Rabo’s Kansas based US cattle and beef analyst Lance Zimmermann

AUSTRALIA’S beef export opportunity to the United States in coming years would be more like a ‘slow-moving storm,’ rather than a ‘tsunami,’ a leading US beef industry analyst told a Beef 2024 breakfast audience last week.

Rabobank’s Kansas-based US beef and cattle analyst Lance Zimmermann told a packed room in Rockhampton that the weather analogy might suggest that to a ‘slow moving storm’ might be kinder, and less impactful.

“But they dump massive amounts of rainfall on an area, and have sustained winds that people have to put up with, as well as the flooding and chaos afterwards,” he said.

Promise of a ‘wildly higher beef market’

Mr Zimmerman acknowledged that there had been a lot of discussion about the promise of a ‘wildly higher beef market’ coming in the global space, implied largely on the contraction happening in the US beef industry.

“What I can tell you is that the market is going to be strong, and I think we are in a situation where the market will find more and more support as we see tighter and tighter domestic US beef supplies due to the US herd contraction.

“But it’s going to be better being a slow-burning process, rather than a moonshot, across the global marketplace, as we see continual decline in the US cow herd – leaning into US beef production numbers and impacting US domestic and export beef trade volumes.”

“Ultimately it will lead to a decline in global beef supplies.”

Mr Zimmermann said there was going to be a need for patience, as the impact of US herd decline unfolded.

The moves were likely to come slower than what a lot of folks were talking about, he said. Cattle cycles tended to move in years – not months or weeks.

“As we talk about herd decline, rebuilding and all the infrastructure that’s built around the US beef industry, those changes happen over long time horizons,” he said.

“In the aftermath of a ‘slow moving storm,’ flooding could occur – in this case a large amount of animal protein on the global market and concern over the cost structure surrounding the beef industry. At the consumer level, of lot of cost has been pushed onto the US consumer.

Backgrounding the size and shape of the US beef industry, Mr Zimmermann said that numbers on feed had remained elevated over the past couple of years of drought, as cattle had been ‘rushed’ through one of three production systems faster and faster.

“But as we go through the remainder of 2024 and certainly the next three years after that, we are going to see significant reductions in the cattle represented in some US production models. That will be the pain-point in our US industry, going forward,” he said.

Smaller cow calf guys

The foundation of the US beef production system was the ‘cow calf guy’, dominated by small players. Ninety five percent of cow-calf operators in the US had less than 200 breeding cows.

“Their cattle operation is a side gig, behind a job or two in town,” Mr Zimmermann said.

But that 95pc of small operators accounted for 55pc of all US beef production.

“So while they are small, in terms of influence within the industry, they are mighty. When we think about rebuilding efforts in the US cow herd, which are still a distant dream, that’s the group we are trying to influence – the small operator.”

So a lot of the discussion around herd rebuilding came back to how the small operator reacts to market signals.

“If you run less than 200 head, you’re not necessarily thinking about profit and loss in the same way as if you are a 500 or 5000 head operation. It becomes less about profitability and pasture availability, and a lot more about cash flow and pasture availability.”

Mr Zimmermann said that sector faced a lot of risks today – weather risk, geo-political risk, demand, profitability, pasture availability, regulation and others.

Drought impact lingers

He said the eight connected Midwest US states from Texas in the south to South Dakota in the north represented more than half the US cow-herd.

“If you want to know where drought matters in terms of rebuilding efforts, this area is it. In 2022, more than 65pc of the nation’s cow herd was in some stage of drought. It’s gotten better today, but there are still lots of areas that are abnormally dry or in moderate drought,” he said.

“There’s topsoil moisture, but not much beneath it – it’s not good enough to motivate these smaller producers to start rebuilding their herds today,” he said.

“There’s still considerable volatility in those climate patterns, and weather risk is still very much on US producers’ minds.”

Big rally in cattle prices

There had already been a big rally in US cattle prices for fat cattle, feeders and calves, with prices up about 60pc from the 2020 lows, to where they averaged in 2023, Mr Zimmermann said. But corn prices over the same cycle are up 70pc, fuel prices up about the same, and interest rates up 130pc.

“So a lot of the price rally that US cattle producers experienced over the last three years did very little to incentivise the herd rebuild,” he said.

Click on graphs for a larger view

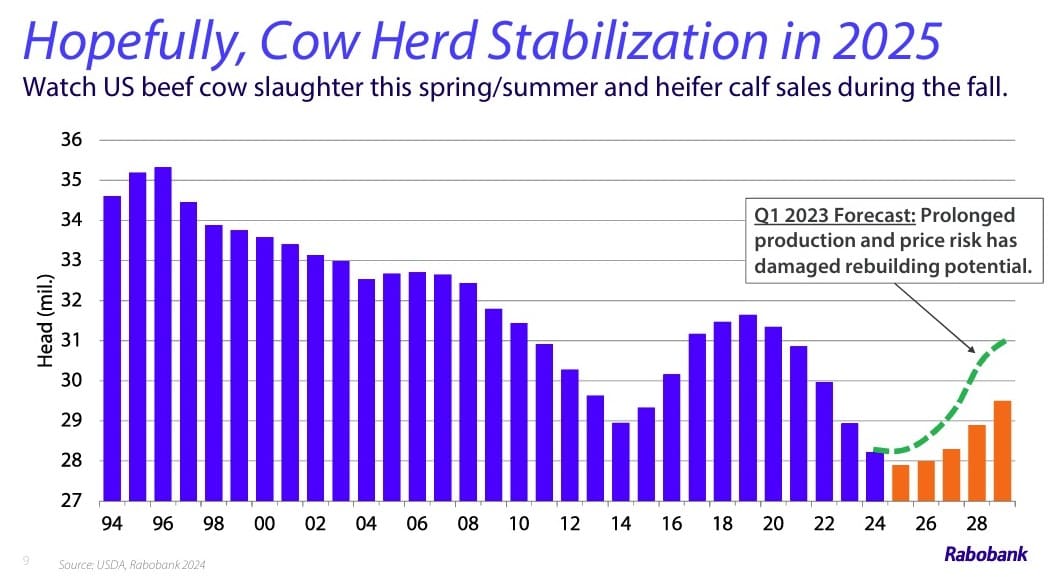

The graph published here is Rabo’s US cow herd forecast out to 2029. The green dashed line is the original projection made 15 months ago, with the orange bars are the current forecast. It shows how the headwinds faced by the US industry have slowed recovery and rebuilding potential.

“Looking at the US producer today, the sentiments in the countryside are pretty sour,” Mr Zimmermann said. “They have dealt over the last five years with record price volatility, record climate volatility, increased regulation and generational transfer.”

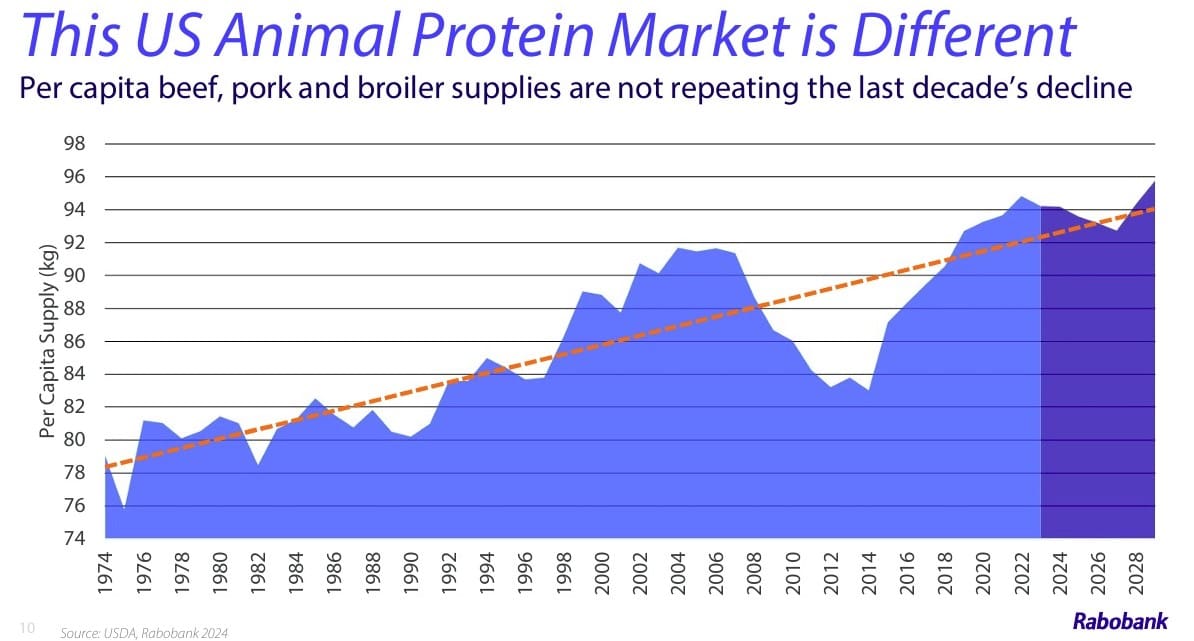

One of the reasons why future US beef prices would not be a ‘moonshot higher’ going forward was competing proteins, he said. As this graph shows, per capita US consumption of beef, pork and poultry was record high last year (95.5kg per person).

“It’s now trending lower (darker blue section), but nothing like the magnitude we saw in 2013-2015,” he said.

Not only did the US have massive drought, but there were virus outbreaks in pork and poultry. Per capita consumption of meat protein then was as low as its been since the early 1990s. But that’s been rebuilt aggressively – there was now a lot more competition in the US animal protein marketplace.

US consumers changing

Mr Zimmermann highlighted demand headwinds for beef, saying consumer confidence ‘reigned supreme.’

He said there were two things to watch in terms of demand: consumer income and consumer confidence – not just their income growth, but buying power. That was a chief concern in the US economy right now.

“The second part is how they feel about the economy (domestically and globally). Any little shock to their confidence is going to spill over into protein markets. But the good news is, first quarter beef demand in the US is going exceptionally well – the second highest recorded in 30 years.

“The consumer today is saying, hey – beef is expensive, but it’s still worth it. That’s an important consideration for all in the global beef industry.

Trade implications

The result of the next phase in the US beef production cycle meant the US would be in a state of imbalance, Mr Zimmermann said.

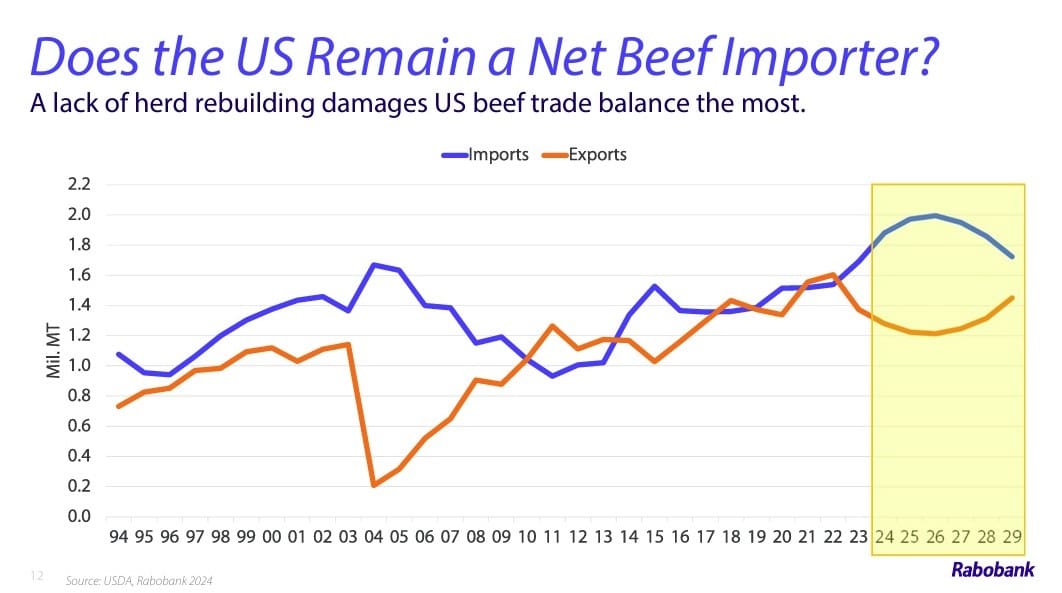

“We’re not going to have near the volume of grinding beef available to us, from a 90CL lean perspective. In the forecast captured in the graph above, our expectation is that the US is going to have to lean harder into imports over the next five years,” he said.

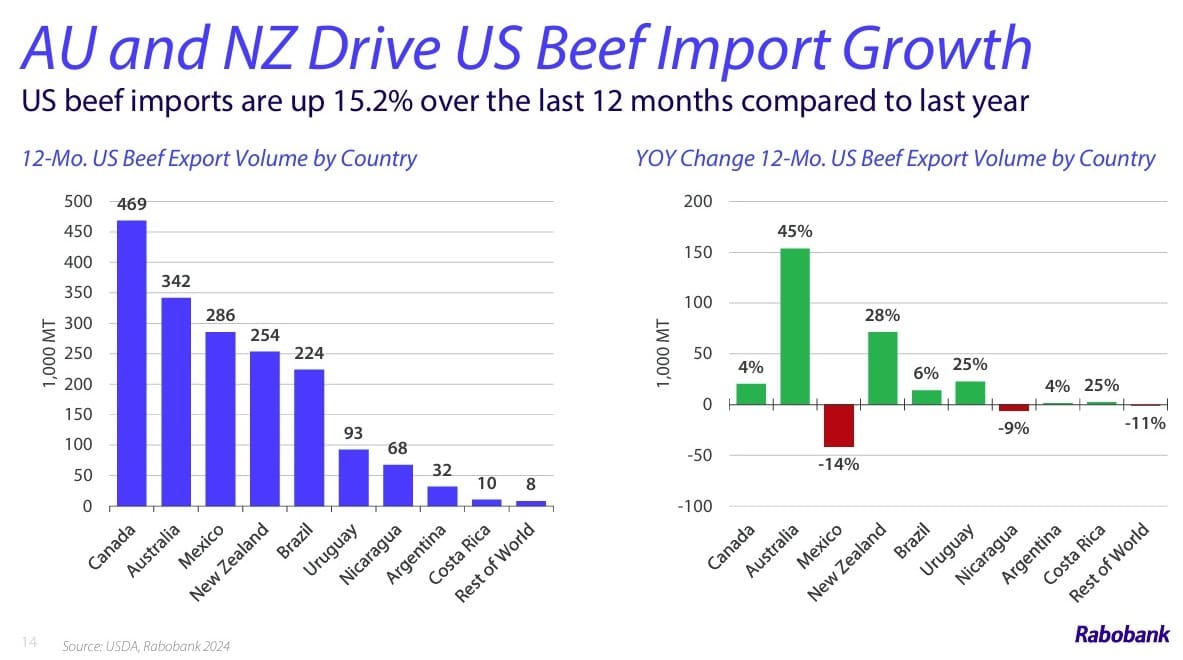

Last year, US beef imports were up 11pc by volume, and 2024 is likely to add another 9pc on that.

Significantly for Australia, US beef exports are also in decline. Last year exports were down 14pc year-on-year, with another 7-9pc pullback expected this year.

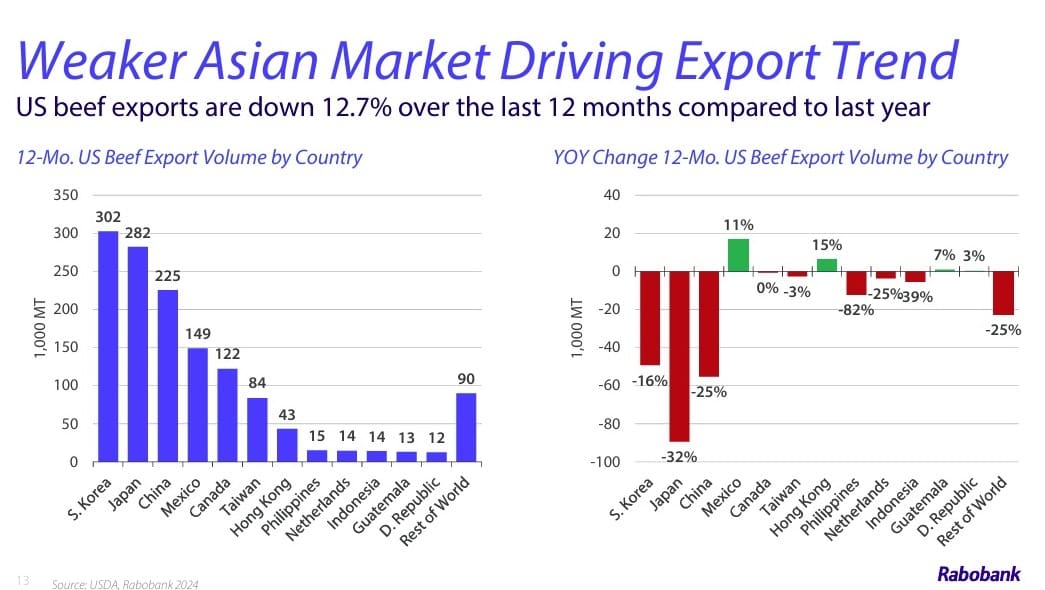

As seen in this graph, the biggest pull-back in US exports has been to its largest markets: Japan, down 32pc on the previous 12 months, China back 25pc and South Korea back 16pc. Australia competes head-on with the US in all three.

In terms of US beef imports (see graph below) the same impact is seen – Australian volume is up 45pc compared with the previous year, with New Zealand up 28pc, Uruguay 25pc and Brazil 6pc.

Brazil is limited in volume under the US’s 65,000t ‘other country’ import quota, meaning it has to pay a 26.5pc tariff after that volume is exhausted (that’s happened this year already, in March).

“The competition in this space is interesting,” Mr Zimmermann said.

“From a 90CL grinding beef perspective, Australia is the giant in the room – the US’s biggest import partner for that product. In the cuts market, Mexico and Canada have taken more of the market for lower marbling score product, as US production declines.

“Mexico is going to be a bigger competitor for Australia in that imported cuts market,” he said.

The US cuts market was built on a chilled (not frozen) product by-and large (perhaps with the exception of some food service use), and Mexico was attractive for that reason, due to geographic proximity.

“Mexican beef exports to the US are double what they were ten years ago,” Mr Zimmermann said.

US cattle and beef prices trending ‘inevitably’ higher

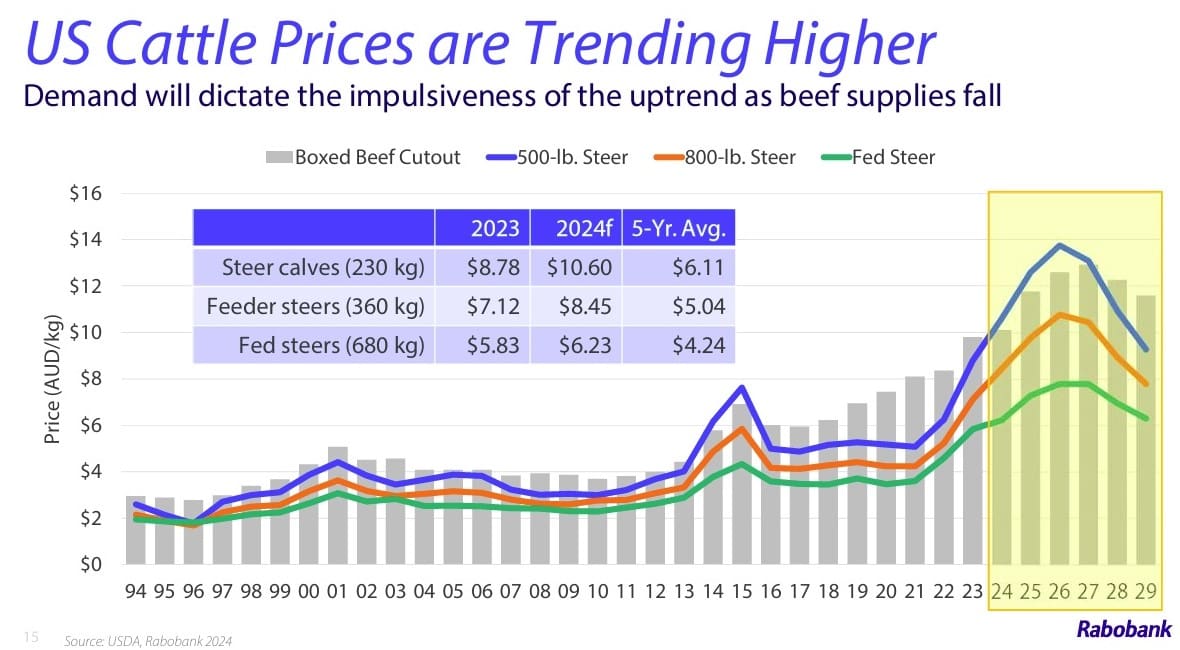

So what are US cattle and beef prices going to look like heading into the next phase of short domestic supply?

“The forecast trend is higher – whether it is calf prices, yearlings finished cattle or boxed beef,” he said, referring to the graph above, “but you’ll notice it is not impulsively higher.”

“We have already priced-in a good chunk of what we expect, and its still supportive, going forward.

“A lot of this is based on a retail consumer price that’s going to trend towards an average of US$9.50/lb, going out to 2026-27 – around $28/kg Australian. Today the average price is around US$7.75/lb.

Questions probe the future

Responding to an audience question about US heifer retention, Mr Zimmermann said some Australians he had spoken to during his visit had appeared ‘somewhat shocked’ to hear that the US has not yet even commenced rebuilding its herd.

“As I look at the fourth quarter last year, we sold more heifers to feedlots as a percentage of the total mix of feeder and calf sales than we did in the same period in 2022,” he said.

“US cattle producers are in the mindset of ‘take the money now, and worry about the rebuild later,’ and that flows right through the system. Females on feed are going to stay elevated through to the end of this year.”

Futures market says: “Prove it to us”

Another question asked what features Australian producers should watch for, as the US cycle changes.

There were two triggers Mr Zimmermann said he was really watching – one price related, the other slaughter trend related.

“When you look at our US live cattle futures market, in relation to live cattle and feedlot cattle prices, right now the futures market is simply telling cattle producers and meat purveyors: Prove it to us.”

“Prove to us that demand is as good as you really think, and prove to us that the (US) cattle aren’t there. It’s phenomenal – it’s shocking all of us. The futures market is just like many of us – it’s impatient, and wants to see the proof of the fundamentals before it prices it in.

“I would tell you than based on current fundamentals that we are forecasting, they don’t have a clue. We are seeing Futures prices for April 2025 (12 months from now) that are below where the cash market traded during April this year.

“Conceivably, that makes no sense – even if we factor-in demand at steady levels, or even discount demand a couple of percentage points, based on the supply decline we expect to see, that futures price should be well above where it traded last month. And it’s not.”

So one thing the Australian industry should watch closely was when the US futures market catches on, pricing in those preferred contracts an appropriate price based on what’s being seen.

The other barometer to watch was US beef cow slaughter, he said.

“Over the past three decades, the US cow culling rate has been pretty consistently around ten percent, drifting as high as 12pc in a calendar year and as low as 8/8.5pc. This year would end around 10.7pc, signalling slight liquidation, and no heifers behind them.

“But when does the cow calf operator really start applying the brakes to cow slaughter, with a culling rate well below 10pc?” Mr Zimmermann asked.

“I think we’ll get down to 10pc as we work to next year, but it wouldn’t shock me if the US industry stays in a stabilisation phase longer than what we are comfortable with.”

An excellent third trigger to watch could be heifer numbers going into US feedlots, as the industry gets to September, October and November.