THE answer to this question depends a lot on how you define ‘value’.

We are referring primarily to the intrinsic economic value of a property, as opposed to the value placed on it by the market. A previous article on ‘Beef land vs. Gold’ discusses different approaches to valuation.

The intrinsic economic value of an asset is essentially its value based on its future earning capacity, which means that land condition has a big effect.

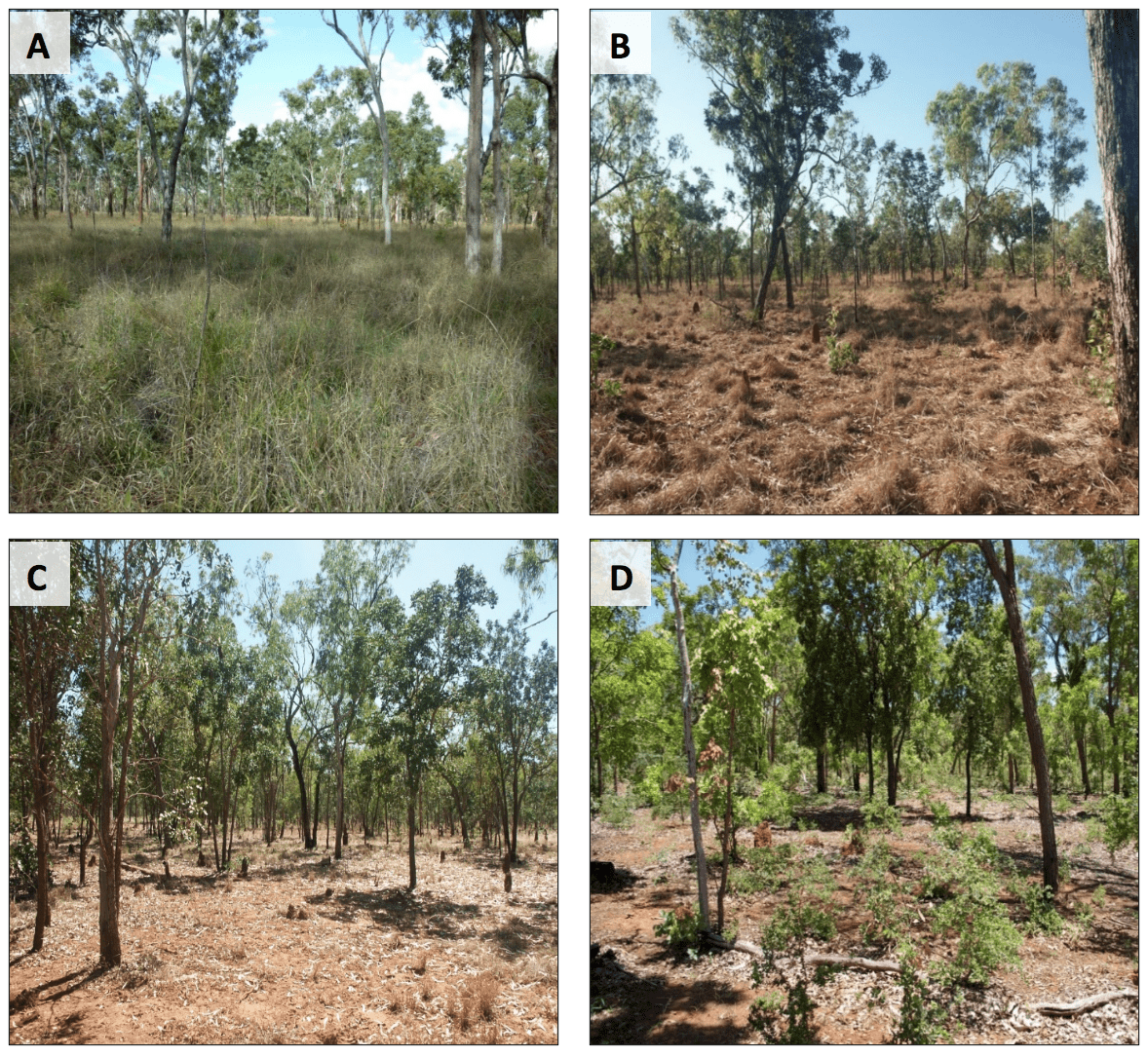

There are four categories of land condition recognised in northern Australia: ‘A’ for good condition, ‘B’ for fair, ‘C’ for poor and ‘D’ for very poor. This report-card style classification is determined by the health and functioning of the pasture and soil components of the area being assessed. Land in poor (‘C’) condition grows less than half the quantity of useful pasture compared to the same land type in good condition, regardless of season. This means the number of stock that can be supported by degraded pastures will be less than half what they could be on good condition land. B land condition grows 75% of the useful pasture that A does, and D 20%, see pictures below.

ABCD land condition ratings for a savanna woodland.

ABCD land condition ratings for a savanna woodland.

Note the decline in 3P grass density, increased bare ground and woody vegetation thickenings as land condition declines in this example.

The chief determinant of an ABCD land condition rating is pasture condition, as indicated by the presence and density of 3P (Perennial, Productive and Palatable) pasture species. The next important factor is soil condition, which assesses its potential to store and cycle nutrients and absorb rainfall. The percentage of bare ground is a key metric that indicates how susceptible the soil is to erosion. Trees and shrubs play important roles in water and nutrient cycling in rangeland ecosystems; however, woodland thickening can reduce pasture growth and ground cover, resulting in less-productive pastures and lower carrying capacities.

We think that determining the true intrinsic value of a potential purchase is all about first class due diligence and that ball is entirely in your court. There are only three variables in both the north and the south:

- The long-term sustainable carrying capacity of the property.

- The current land condition of the property.

- The expected EBIT per AE or DSE.

The first two should be provided as a report on an assessment conducted by an experienced professional rangeland practitioner in the north and an experienced private pasture agronomist in the south. Anything less will be guesswork. Land condition can be addressed through fertilisers and pasture rejuvenation in the south, but these are often not economic in the north. Mechanical intervention may be, otherwise it is a matter of time.

Knowing your expected earnings before interest and tax (EBIT) per animal unit from the acquisition is essential. This requires a good understanding of your current performance as well as expected productivity and operating costs of the acquisition. Managing, or buying, a grazing business without knowing these numbers makes decision making a stab in the dark. The data tables in the Australian Beef Report provide a starting point.

The following table is an example of how this might work in the north, accounting for the effect of land condition. We have Surprise Downs, a 120,000 hectare station just this side of Woop Woop. We’ve modelled two potential scenarios, Scenario 1 has the majority of the property in A and B condition, whereas Scenario 2 has the majority in C and D condition.

Example of land condition impact on land valuation

| Surprise Downs Station 120,000 ha | |||||||

| Land Condition Assessment Category | |||||||

| Scenario 1 | A | B | C | D | Total | ||

| Area % | 40% | 35% | 20% | 5% | 100% | ||

| Area (ha) | 48,000 | 42,000 | 24,000 | 6,000 | 120,000 | ||

| AE/100ha | 7.0 | 5.4 | 3.0 | 1.4 | |||

| Total AE (CC) | 3,360 | 2,264 | 722 | 84 | 6,430 | ||

| Scenario 2 | A | B | C | D | Total | ||

| Area % | 5% | 20% | 35% | 40% | 100% | ||

| Area (ha) | 6,000 | 24,000 | 42,000 | 48,000 | 120,000 | ||

| AE/100ha | 7.0 | 5.4 | 3.0 | 1.4 | |||

| Total AE (CC) | 420 | 1,294 | 1,264 | 672 | 3,650 | ||

| EBIT/AE: | $80 | ||||||

| Capitalisation Rate: | 4% | ||||||

| Value Scenario 1: | $12.9M | ||||||

| Value Scenario 2: | $7.3M | ||||||

The first pass at a valuation involves multiplying the LTCC by the EBIT per AE to calculate estimated business EBIT, and then dividing the result by the required rate of return, in this case 4% (i.e. capitalisation of EBIT valuation).

The above example shows a staggering $5.6M difference in the intrinsic economic value of Surprise Downs Station, based entirely on land condition. If you want to pay $13M for it in Scenario 2, you will need to have an EBIT per AE of around $145 to achieve a 4% return. If you are only at $80 it is a big call to get to $145 quickly.

The rate of return (capitalisation rate) is critical and it is up to you. We believe that 4% is entry level; below this you are not really serious about your business. If you use 2% you can afford to pay $26M in Scenario 1, but if you choose 6%, all you can afford is $9M. This single number can and does decide whether a purchase will be wealth creating or wealth destroying.

The immediate reaction when one pays too much is to stack the cattle on to make as much money as possible to justify or clear the debt. This process just compounds the problem.

The above template is universally applicable and can be adapted for the south if potential purchasers are serious.

Current land prices make achieving a reasonable return very difficult, but to us this means that thorough due diligence is even more critical. You may have to look at 20 or more potential acquisitions before you find the gem, but the gems are always there, truly. It needs patience and discipline because the decision has long-term consequences.

Purchasing a property without proper due diligence and an estimate of its intrinsic economic value is like trying to draft cattle with a blindfold on. You may get the odd call right, but it will inevitably be a result of random chance. There is no room for random chance in rural asset purchases, just as there is no room for flogging landscapes beyond capacity in order to make foolish financial decisions work.

This aricle is an edited excerpt from ‘The Australian Beef Report: 2020 Vision’, more information is available at www.bushagri.com.au/abr