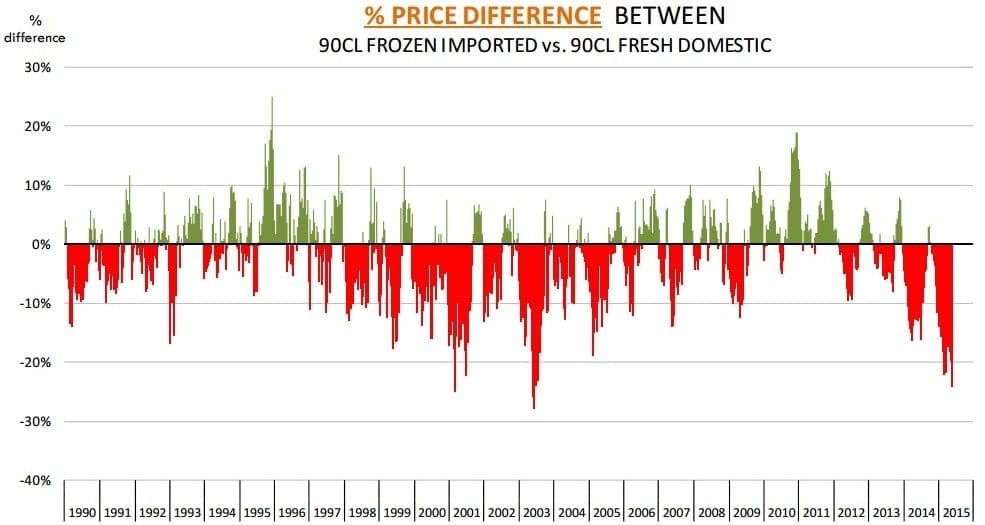

In percentage terms, as the graph here shows, it is not quite at record level yet, but is within sight of the record set in 2003.

The development takes on a more serious note, given the sheer volume of Australian manufacturing beef entering the US market at present. Exports to the US for the month of May again look like going past 40,000 tonnes, compared with 31,000t this time a year earlier – a 29pc rise in 12 months.

Sanger Australia senior meat trader Stuart Hanna says at US70c/lb, the current price differential between Australian and local US beef is wider than it has ever been.

“Multiply that to convert it into kilograms, and overlay the exchange rate, and it represents a price difference in Aussie dollar terms of A$2/kg,” he said.

“It’s a huge number. Traditionally, a US20c/lb differential either way between imported and domestic was a big amount. Over the past couple of years, we’ve seen 40s, 50s and now +US70c/lb gap. There’s never been anything like it – especially as the Aussie dollar has been as low as it is.”

Sanger Australia senior meat trader, Stuart Hanna

There were a range of factors impacting on the price movements, Mr Hanna and other stakeholders have told Beef Central.

“It’s largely about the sheer weight of meat in the pipeline,” he said.

“Australia looks like hitting another 40,000t export month to the US for May (actuals will be published on Beef Central early this week, as part of our regular monthly beef export summary), plus the Kiwi cow-kill is extremely high. There’s been three record weeks of cow-kills in New Zealand, because dairy prices are so flat at present,” Mr Hanna said.

On the plus side, NZ kills are expected to decline from next week, or perhaps the week after. The NZ rate of kill often falls away in quite dramatic fashion around early June.

Mr Hanna said in the end, the big US end-users of Australian frozen manufacturing beef could only use so much frozen product in their ‘blend’ (hamburger pattie manufacturing process).

“Most of the major burger grinders can use a mix of chilled or frozen, but traditionally the maximum amount of frozen that can be used, for practical blending/binding performance reasons, is about 35-40pc. That, in itself, puts a cap on how much frozen imported they can use, especially when supply is so abundant.”

Another factor was that very little Australian frozen 90CL was used in retail applications in the US, with the overwhelming majority used within the food service (burger restaurant) industry.

“We’ve now entered the start of the US summer season, traditionally a big burger consumption/grilling period. All of the players I’m speaking to are reporting that their customer orders haven’t been enormous. A lot of the big end-users already have their stocks and distribution centres filled at this time of the year,” Mr Hanna said.

Another factor was the sheer price of beef in the US at present.

“The fact that grinders are still putting domestic US 90s in there at $US3/lb (the equivalent of A$8.50/kg) makes the final cut-out on a retail beef burger very, very expensive,” he said.

“It’s the same in the quick-service burger restaurant segment. Companies are promoting other proteins like chicken or pork as specials, because beef price is so high.”

Asked what the solution was to narrowing the gap between imported and domestic US prices, Mr Hanna said the supply chain “just had to get through a bit of meat.”

“I think we’ll start to. There’s a fair bit of meat still in cold storage, based on my observations in the market during a visit the week before last. While ever that’s the case, that’s going to limit interest. It’s just going to take a bit of getting through stocks; a lower NZ beef kill, and perhaps for Australia to reduce its shipments a little, which will happen at some point this year.”

“I think that price gap will then start to close. I’d expect pricing for Australian 90CL to again start to improve in the next two to three months. I don’t know that it will get to the heady heights of last year (see Beef Central’s home page 90CL graph) but we will start to see that price gap reduce.”

The A$ dropping another 100 points last week only added a little more fuel to that fire.

Other influences on comparative pricing

Friday’s Steiner Consulting latest weekly imported US beef report highlighted some additional influences on the current price gap in manufacturing beef.

Steiner said imported beef prices were lower once again last week, on moderate offerings from overseas packers and very limited demand from US end-users. Market participants continued to note that at this point, the imported beef market appeared to be ‘well supplied’, especially with lean grinding beef.

“The shift from some large end-users to promoting hamburgers with domestic ground product also has limited demand for imported product and contributed to the large spread between imported and domestic beef,” the report said.

Prices last week for domestic US 90CL boneless beef were around US$2.97/lb, while imported beef (ex-dock, Philadelphia basis) was quoted at around US$2.25/lb, a difference of US72c. This is by far the largest spread between domestic and imported beef ever seen.

“However, it’s important to consider that the relative prices for beef have increased. When looking at the percentage difference in price, then the current situation is not entirely unprecedented,” Steiner said. “Indeed, in the early 2000s, a large spread between domestic and imported lean beef was the norm, not the exception.”

At the graph published as part of this article shows, in 2001 and 2003 there were periods when imported beef traded at a 20pc discount to the price of domestic product – but that was on the basis of much lower c/lb prices than those being seen today. Even during those years, however, imported beef managed to register a small premium to domestic in the final quarter of the year.

COOL effects

Steiner also raised discussion about what effect, if any, there will be on imported/domestic pricing if the US Congress decides to scrap its controversial Country of Origin Labelling law (COOL).

There had been a lot of speculation in recent weeks as to what happens to the spread between domestic and imported beef. The World Trade Organisation recently found that the COOL law unfairly discriminates against meat imports and gives an advantage to domestic producers.

As a result, Canada and Mexico now can impose retaliatory tariffs on a wide range of US products. Many analysts expect that the US Congress will intervene before the tariffs go into effect.

Legislation to repeal COOL has already been passed by the House Agriculture Committee. The legislation will then need to be approved by the entire House and then also by the US Senate before it goes to President Obama for his signature.

It is possible that the law may make its way through the legislature and executive by September but that may be a very aggressive timeline, Steiner suggested.

“Some expect that the repeal of COOL will quickly get retailers to use more imported beef and thus reduce the current spread of domestic to imported,” the report said.

“We are not sure that the process will be as swift as some expect. Retailers are notorious for abiding by their processes and do not take changes in their specification lightly. Some may have a specification for fresh-only in their ground beef packages, and changing to partly frozen product may require a lot of work on their part.”

“A large spread between domestic and imported existed well before COOL went into effect. Retailers also wanted to know that they can count on a consistent supply of product rather than be dependent on the fluctuations in product availability that go with using imported beef.”

Over the years, larger US retailers had also moved away from grinding their own beef to sourcing ground beef directly from packers in the US.

“It is possible that the repeal of COOL may have some marginal impact on grinding beef values as some retailers (likely small ones) may find a way to take advantage of the big spread and use more imported,” Steiner said.

“However, we do think there are structural issues that currently prevent the use of frozen imported beef in the US retail ground beef supply, and they will not change if or when COOL is repealed.”

- MLA on Friday reported that imported beef prices into the US continued to decline last week, with the imported 90CL cow beef indicator US2.5¢ lower, at US217.5¢/lb CIF (down 2.2A¢ to 615.5A¢/kg CIF).