During 2011, the US recorded significant price increase for a number of beef items, driven in part by strong exports to both traditional and new markets.

During 2011, the US recorded significant price increase for a number of beef items, driven in part by strong exports to both traditional and new markets.

Will exports hold up in 2012, and if so what will sustain ever-expanding shipments?

Economist Steve Meyer, writing in Chicago Mercantile Exchange’s Daily Livestock Report yesterday, suggests US currency movements, trade access and other issues will all play a part in US beef export activity this year.

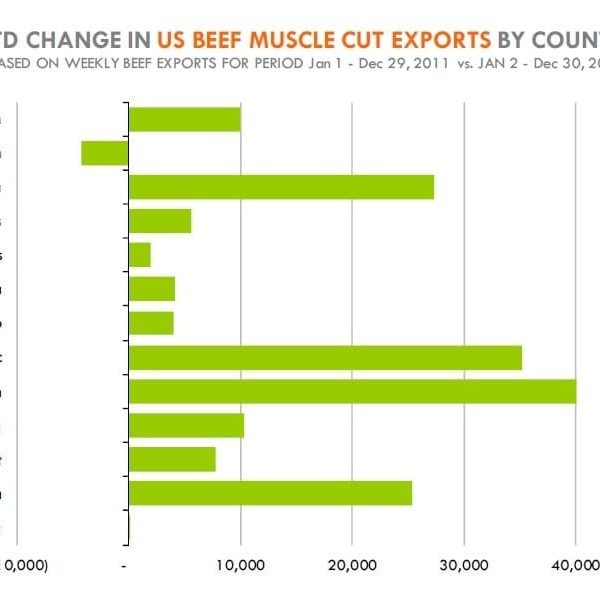

He used the graph published here showing the growth in US beef exports in 2011. The data is based on weekly shipments, product weight basis, through the end of the year. For the 2011 year, exports of US beef muscle cuts (cooked beef and offal not included) rose 27 percent compared to the previous 12 months.

Four countries – Korea, Japan, Canada and Russia – accounted for about 75pc of the overall growth in US beef exports.

“We think the growth in US shipments to these markets is far from reaching saturation point,” Mr Meyer said.

“In the case of South Korea, the Free Trade Agreement (see separate story) as well as limited growth in the country’s domestic production will sustain demand for US beef. Australia is still the top supplier of imported beef in the Korean market, but herd rebuilding in Australia will limit product availability and will likely provide opportunities for further expansion of US beef exports,” he said.

Additionally, current US exports to Korea still remained well below volumes that were shipped prior to the outbreak of BSE in North America.

Japan constitutes an even more important growth market for US beef, Mr Meyer suggested.

“At the moment, the key factor impeding growth in Japan is the requirement that the US ship only beef from cattle that were 21 month or younger at slaughter. There are plenty of rumours that this requirement may be changed to 30 month or younger in 2012, and if that happens, it will provide opportunities for even higher beef exports.”

As with Korea, Australia remained the top supplier of imported beef to Japan, but export supplies will be constrained due to herd rebuilding.

Currency factor

Mr Meyer said the key risk to US beef exports this year remained a sharp appreciation in the US currency. Even as the US$ had gained ground recently, it still remained relatively weak, particularly in comparison with currencies of the US’s major beef markets.

The only scenario Mr Meyer saw for a sharp appreciation in the US currency was if the Euro broke up, leading to an inflow of capital into US dollar denominated assets. However the preponderance of evidence at this point was that the Euro Zone would be able to muddle through its current financial crisis, and further improvements in global economic growth would spur demand for US beef.

It was also worth noting the global beef supply picture, Mr Meyer said. Key world beef exporters, Brazil, Australia, Argentina and Canada were all in herd rebuilding mode. While this will paved the way for higher beef supplies in 2013-2016, the current year would likely continue to see limited global beef supply availability.

“Beef demand in emerging countries will likely continue to increase and, in the short term, the US remains a favoured, and relatively competitive, beef supply source,” he said.