EASTER is typically a key decision-making point for North Queensland producers in terms of cattle stocking/trading and buying or selling property.

Roger Hill

Independent property valuer and market observer Roger Hill recently became a partner at Preston Rowe Paterson, setting up the valuation company’s first regional office in North Queensland together with Brennan Leggett.

In this week’s property review, Mr Hill reports that 2024 is already a better year than the previous 12 months.

“Lower cattle prices and poor seasonal conditions during 2023 put a check on property market flamboyance,” he said.

Mr Hill identified four macro influences impacting northern Queensland property values for the remainder of this year:

- Season – available grass

- Commodity prices

- Interest rates; and

- Properties for sale

Season

Mr Hill said rainfall in November was certainly welcome with subsequent rain positively received, resulting in prolific grass in many areas.

“Now, the focus is not so much on the usual risk mitigation and decision-making (green date and Easter triggers), but on making the best use of the abundant feed. The opportunity for a forthcoming trade is front of mind for some producers,” he said.

The table below reviews the BOM website data records for which areas around the region had a good start to the wet and how the current wet season compares to the median rainfall records.

| Town | End ’23 rain (mm) | 2024 rain (mm) | Total mm for wet | Median (mm) | % of median |

| Boulia | 22.7 | 157.2 | 179.9 | 215.6 | 83% |

| Winton | 62.2 | 339 | 401.2 | 350.2 | 115% |

| Longreach | 78 | 168.4 | 246.4 | 404.5 | 61% |

| Barcaldine | 244.2 | 158 | 402.2 | 466.3 | 86% |

| Emerald | 215.2 | 160.2 | 375.4 | 496.4 | 76% |

| Clermont | 280 | 175.8 | 455.8 | 629.4 | 72% |

| Trafalgar (CT) | 245.5 | 651.1 | 896.6 | 611 | 147% |

| Georgetown | 254.4 | 1169.8 | 1424.2 | 753.2 | 189% |

| Croydon | 120.2 | 580.6 | 700.8 | 720.2 | 97% |

| Camooweal | 58 | 642.6 | 700.6 | 375.4 | 187% |

| Cloncurry | 49.8 | 546.4 | 596.2 | 500.2 | 119% |

| Richmond | 83.2 | 264.6 | 347.8 | 462.8 | 75% |

Cattle market

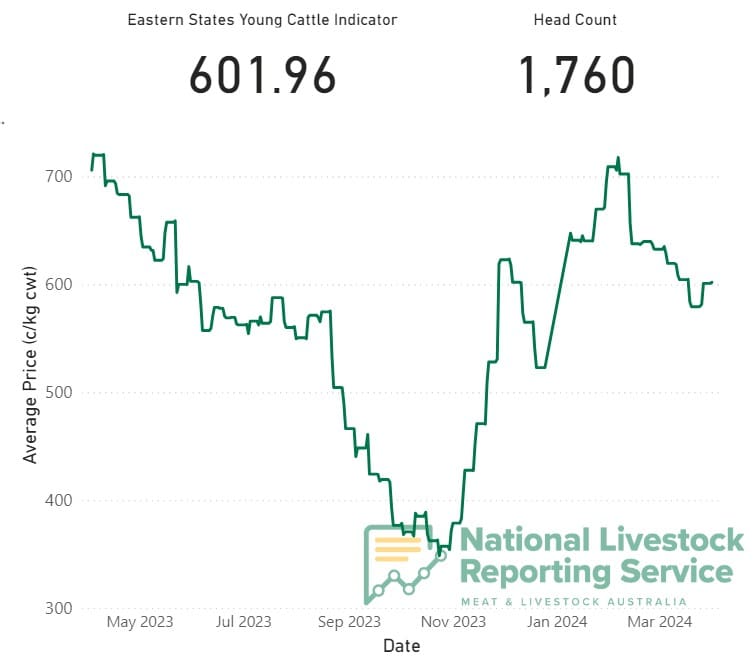

Mr Hill said it was interesting to look at the cattle market (Eastern States Young Cattle Indicator) over the last 18 months.

- The ECYI peaked in January 2022 at 1154c/kg cwt

- In April 2023, it was around 720c/kg

- In October 2023, it softened to 348c/kg

- In February 2024, it strengthened to 717c/kg

- In March 2024, it dropped to around 600c/kg

He noted the EYCI often softens during the first round of mustering from April to June.

“With the rainfall and the volume of grass this year, cattle may be held back again. Then, as the dry season continues and supply reduces towards Christmas, the cattle market typically increases.”

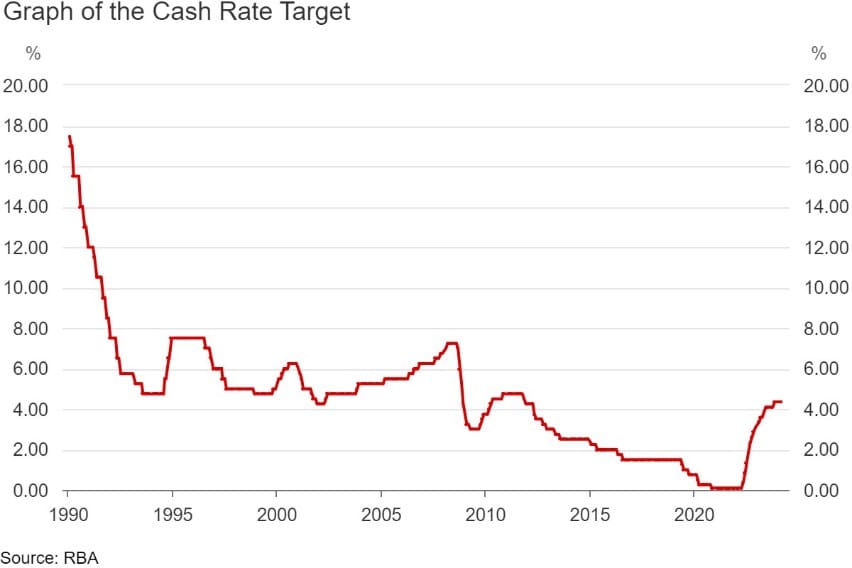

Interest Rates

The Reserve Bank has held the cash rate at 4.35 percent since November 2023.

Last month, the Reserve Bank board stated, “the monetary policy decision indicates a highly uncertain outlook, however inflation appears to be moderating.”

Mr Hill believes this may send a signal of confidence to the rural property market the interest rate cycle may be near its peak.

“While conducting valuation inspections, producers are commenting on the impacts of interest rate changes.”

He said the cost of capital was biting into producers’ budgets.

“One percent for each $1 million of debt is $10,000 per year in servicing, and the comments I am hearing are that that if a borrower owes $10 million, then that one percent represents $100,000 – that is a fair chunk of cattle sales.”

Mr Hill said 20 years ago, the cash rate in February 2004 was 5.25pc, which then softened to 2.5pc a decade later in February 2014.

“A substantial driver in recent rural property market value rises was the low interest rate environment from around 2010 to around 2020,” he said.

“Given that property owners are looking for cost savings at the current rate, they are certainly hoping to see the top of the interest rate cycle shortly, and do not want to endure further increases in the cost of capital.”

Properties for sale

Mr Hill reported that in North Queensland, over the last five to ten years, there had been only a steady number of rural properties offered to the market at any one time.

“This limited supply, coupled with high demand, certainly was another factor that drove value increases in the recent property cycle.”

Earlier this year, he estimated the 2024 property cycle would see an increase in properties (around 25) offered to the market.

“That is not an alarming amount – that is a healthy amount of sales activity compared to last year’s 17 or 18 transactions.”

“When there are too many sales across the region (above 30), the perception of asset liquidity affects decision making, and people do tend to start taking bigger property trading risks at that point,” he said.

In the current market, Mr Hill said rural properties should change hands within a six-month marketing window, if they were priced correctly and the vendors listen to the market for guidance.

“Whether they successfully transact depends on vendor expectations. A property that is priced too high will be a stumbling point.”

Mr Hill said there had been some instances where substantial prices have been achieved by vendors who have waited and stood their ground.

“Typically, there are situations where a purchaser has paid the premium knowing that it is a strong price for their own reasons. Some of those reasons have been lack of available country, or the potential for a renewable project.”

Mr Hill is confident that the broader market is wise enough to know if those prices reflect market value or not.

With the anticipated increase in country coming onto the market, he believes there will be some outcomes this year in the buyer’s favour.

“Vendors will need to be wise as to their pricing decisions or take a risk at holding out for a higher price. Right now, landholders appear to be reasonable in their property pricing and few are asking for an increase on the existing 2022 to 2023 parameters.”

In the short term, he said it was important that people carry out proper due diligence.

As a rough secondary guide, Mr Hill provided the following beast area values ($/AE) currently in the marketplace:

- Charters Towers – $3500/AE to $5500/AE and in one or two instances, as high as $10,000/AE

- Georgetown – $2750 to $3700/AE

- Croydon – No sales for some years in the district. Last sales were in the $2000 to $2200/AE bracket

- Mitchell grass downs – Wide range from $4400/AE with a regular $5000 to $6000/AE and occasionally higher

- Desert uplands – $3500 through to $10,000/AE which appears to be wide, yet there is a wide scope of country types and standard of development across the bioregion.

Wagyu cattle on Barragunda, near Hughenden

NQ properties currently listed for sale

Here’s a quick summary of North Queensland grazing properties currently listed for sale:

- Adjoining grazing and irrigation blocks, the 830ha Billabong and the 547ha Keshvale, are located near Woodstock, 50km south of Townsville. They are being offered for sale separately or as a whole by expressions of interest closing on April 23.

- The 9269ha Barragunda, 67km south of Hughenden, is open downs breeding, backgrounding or fattening country which is enjoying an excellent start to the season. It will be auctioned bare on April 18.

- The 19,248ha Marathon, 40km east of Richmond and 70km west of Hughenden, offers breeding, backgrounding and finishing with direct access to the Flinders River. The walk-in walk-out sale includes around 2000 head of cattle.

- Offers over $18.6m are being sought for the well-watered breeding and backgrounding enterprise Burlington Station, 50km north of Mt Surprise. The 46,000ha holding is being offered on a WIWO basis including 3200 females, 100 bulls and between 1000 and 1200 weaners.

- The 9962ha Rocky Springs is a freehold block 15km from Mount Surprise. Abundantly watered, the breeding facility offers potential for backgrounding and finishing of dry cattle. The sale includes 1400 breeders and calves and 500 dry cattle.