Trouble is brewing in Europe, where Greece and other EU member countries are again showing signs of severe financial stress. Here, Chicago Mercantile Exchange analysts Steve Meyer and Len Steiner provide a summary of the situation, from global agriculture’s perspective.

Agricultural and broader commodity markets were sharply lower on Wednesday as traders reacted negatively to events in Greece and ongoing uncertainty about the future of the European Union.

Agricultural and broader commodity markets were sharply lower on Wednesday as traders reacted negatively to events in Greece and ongoing uncertainty about the future of the European Union.

The issue is not new and it has been percolating for some time. There was some hope in May 2010 that, as Germany and larger EU economies put together a unified front and cobbled together a US$1 trillion package, it would be enough to ease fears in the credit markets.

It worked for a while. However, it is becoming increasingly obvious that the troubles plaguing some of the weaker members of the EU will not go away given the constraints a fixed currency regime places on them.

In the case of Greece, cutbacks in spending have further deteriorated the economic situation, which in turn has created the need for more cutbacks, and so the downward cycle continues.

In CME’s view, the real issue with the EU is cultural and political as much as economic. The ultimate goal of the EU was to create a political union, the citizens of which ‘imagined’ themselves as part of this greater community. Let’s not forget that the nation-state was born in Europe and ultimately it appears that the national bonds are infinitely stronger than bureaucrats in Brussels could foresee. The citizens rioting in the streets of Athens are doing so as Greeks first, rather than members of the EU.

At this point only a few people are talking about a breakup of the EU, but that number is growing. All the countries involved have a lot invested in this project and the costs are incalculable at this time.

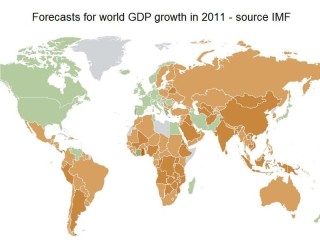

Commodity markets, including agricultural, focus on growth as a broad demand driver. The chart above (click on small image below for a clearer version) was put together in April by the International Monetary Fund and it illustrates their expectations for 2011 GDP growth on a global scale.

At this time, a number of events have taken place that could significantly impact that outlook. In North America, economic growth for 2011 was pegged at 2.8pc for the US and Canada (green represents weak growth, 0-3pc). Q1 growth in the US was 1.84pc while in Canada it was 3.9pc.

Whether one looks at purchasing, investment or labour trends, the fear is that US growth will remain constrained therefore weighing on overall commodity demand.

The broader EU GDP was expected to grow by a meagre 1.8pc, but even that forecast may be dragged down by growing credit problems for countries in the periphery such as Greece, Portugal and Ireland. And as EU GDP deteriorates, more cutbacks may be needed which would further erode economic growth. Much of the orange colouring (represents strong growth, 3-10+pc) in the chart comes from Asian and South American countries.

Countries like Brazil and China have been growth drivers, but even there issues are emerging.

China is on an upward economic trend, but in the short term, there could be bumps in the road.

Much of the Chinese growth is driven by exports to the US and EU and as those economies slow down, so will Chinese growth. Inflation in China has increased sharply and Chinese authorities are struggling to balance growth with financial stability.

Broad commodity markets, and particularly agricultural commodity exports, have been on a bull-run for some time. The drivers for that (expanding populations, industrialisation of developing economies, strained resources) are not going away. In the short term, however, we will likely see a lot of volatility as the global marketplace struggles to find a middle ground between politics, economy and culture.

- • The Australian dollar slipped well below US105c overnight, before recovering to 105.55c this morning, as a direct response to this week’s financial developments in the EU.