A NUMBER of factors, including mounting competition for Australian beef from China and limited supply out of New Zealand, are contributing to a sharp rise in Australian imported manufacturing beef prices in the United States this month.

As can be seen on the 90CL US imported beef graph on Beef Central’s new home page Industry Dashboard, lean imported manufacturing beef is currently quoted in the US at 650c/kg (Australian dollars) CIF, up almost 50c/kg or more than eight percent in the past four weeks.

Sanger Australia senior meat trader, Stuart Hanna

It’s the highest price, in CIF A$ terms, seen since a brief period in July 2017. Prior to that, prices have not been at this level since October 2015, when the US was suffering considerable beef shortages, due to its own drought over the preceding two years.

Current strong export manufacturing beef prices are supportive of Australia’s ongoing female liquidation due to drought, helping underpin prices paid for female slaughter stock by processors in a congested market environment. Direct consignment quotes published this week are for 440-445c/kg for heavy cows for processing in southern Queensland.

Export meat trader Stuart Hanna from Sanger Australia says impact on the CIF value of Australian lean in the US can be explained by at least four main factors:

- Strong competition from China bidding away Australian product from the US

- Favourable currency movements for Australian exports

- A greater proportion of New Zealand manufacturing product being sold into China instead of the US, leaving a shortfall in US supply, and

- Generally strong beef demand from US consumers.

Mr Hanna said the recent price rise had not been widely anticipated.

“A feature of NZ grinding beef production, which competes directly with Australian supply in international markets, is that it tends to run as regular as clockwork every year,” he said.

“They (US customers) know there is going to be a bull run, and a cow run – and they sat and waited,” he said. “But in the end, what has happened is that the Kiwis – like Australia – are now selling a lot of meat the China – including grinding meat.”

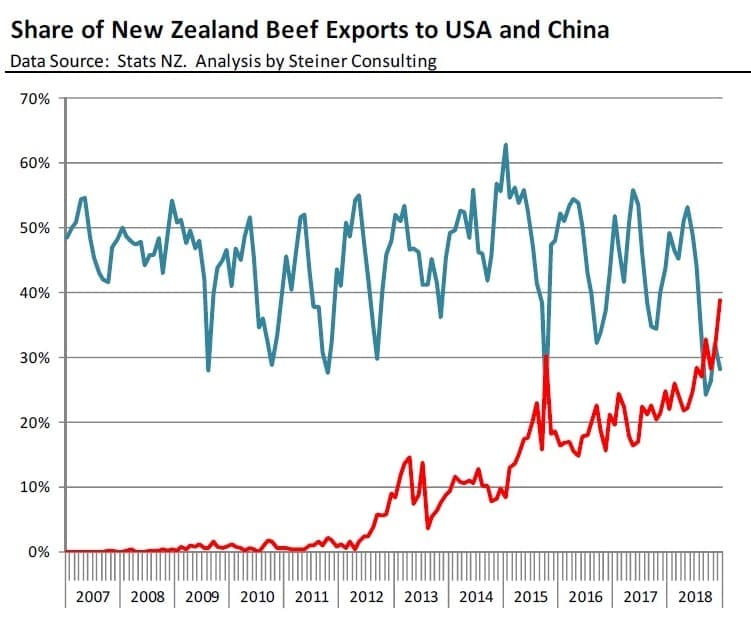

China volume (red line) and US volume (blue line) as a percentage of overall NZ beef exports. Source: Steiner. Click on image to enlarge

The point is well-illustrated in this graph published in the weekly Steiner US imported beef market report, showing China for the first time eclipsing the US as a destination for NZ beef. By nature of its large dairy industry, New Zealand’s beef industry tends to be aligned with manufacturing beef production.

Equally significantly, Australia’s month to date export statistics (to 18 Feb) have ‘other Asia’ (principally China and Hong Kong) tracking well above Japan (Australia’s largest export customer by volume), for what is possibly the first time in history. More on this in our end-of-month exports wrap in ten days’ time.

Mr Hanna said he suspected there had also been a flow-on effect from a couple of other factors:

The impact of the spread of African Swine Fever within China (most recently also detected in Vietnam), which had seen a sharp clamp-down in China on livestock movements, and the constriction of the grey channel, especially for cheap, low-quality Indian buffalo meat.

“All of a sudden that 600,000 to 700,000t a year of Indian buffalo that was arriving in China via the grey channel has dried up. Even if it has only dropped by 10-20pc, it still represents a big shortfall,” he said.

“That’s meant they have had to go and source another cheaper manufacturing beef type item – it could be South America, but in-season, it’s also New Zealand, and Australia.”

“In the end, everything in NZ is HGP-free, so there is no real hindrance to escalating trade into China. All it is to NZ exporters is a label and another code, and they are away.”

Currency factor

Mr Hanna said the current Australian price trend was reflected in A$ Free on Board (FOB) returns that were ‘very good’ at present, but measured in USc/pound CIF (delivered port or coldstore in the US), were not so impressive.

“A nice low dollar is certainly helping us,” he said.

“If we are talking a US210c/lb CIF price at the moment, that’s not an extraordinarily high price, but with a US dollar worth US71c or less, that turns into $6.20/kg in Aussie dollars.”

“In contrast, back in 2014-15, when the US had no cattle after drought, we got to US300c/lb for 90CL manufacturing beef, when the A$ was at parity with the US$.”

“The US will pay what they have to for our manufacturing beef, but they certainly aren’t going to pay US300c/lb in this current price run. But we think there is some upside in the current price cycle, after three weeks of consistent, steady rises.”

“They (US customers) are going to have to keep buying, because the China dynamics aren’t about to change.”

“I think the current level of pricing is at least sustainable. We had a long period below US200c/lb for 90s, and it was cheap. Historically, current pricing is not that much in US$ terms.”

Mr Hanna said while ever domestic fatty trim (50CL) in the US was cheap, it made for a very cheap hamburger, when blended with imported lean trim.

Beef Central asked him whether US customers were showing any sense of concern over beef supply out of Australia later this year, given the serious impact of drought.

“Customers are starting to think a bit more about it, because there are a couple of factors affecting them,” he said.

“I don’t know that they live too much beyond the moment with regard to forward planning for supply. Not a lot of them run huge inventories like the Japanese customers tend to do. But they are starting to realise that that little frozen component that Australia provides, to supplement domestic trim, is important in the overall mix.”

Mr Hanna said demand out of the US for manufacturing and other beef remained ‘pretty good,’ which would also underpin prices.

“Thin-meats, for example – used for fajitas and that sort of menu item – is always very good in the first half of the year, and has remained that way, delivering good returns.”

“General the gut-feel out of America is that their economy is still pretty good, confidence is good and demand is good. The bigger retailers and food service operators are featuring beef again, because they can make a burger pretty affordable, with domestic 50s so cheap. Beef is more affordable, and middle America is a consuming giant with a preference for beef over other proteins, if they can get it at an attractive enough price.”

“They’re the guys that take the pick-up through the drive-through at least once a day.”

Australian exports down, year-on-year

US imported beef market analyst Steiner said this week that limited availability in NZ, improved end-user demand in the domestic market and higher prices for domestic lean grinding beef all contributed to the recent turnaround in imported beef values.

“Imported beef has traded at a premium to fresh domestic beef and that continues to be the case,” Steiner’s weekly report said.

Despite large kills in Australia since the start of the year, imports to the US from Australia and NZ were down a combined 6400t or 20pc compared to the same four-week period a year ago.

“To put this in context, a shortfall of 6400t is the equivalent of 353 truckloads,” Steiner said.

Some market participants had attributed the quick turnaround in prices recently to importers being caught-short and looking to cover positions.

“The latest export data from NZ confirms what we have been hearing from a number of market participants: that China has become a significant competitor to the US in New Zealand.

Prior to 2012 New Zealand exports to China were minimal. Between 2012 and 2015 China share increased to around 10pc of NZ exports and in 2015-17, that share was around 20pc. However, in the last three months of 2018 China became an even more important destination for NZ beef and exports there accounted for over a third of all New Zealand beef exports.

In December shipments to China were almost 40pc of NZ’s total.

“This follows a similar pattern we have seen in other markets. At this time China accounts for 55pc of all beef exports in Argentina and Uruguay and China/Hong Kong account for 40pc of all beef exports from Brazil,” Steiner said.

Bull slaughter in New Zealand should fall off sharply by the end of February, Steiner said, and and with more product going to China and directly to soma large US end-users, this this could lead to a sharp contraction in lean and extra lean supply availability in the US.

While the jump in slaughter bolstered Australian beef exports in January, volume of beef shipped to the US market was relatively small.

“Rather, the bulk of the increase went into the Chinese market,” Steiner said. “Beef exports to the US in January were 13,600t, 7pc higher than a year ago, while exports to China were 12,100t, 53pc higher than a year ago.

Increasing beef supplies in Australia and the seasonal increase in cow slaughter in NZ would support the rationale for shorting imported beef prices in the US, Steiner said. However this had become an increasingly risky strategy for US traders, as China was absorbing almost all of the increase in Australian and NZ supplies.