THERE’S been a mild, but nevertheless encouraging recovery in US grinding beef prices for imported Australian product over the past month, but so far the trend has not really been reflected in other international markets.

Other key destinations for grinding meat including Japan, Korea and China remain ‘listless’ and ‘disinterested’ this week, exporter meat sales trading desks told Beef Central yesterday.

The latest weekly quote for imported Australian 90CL frozen cow beef into the US was 603.9c/kg in Aussie dollar terms, another 12.3c up on last week. It’s the first time the figure has crept into the 600s since mid-October last year, but remains a long way from the high 600s-low 700s seen for much of last year.

The latest weekly quote for imported Australian 90CL frozen cow beef into the US was 603.9c/kg in Aussie dollar terms, another 12.3c up on last week. It’s the first time the figure has crept into the 600s since mid-October last year, but remains a long way from the high 600s-low 700s seen for much of last year.

This week’s rise came despite a minor rally in the A$ value against the greenback, trading this morning at US71.98c. In US$ terms, Steiner’s latest imported 90CL quote was US194c/lb, up 3.5c on last week.

Guest columnist Steve Kay discusses some of the reasons behind the current US demand rise in yesterday’s monthly Kay’s Cuts column, accessible here for those that missed it.

In its weekly imported grinding beef report prepared for MLA, Steiner Consulting says imported lean beef prices were higher once again this week, on good end-user interest and limited offerings from Australian and New Zealand suppliers.

Uruguay shipments continue to be limited and volumes from Mexico and Central America also have so far fallen short of the supply that was available a year ago.

Market participants described prices as ‘firm’ and interest from end-users as ‘good’, mostly for lean (90CL) and extra lean (95s) product. Fatty trim prices in the domestic market remain weak and, according to market participants contacted by Steiner, other markets are now much more competitive with the US, even when accounting for exchange rate.

“As a result, we could not establish a market price for 75CL trim, for instance. Supplies of other fat trimmings, such as 80CL and 65CL, continue to be very thin,” Steiner said.

Prices for round cuts for the most part have been weaker this week, largely reflecting softness in the price of domestic cow cuts.

“Availability of cuts from Australia continues to be limited at this point but the trades that are getting done are notably lower than what they were last summer and fall,” Steiner noted.

“There is some hope that in the very near term the value of round cuts from steers and heifers will improve, largely because of limited slaughter. However, the value of round cuts declines in the (northern hemisphere) spring and this continues to be a factor for imported product that will deliver in forward months.”

“Overseas are afraid to over commit due to uncertainty about slaughter levels and, more importantly cattle prices. Domestic end-users recognise the seasonal pattern and thus continue to focus on short-term needs,” Steiner said.

US cow/bull slaughter is expected to remain limited in the near term, likely around 110,000 head per week through mid-April.

“While cow inventories have increased in the last couple of years, the flow of cull cows is not expected to increase until the second half of 2016,” Steiner said. “At this point there is more interest from end users looking to cover needs for late March, April and early May. Some large end-users likely have covered some of their forward positions but there are also plenty of smaller processors/manufacturers who liquidated inventories following the sharp price correction last fall.”

The tendency so far has been to stay short bought but market participants also recognise that:

a) domestic cow supplies are not going to recover in the very near term

b) fed cattle futures may be much lower than a year ago – but so is the value of lean/extra lean beef trimmings. To count on continued weakness into the spring may not be very prudent, Steiner suggested. “A rude reminder of what happens when you are short is the spike in the price of 50CL beef trimmings in January, and

c) supplies of imported beef coming into the US in the first half of 2016 will be much lower than what was seen last year or even in 2014. This remains supportive of the overall lean beef complex and will contribute to a tighter spread between domestic and imported lean.

Australian Slaughter and Exports

MLA is currently forecasting a steep drop in Australian slaughter in 2016 and 2017, driven largely by a dramatic drop in cattle inventories, Steiner noted.

“As US imported beef market participants well know, there is a very strong correlation between Australian slaughter and overall Australian exports. The relationship is not that strong between slaughter and shipments to the US, especially over the long-term because other factors, especially currency and relative prices, will impact the flow of product. Using a rolling three-month average of slaughter and exports to eliminate some of the seasonal impacts, the relationship between Australian slaughter and exports is extremely tight. Sharp declines in slaughter should lead to a notable decline in Australian beef shipments in 2016.

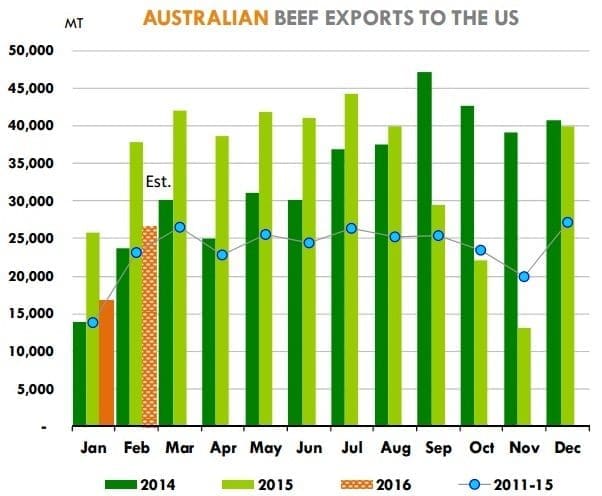

A 15pc decline in Australian slaughter for the period Feb-Apr would imply average monthly slaughter of around 88,000 tonnes. Last year, monthly slaughter during those three months averaged 114,316t and in 2014, those same three months averaged 101,269t.

Likely trends in this year’s exports to US

Much of the increase in Australian exports in 2014 and 2015 was absorbed by the US market.

As Australia’s export volumes this year decline, it would make sense that shipments to the US will also be down, Steiner suggested.

“We still expect the US market to account for 28-32pc of Australian exports during this period. Using our 88,000t average figure, this would imply monthly shipments to the US of around 24,600-28,160t. February monthly exports already are projected at a little over 26,000t, falling in the middle of that range.

“This figure can move around, in part because slaughter may not decline by 15pc. However, bigger declines in slaughter could make it increasingly difficult to maintain the level of shipments that US customer market participants have become accustomed to in the last few years,” Steiner said.