INFORMED decisions require careful analysis, and careful analysis requires accurate data.

It is no different when it comes to buying property, as good data takes away the sentiment and brings the process back to a clear business decision.

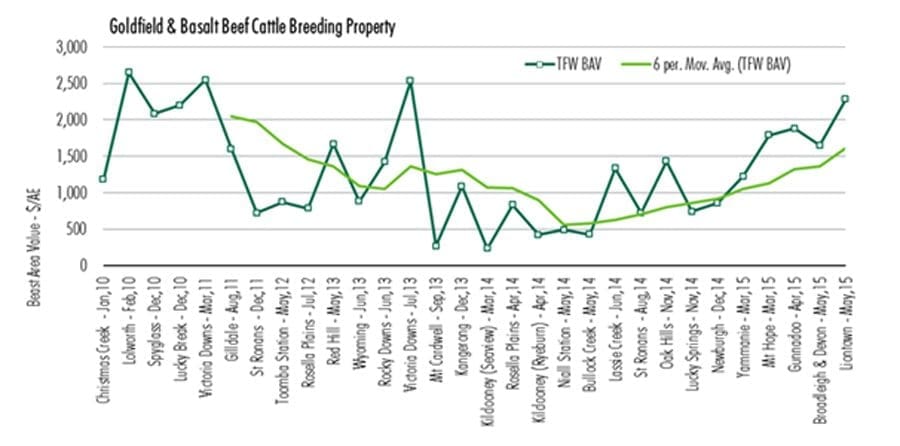

Over the last five years, experienced and widely respected rural land valuer Peter Honnef has analysed a number of beef cattle breeding property transactions in a specific sub-market area in the Goldfield and Basalt country, in the Charters Towers Region of North Queensland.

Over the last five years, experienced and widely respected rural land valuer Peter Honnef has analysed a number of beef cattle breeding property transactions in a specific sub-market area in the Goldfield and Basalt country, in the Charters Towers Region of North Queensland.

Mr Honnef, CBRE’s director of agribusiness valuations, said he chose the area because it was a good market indicator of beef property sentiment. In addition, it provided a good cross-section of operations from breeding through to backgrounding and growing.

By comparison, other areas hadn’t moved at all, he said.

“Queensland’s downs country, where it is all black soil and Mitchell/Flinders grass, is absolutely bare and there has been very little property movement,” Mr Honnef said.

Comparing ‘apples with apples’

In an attempt to value each of the properties equally, he stripped-back the sale price to land content only.

Cattle, plant and equipment value was removed, as was the value of buildings. What was left was a value that is termed TFW – Treated (cleared), Fenced and Watered.

The core principal of valuation, Mr Honnef said, was to compare ‘like with like’, ‘apples with apples’, and ‘oranges with oranges.’

“That gives a pure land price level of value. Then we look at the land on a dollar per beast area basis,” he said.

“The carrying capacity is estimated by the number of adult equivalents a property can carry. When we talk about AE, it is 450kg/beast. Once all those standards are adopted, the figures show a trend-line. Using a moving average, the trend line shows the market (in the nominated area, at least) has bottomed and has been rising since the beginning of this year.”

Click on image for a larger view

The chart published here shows a series of peaks and troughs. Mr Honnef said a number of factors were responsible for the lows, starting with the Global Financial Crisis from 2008 which knocked the confidence out of the industry.

“In 2010, confidence was returning to the beef sector. Then the Federal Government banned live exports to Indonesia and the market crashed. It knocked the wind out of the northern beef property sales sector,” Mr Honnef said.

“The following year the drought started, and in 2012 there was below average rainfall across many parts of Queensland. The situation continued, leading to severe drought conditions and disappearing cash flows. Many people who purchased properties at the peak in 2006-07 were forced into receivership and property prices plummeted.”

And the peaks? Mr Honnef said it was important not to interpret the graph as a ‘trend line chart’ because it is an ‘actual price chart’.

“It reflects property type values, not averages. Sales that show a peak are quality properties, or properties that are close to town, and are valued higher. Not all properties in the same area have the same values because they have different features and characteristics,” he said.

What is interesting is that all the property purchases have been by locals, and that is why Mr Honnef believes this region, at least, is now in a rising market.

“From March onwards, all those properties that had been on the market for a number of years, sold. The market is now meeting vendor’s prices,” he said.

Chart shows change in buyer thinking

Mr Honnef said while foreign investors have paid some record property prices recently, this was not a true indicator of local market sentiment.

“What this chart shows is the change in thinking of northern farming families growing beef. They are now willing to pay above $1000/ beast area for a property in the region analysed. Six months ago, they were paying below $1000/ beast area.”

Mr Honnef said market sentiment changed mid-year when there was a lot of talk about foreign investment, food security and rising middle classes in Asia demanding westernised foods and lifestyles.

“Now there’s the anticipation of a wet season and as a result, people are starting to become more optimistic and confident. However, the real driver is higher beef prices.”

“If people have the capacity and ability, they should be making acquisitions. Producers are far better buying now (in a drought) than waiting for rain, because the markets will increase. Now is the time. My opinion is that we have moved from the bottom of the market to a rising market,” Mr Honnef said.

So where is the chart plot-line headed?

According to Mr Honnef, up, up and up.

“Queensland will get a season. It may not be average or above average rainfall, but any sort of season will create some feed, and opportunities. Strong cattle prices, coupled with strong demand, will push beef prices even higher, and they are one of the core catalysts to property value changes. Higher beef prices will keep pushing up property prices.”

Mr Honnef said the Australian property market hit a peak in 2006-2007 and he predicts those levels will be reached again within the next 18 to 24 months.