AS THE long and eventful 2016 beef slaughter season draws to a close, stakeholders are starting to reflect on the year that was, and what lies ahead for 2017 in terms of cattle supply and beef production prospects.

Tightest cattle supplies in 20 years has been the underlying story in the processing sector this year, and to some extent its miraculous that a number of smaller processors did not pull up stumps during the year as the deadly price tussle for meagre cattle supplies unfolded.

After two years of record beef kills forced by drought, 2016 became a struggle to retain market share for many processors, forcing prices ever-higher. From its peak during May around 585c/kg for four-tooth grassfed ox in southern Queensland plants, there has been a gradual easing back to rates today around 540c for the same animal, as slaughter losses mounted.

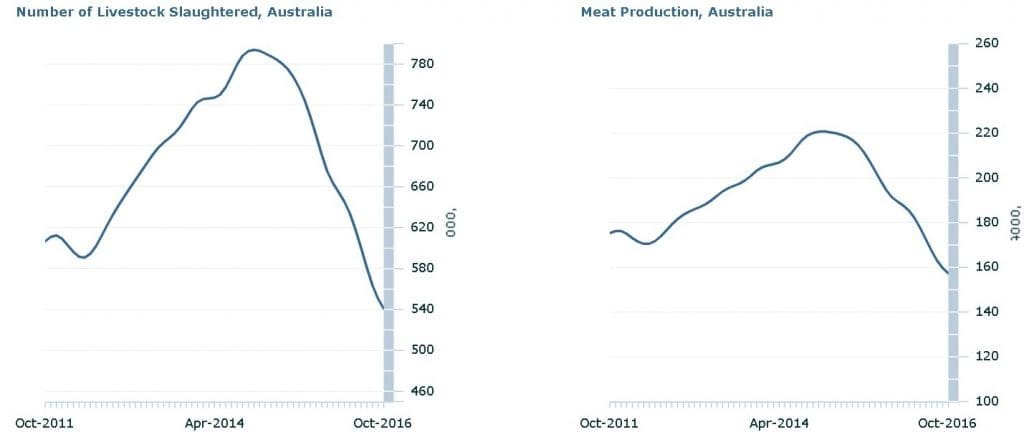

The difficulty in sourcing slaughter stock throughout 2016 is evident in latest ABS statistics released this morning, which show total slaughter numbers for October at 540,0765 head, almost 24 percent behind the same period last year, representing a total ‘loss’ of almost 170,000 head.

The ABS figures, while lacking the currency of weekly kills reported by NLRS, help illustrate the extent of the longer-term decline on slaughter performance this year. The graphs published above show cattle (not livestock, as titled) slaughter numbers and beef production, using a ‘rolling 12-month’ average methodology based on monthly turnover. It shows that the monthly rolling average continues to fall as recently as October, now reaching 540,000 head per month, or about 135,000/week.

Similarly, meat production continued to trend downwards through the year, reaching 160,000t/month as a rolling average in the most recent graphs released this morning.

Second and third quarters of 2017 could be ‘horrendous’

Will that plot line now start to level out, or indeed start to recover?

Processing contacts we’ve spoken to regularly throughout the 2016 year hold out little hope for any significant improvement in 2017.

The general consensus, given anything like a normal wet season emerging in coming weeks/months, is that slaughter cattle supply is likely to be ‘OK’ during the first quarter, but desperately tight during the second and third quarters ending September 30.

One large multi-site, multi-state processor is anticipating quarters two and three next year to be ‘horrendous’ for supply of both feeders and fat cattle, before a modest recovery cuts in later in the year.

If it stays dry over summer, the additional weight cattle gained after unseasonal rain during the back half of this year is likely to bring those cattle forward, even earlier – especially in the north. That scenario is likely to see some processors wary about opening northern export plants early, only to have to close them later in the year due to lack of numbers – at enormous cost.

Strategic closures by smaller single site processors unable to maintain the pace on cattle price has to be on the cards again next year, but every export plant in the country has export customers it wants to maintain, and any closures risks losing those relationships.

Meat & Livestock Australia’s most recent October industry projections update has cattle numbers next year lifting marginally – up 1.5pc to 26.54 million head, before topping 28m head again by 2019 as the recovery processes builds.

Expectations are for adult cattle slaughter to drop a further 2pc next year to 6.9m head, due to the circumstances described above.

Beef exports have been in decline during 2016, and trade will continue to remain slow during 2017, with MLA’s expectations of total shipments declining a further 4pc to 940,000t – the lowest volume since 2010.

This means the domestic : export ratio will return to longer-term average levels and exports are likely to account for 68pc of production, compared to a record high 74pc in 2015.

Kill little changed

Last week’s seven-day eastern states kill reported by NLRS was 130,922 head, down just marginally on the week before. Most processors appear to have most of their kill slots covered for the run through to Christmas closure, with the ‘take’ out of saleyards this week adequate to cover their needs – despite some of yesterday’s yarding being well down.

Some Queensland plants were pulling cattle out of the south to fill their needs, despite the hot weather. Toowoomba’s offering yesterday was back 16pc on the previous week, while numbers at TRLX Tamworth fell 27pc, and Wagga was back 7pc, to 3765 head. The harvest season continued to impact saleyard numbers in southern areas this week.

Grids steady

Southern Queensland grid prices were stable again this week, and are now little likely to change before the Christmas closures. Best offers seen this morning from large Queensland export processors for kills before December 16 shut-downs were 535-540c/kg for grassfed four-tooth ox, and 475-485c/kg for heavy cows.

A northern NSW export plant is among those that is no longer quoting on kills for 2016, and has already issued grid offers for week commencing January 9 next year. Its opening offer for four-tooth grassfed steer for the 2017 year is 510c (HGP-free), and eight-tooth heavy cow 460c. That’s a further 10c/kg dressed weight decline on the same plant’s final grid for kills seen in 2016.