In the second and final part of his analysis of different approaches to the property valuation task, Brisbane based accountant and property valuation professional Michael Vail walks through the valuation of a Central Queensland cattle producing enterprise.

A Pastoral Valuation

Let us assume that you have been offered the opportunity to buy a business: a going concern (with ‘all things necessary’), WIWO beef cattle production enterprise along the Ward River, south of Tambo, and east of Augathella, in Central Western Queensland.

Let us assume that you have been offered the opportunity to buy a business: a going concern (with ‘all things necessary’), WIWO beef cattle production enterprise along the Ward River, south of Tambo, and east of Augathella, in Central Western Queensland.

What is it really worth as an investment; and how would I approach this task?

Firstly, you should understand the likely net Cash-Flows of the enterprise, and to do that, some very robust assumptions must be made.

Assumptions:

- Land & Improvement values for quality grazing land have doubled since 1987, implying a Capital Gain rate-of-return of around 2.5% pa (using Rule of 72).

- The area of the subject property is 65,000-Acres.

- The sustainable stocking rate (SSR) is one adult equivalent (AE) to 14-Acres.

- The enterprise will be operated as a self-replacing, beef breeding concern, turning-off 18-month old Jap Ox, plus Cast-for-Age (CFA), and Culls.

- Over a 10-year cycle, rainfall is expected to be around 16” per Annum: and the falls may be spread throughout the year, albeit most will fall in the Summer months.

- Prices, and Costs, are expected to increase over time, in line with the CPI e of around 2.0% to 3.0%; an amount considered benign by central banks. This should continue over the medium term (i.e. 5-to-20 years), although a possible rise in underlying inflation may occur within the next 5-years, which will change actual outcomes.

- Revenue is expected to be around $1.95-million, and to grow at around 1.0% pa; based upon a retention rate of 20.0%, combined with a ROE of around 5.0%, as a minimum.

- An appropriate hurdle rate of return is 18.0% (before interest and taxation).

- EBIT will be around 45.0% of Revenue.

- Debt will be $NIL.

We now ask, “What is the Fair Investment Value for this going-concern enterprise?”

If the Vendors have compiled an independently vetted Information Memorandum (IM), which has been signed-off by Directors and their independent professional advisors, then of course, you may place more certainty around what might otherwise be considered hypothetical (read, ‘rubbery’) numbers.

It is good to be sceptical: think of an old Italian saying of, “If you ask the Water-seller if the water is fresh, what do you think he will say?”

You should mostly trust the IM, but always verify; using a visit to the property to see with your own two eyes, and other sources (e.g. in buying pastoral property, you should always go and speak to others in the area who have lived there a long time and know the property and management ‘quite well’). If the property is large, ask for an employee to drive you around for a few days, and in this way you may see more, and not become ‘lost’.

Let us assume the above assumptions are robust and correct.

The next step is to choose an appropriate valuation approach and methodology to apply.

The choices of approach to the valuation task are:

- Comparative Sales Analysis

- Asset Summation

- Industry ‘Rule-of-Thumb’

- Income

- Comparative Sales Analysis is the approach most Registered Land Valuers use (albeit with a check-test method or two), because it is ‘safe’; assuming the properties are in fact comparable. Many are not! Useful for a BARE-basis transaction. It is also preferred by the Law Courts.

Asset Summation is also used by Registered Land Valuers, especially in valuations for bank mortgage security and lending purposes. However, for the derivation of a Fair Investment Value it is not usually suitable, due to the synergy between assets, and potential for double-counting of the assets; and also the fact this approach is valuing assets on a break-up basis, as a Liquidator/Banker is wont to do. If a property is marginal for profit, and usually not a going-concern, then a break-up basis may be appropriate, though other methods may be more appropriate (e.g. the ‘Cost-to-Create’ method).

Industry ‘Rule-of-Thumb’ methods are applied every day by Valuers, Bankers, Pastoral Houses, Graziers and their Agents, and most other Stakeholders. The predominant one for the pastoral industry is the Beast Area Valuation (BAV) method; which is ‘about right’ when applied correctly as a WIWO, going-concern (with ‘all things necessary’) methodology.

For over thirty years now, in the Author’s memory, the BAV has been applied incorrectly on a BARE-basis; without apportionments to Stock-on-Hand, and Plant & equipment, and the Buyer then has to spend further Capital, the value of the Stock and Plant to replace them, and return to being a going-concern. BAV is always a WIWO methodology (Rost & Collins 1993 pp-284).

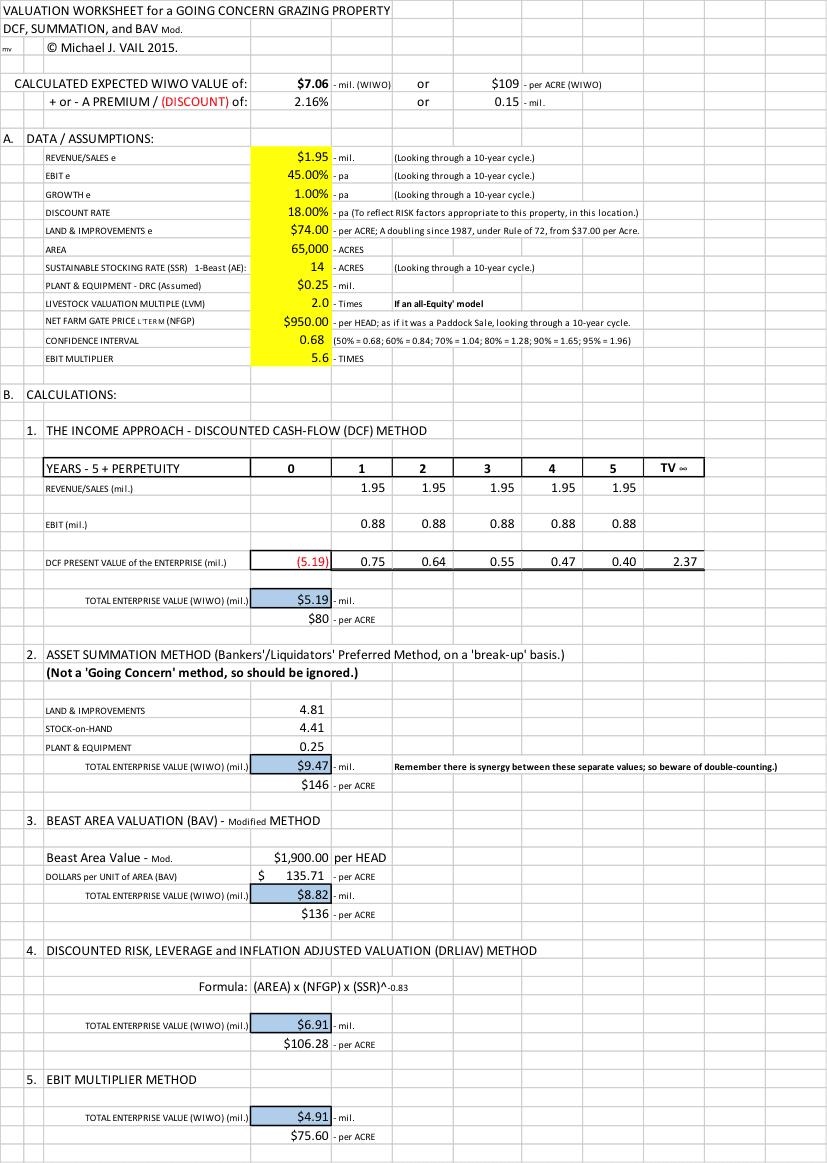

The Income approach is the preferred approach of valuing a going-concern and profitable enterprise; and the Discounted Cash-Flow (DCF) methodology should be considered to calculate the Free Cash-Flow of the Firm, and the Enterprise Value (EV).

Cash-Flow is true to the bank account (as it must reconcile), and unable to be ‘fudged’; though a Revenue (which is always maximised) method may be better, as it is considered ‘pure’. Because long-term Revenue has not been adulterated by management decisions, Accounting Standards, and taxation.

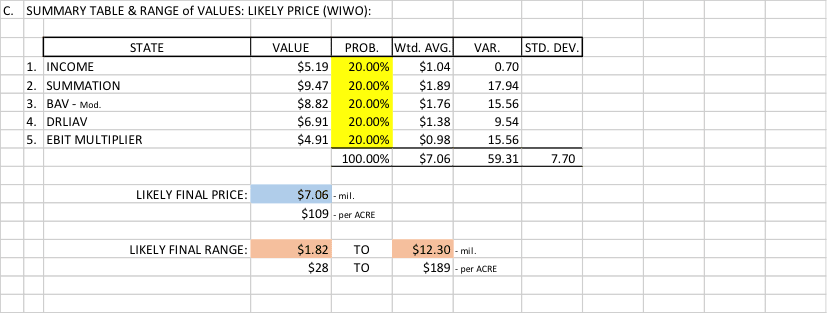

The valuation task should be approached to look at the asset from several perspectives, and an appropriate way to do that is to select at least two, preferably three separate methods/approaches to use. This sets a range of values, and a check-test on the others, with degree of dispersion being a buyer’s guide to relevance and accuracy.

You must understand that there is no one true value, and that all valuation lies in the eye of the beholder.

However, this approach will lead to a better guess.

For instance, we may choose an amalgam of:

- The Income DCF method as an a priori method, backed-up by,

- Asset Summation method,

- The Industry BAV Modified method,

- The Discounted Risk, Leverage and Inflation Adjusted Valuation (DRLIAV) method, and

- An EBIT multiplier method.

You may consider dropping-off the highest and lowest values, and take a simple average of the other three to arrive at your likely WIWO Value.

Comparative Sales Analysis should only be used, in my opinion, if properties are directly comparable; else it is a nonsense to use it. Very suitable to residential properties in the city, where there is volume and liquidity in the market, and price discovery is more efficient.

When using DCF or any methodology, a most important point to remember is that the assumptions must be robust; and tested as such, for that level of activity.

Despite the hurdle rate of return (i.e. discount rate) being very powerful in the denominator, with a lot of angst over the measurement and application of same, it is the robustness of the assumptions above the line, and the net cash-flows in the numerator which is paramount, because a large degree of error here will magnify the distortion once the denominator is applied; either too much, or too little.

The discount rate should adequately reflect reality, and the quantum of risk in the transaction: when the likely loss of Capital is measured.

The Author has found (Vail 2014) that the appropriate discount rate for this type of investment project is between 15% to 33.33% depending upon the risk factors identified, with most values falling around 21.5% (+/- 3.5%).

From this you may observe, that if most Australian industrial firms’ Weighted Average Cost of Capital (WACC) is around 12% or less, with late stage Venture Capital discount rate at around 15% (Mettrick & Yasuda 2010), and the one for a pastoral valuation is 21.5%, you may assume the difference is all pure risk weighting.

Ensure to factor this into future decision-making.

A Further Matter

The quantum of rural debt held by Banks is quite high, even by normal measure, when compared to assets, and whilst a few of the larger Banks have placed a moratorium on foreclosures at this time, this trend will continue for a while yet.

The problem for the rural industry is the ‘shake-out’ is not being allowed to happen. The normal template of viability has been set-aside, as they try to manage the net effects of any decision made on a Clients’ file.

If they put too many Clients into Asset Management, and eventually foreclose, they risk putting too many onto the market at any one time, causing downward pressure on prices; therefore affecting the value of the balance of their asset portfolio (ie our Debts are their Assets).

The Banks do not want to ‘own’ the properties outright, like what happened in the after-effects of the big drought in early 1900’s, and would prefer to give the Graziers who should go a ‘little bit more’ like an Option paying a small premium for plenty of up-side, knowing they will get it back when the property is eventually sold. The Option then costs them nothing. It is in their best interests to manage the situation, whilst possibly providing false hope for the Grazier and Family.

This means the market continues to ‘hold-up’ and is therefore artificially inflated due to self-interest, and unable to return to a reasonable level. A Buyer should have no doubt there is a very large overhang of properties which will be dribbled onto the market over time.

What happened to efficient markets and ‘true’ price discovery?

Something to be aware of.

The Valuation Calculations

Conclusions

When the five approaches are put into a statistical table and measures of dispersion, the mean, and standard deviation are taken, the likely top-price to pay for the Enterprise Value of the property as a going-concern (with ‘all things necessary’) WIWO is $7.06-million (albeit with a range of $1.82-million to $12.30-million), using a Confidence Interval of only 50% due to the uncertainty around the data.

An investor would try to pay less than this WIWO number to ensure they pay an economic price to secure the property.

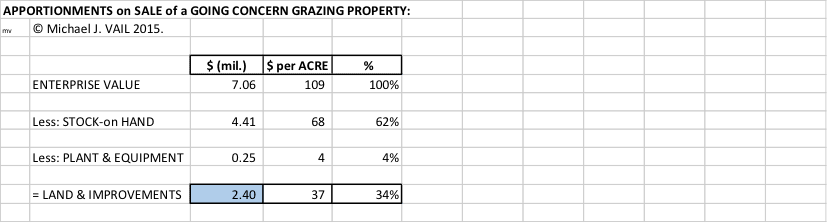

If the property is not a going-concern, and is offered on a BARE-basis, net of Stock and Plant, then the values to replace those assets today will be deducted from this Enterprise Value to arrive at the Land & Improvements value of $37.00 per Acre; which is the BARE-basis price to pay. All else is folly!

If you pay a WIWO price for a BARE-basis offering, then in this instance you will have paid $109.00 for only $37.00 of value. Not very smart, or prudent, considering it will eventually amount to a going-concern premium of more than 66.0%. To put this premium into context, a company purchased on the ASX (where full transparency is key), may pay around a 20.0% premium for control; in a private transaction, private business has private knowledge, and not ‘all’ data/information is known. Therefore more risky.

I hope this helps those out there who are wondering about how to approach the task. I am happy to be proved wrong, and am open to query. I can be contacted on 0488778811, or via email at michael@treponte.com.au

Thank you for taking the time to read this article.

Michael Vail, TRE PONTE Corporate, Brisbane

The author Michael J. Vail, M App Fin, M Prop Val, F Fin, CTA, FCPA, is a director of TRE PONTE Corporate in Brisbane . He can be contacted by email by clicking here

To read previous articles on Beef Central by Michael Vail, click here