Driven by a powerful set of supply, demand and economic factors, the grinding beef market is gaining momentum as arguably the dominant force in world beef trade in 2012, if not already.

There is a growing view that the frozen manufacturing market is driving global beef prices at present, greatly narrowing the conventional price gap between the market for exports of chilled beef in North Asia and North America and the frozen manufacturing/cheap cuts trades to Russia, the Chinas and the Middle East.

As indicated in Beef Central’s home-page ‘state of the industry’ graphs, Australian 90CL beef exported to the US increased a further A14.7¢/kg, to 425¢/kg FOB last week – 23 percent above the same time last year, and close to 22pc up since trade in June.

As indicated in Beef Central’s home-page ‘state of the industry’ graphs, Australian 90CL beef exported to the US increased a further A14.7¢/kg, to 425¢/kg FOB last week – 23 percent above the same time last year, and close to 22pc up since trade in June.

These are the highest prices seen for lean grinding beef in more than three years.

The all-time record price, in A$ terms, was in September 2001, when the 90CL market hit 481c/kg FAS. In contrast with today, however, the A$ at that time was worth less than US50c, and as a result Australia was consigning close to 400,000 tonnes of beef to the US each year.

Similarly, US-domestically produced grinding beef is also currently hitting all-time record high prices.

The price of fresh domestically-produced 50CL trim set daily and weekly record highs in the past fortnight, reaching US$125.74 per hundredweight (112lb or 51kg) on Wednesday last week. That broke a previous record of $117.82 set on March 24.

Figures like this put 50CL domestic grinding meat in the US at 67pc higher than this time last year. Leaner 90CL domestic trimmings are up more than 20pc over the same period.

Lean imported Australian 90CL trim is typically blended with fattier US grainfed trim to produce the perfect burger patty, at about 75CL.

Driving the grinding beef price boom in the US are several factors:

- High demand from US food service operators as budget-conscious customers trade-down from steak cuts. Burger consumption in the US has gone up considerably since 2009 according to a recent study released by analysts, Technomic. Almost half of US consumers today said they ate a burger at least once a week, compared with 38pc two years ago.

- Expectation that US domestic ground beef supplies will fall substantially as the current drought-driven liquidation of cows draws to a close, leading to a big shortage of slaughter cattle in the US next year. One early estimate put the US beef kill in 2012 at 4.5pc lower than 2011, representing about 1.5 million head.

- Diversion of Australian trim and manufacturing meat into markets other than the US, because of currency movements and higher demand in emerging markets like Russia, as well as established markets like Japan where consumers are also trading-down into cheaper meal options.

MLA market analyst Tim McRae said the current grinding beef price trend was simply a reflection that the global beef trade was recognising that the product would ‘just not be out there’ from early 2012 in the quantities required.

“Some US buyers are finding themselves weighing-up whether to purchase domestic beef now to store until early 2012, or wait and purchase next year, when prices are expected to increase.

This expected increase in prices is based on slowing US cattle slaughter and the good returns for Australian (and other suppliers) beef in competing markets,” Mr McRae said.

“With a few positive signals starting to emerge about the global economy, suddenly the alarm bells are starting to ring that manufacturing meat is likely to be in very short supply next year.”

While it had been markets other than the US that had underpinned Australian meat prices this year because of the effect of the dollar, Mr McRae said higher US competition for Australian grinding beef in 2012, because of the shortage of US domestic cattle caused by drought liquidation, could add ‘significant extra impetus’ behind prices for manufacturing-type cattle in Australia next year.

While it had been markets other than the US that had underpinned Australian meat prices this year because of the effect of the dollar, Mr McRae said higher US competition for Australian grinding beef in 2012, because of the shortage of US domestic cattle caused by drought liquidation, could add ‘significant extra impetus’ behind prices for manufacturing-type cattle in Australia next year.

“From a global perspective, if anything there are probably less cattle available for slaughter now than there was a year ago,” he said.

In Australia, even after the past two years of better seasons, Mr McRae sees ‘pretty strong signs of further herd rebuilding going on,’ suggesting supply of manufacturing cows for processing next season is not likely to be particularly high. That would only put further pressure on cow prices during the traditionally strong April/May/June period next year, which also coincides with a traditionally strong US grinding meat demand period around the Memorial Day holiday.

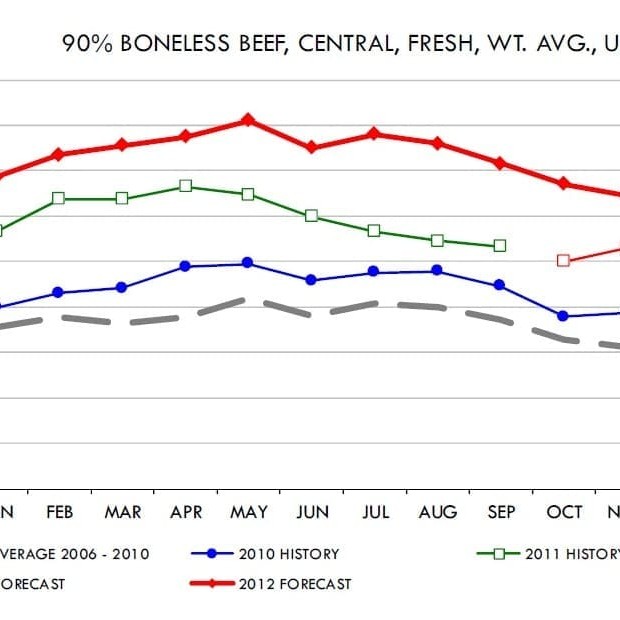

In the graph above, the USDA forecasts 90CL domestic fresh trim to reach US230c/cwt around May next year.

Providing comment recently in the Chicago Mercantile Exchange’s Daily Livestock Report, analyst Len Steiner said normally the US industry tended to look at the Choice cut-out as a key indicator of beef values. But while US packer margins might not be as good as they would currently like, higher prices for beef trimmings had offset this, allowing them to maintain slaughter rates and pay big money for cattle.

“All the talk is that the US consumer may not be willing to pay for high-priced beef, but the data shows cut-out values are nearing the all-time record levels of last year, assisted by trim value,” Mr Steiner said.

US consumers may have shifted towards less expensive beef items such as ground beef, but prices in that complex had escalated, in part due to the absence of imported beef but also because of tight supplies of market-ready cattle.

He said US cow slaughter would fall off towards the end of the year as producers finalised their (northern hemisphere) autumn cow sales. That would further limit supplies of lean grinding beef, making for an even more treacherous market for ground beef going forward.

Drought continues to inflate cow slaughter

While parts of the drought-devastated southern US had received some welcome (but not drought-breaking) rain recently, cow slaughter in the region and nationally remains high and continues to skew the overall weekly US slaughter mix.

Cow slaughter continues at a heavy rate relative to the base cow inventory, with cows and bulls making up as much as 30pc of daily estimated cattle slaughter during November, USDA said in its recent Livestock, Dairy and Poultry Outlook.

This is based on both a seasonal component, in which cow slaughter increases in fall/winter, and a reflection of the tight stocks of hay and other feeds needed to carry cattle through the winter because of the earlier drought.

-

See today's companion story, "US food service shares high price view for grinding beef"