IMPORTED grinding beef prices have risen in the US this week, largely in response to very tight supply following declining kills in Australia and New Zealand in December, and normal Christmas holiday seasonal closures.

The market for imported 90CL blended cow beef was quoted on Wednesday at US195-200c/lb, up US10c from the previous week and 21c higher than this time last year.

Prices were set on relatively good demand from US end-users, higher prices for equivalent domestic US product and very limited offerings from overseas suppliers, Steiner’s weekly market report said.

Packers both in Australia and New Zealand appeared content to pass on earlier lower bids, the report suggested.

“However, there are mixed opinions as to whether the current firm stance on the part of overseas packers is sustainable. Some think that this is typical for this time of year, with overseas packers having sold a fair amount of the January supply and generally not in a big hurry to put sales on the books against February production,” this week’s report said.

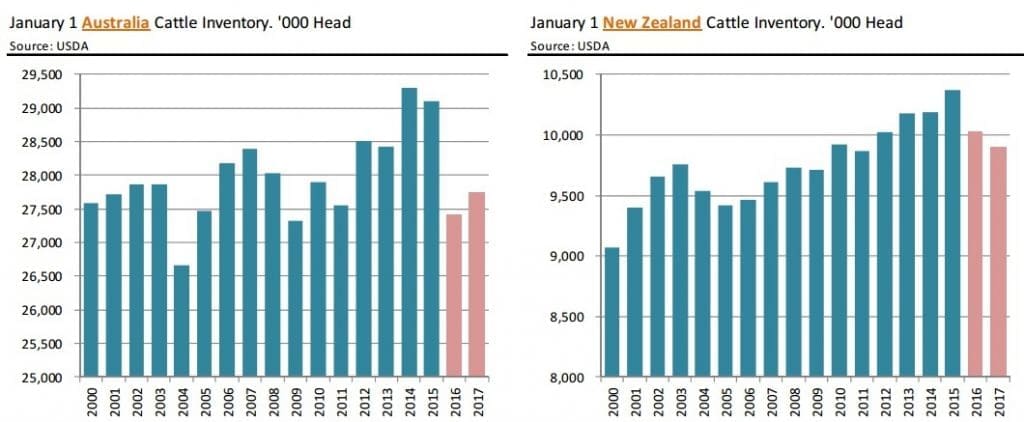

There is broad consensus that the supply of imported 90CL beef is extremely thin, largely due to very limited shipments in the last quarter last year. Australian export statistics for the last three months of 2016 showed total shipments of 90CL beef to the US at 8307 tonnes, down about 10,000t (-54pc) compared with the same period a year earlier, when Australia processing was in overdrive.

“The market at this time is struggling with this shortfall in supply,” Steiner said.

“There is a lot of speculation among market participants as to the supply availability from Australia and NZ in the first half of the year. Some expect supplies of both NZ bull meat and cow meat availability to improve considering the slow start to the year so far.”

NZ kills well down

Through mid-December, NZ bull slaughter was running 19pc below the comparable period the previous year, while total NZ cattle slaughter was down 15.2pc.

“But while it is reasonable to argue for some improvement in slaughter, the NZ supply recovery will depend both on weather conditions (feed availability) and dairy prices. Both those factors so far have contributed to the net reduction in supplies,” Steiner said.

Cattle inventories in NZ as of January are projected to be at the lowest level since 2011, and firm dairy prices, plus above average pastures could continue to limit beef supply availability.

“For now the situation remains uncertain and we think NZ packers put enough meat on the books in December that they can afford to sit on the sidelines and hold firm in their offers,” Steiner said.

While slaughter data out of Australia was limited by holiday closures, the broad expectation was that slaughter will continue to run about 15pc under year-ago levels during 2017. Supplies in the next two to three weeks will likely remain constrained, in part due to the Australia Day holiday on January 26.

“Plants are coming back on line, but market participants have indicated that so far this year, packers appear willing to limit their offerings. Obviously this can change, but for now, this has contributed to the firm tone in the US imported marketplace,” Steiner said.

Premium still exists for imports over domestic US

Prices for imported cuts remain well above US domestic levels this week.

“The price of imported insides, for instance, became competitive relative to domestic fed prices in late December, but we have seen a sharp correction in US domestic prices since then.”

Cap-on insides for USDA Choice beef in the US currently are trading at around US195c/lb, which implies a cap-off equivalent of around US263c/lb compared to imported beef at around US270-275c.

While US cow and bull slaughter has trended downwards over the last two weeks due to the holidays, slaughter for the week ending Dec 24 was still about 30pc larger than the same week a year ago. The lighter slaughter and lack of imported availability has contributed to the strength in domestic grinding beef values recently, Steiner said.

USDA quoted the price of domestic 90CL beef on Tuesday at US201c/lb, still about 5c/lb under the price of imported beef, but quite an improvement from the 190c/lb market in mid-December.

“It is not unusual for domestic US lean grinding beef prices to move higher in January and February, largely because of lower cow slaughter numbers, but the sharp recovery in the last four weeks is more rapid than usual,” Steiner said.

“We think in part this reflects the rapid increase in the overall beef cutout. But the cutout has been slumping the last few days and it remains to be seen if, in the short term, this also puts some downward pressure on the price of lean and extra lean grinding beef.”

Particularly concerning was the sharp decline in the price of both round and chuck cuts, items that normally perform well during this time of year.

“Retail demand so far this year has not been as good as some had hoped, and this may keep grinding beef values on the defensive. So far, imported beef is trading at a premium to domestic and in the short term we think that premium will remain, given the limited shipments from Australia and NZ,” Steiner said.

Brazil beef shipments to the US remained limited, it said. “For now, the volumes are minimal and have no impact on trade, but its an item that bears watching.”